Editor's Note: This article is part of an ongoing RANE series on the shifting patterns of global trade. The first installment provided a broad overview of the geopolitical and economic implications of these shifts. Other installments have examined trade patterns in the Americas, the Strait of Hormuz, Japan and South Korea, India, Turkey, ASEAN countries, the data flows, Mercosur, maritime chokepoints (part one and part two), digital trade and Congo. The first part of this installment on East Africa can be found here.

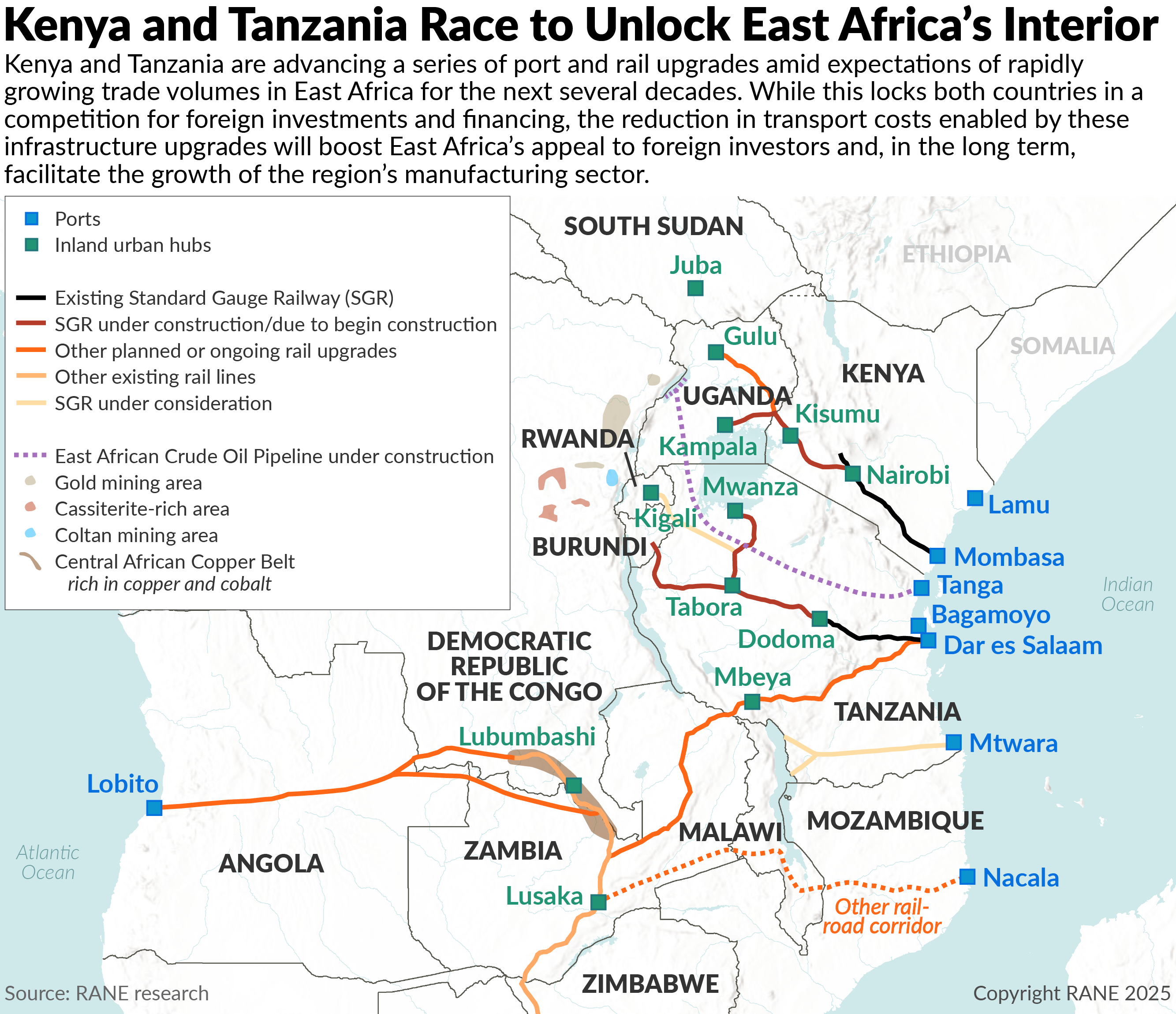

Kenya and Tanzania's infrastructure buildup will support East Africa's industrialization in the coming decades, but the extent to which the region benefits from these initiatives will depend on governments' willingness to deepen regional integration, shifts in the international trading system, global growth outlook and technological changes. East African countries' infrastructure buildup will help provide employment for thousands of workers and stimulate regional demand through the procurement of materials. Although this will boost the region's economic growth in the short term, infrastructure upgrades will deliver their full potential in the long term by lowering transportation costs and supporting larger trade volumes. Even though Kenya and Tanzania are now competing against each other to secure investments, their contest will help shore up the attractiveness of East Africa as a whole for foreign investors. Importantly, the reduction in transportation costs will set the stage for the region to better leverage low labor costs to attract manufacturing activity, which will be critical for national governments to provide employment opportunities for their rapidly growing populations. This could enable the region to gradually emerge as a new frontier for light manufacturing through the 2030s as wages rise in Asia and other manufacturing centers. Moreover, rail upgrades and extensions will enable the growth of regional value chains that span the hinterland, supporting the development of secondary hubs and ensuring that economic opportunities are not limited to coastal regions. While Kenya appears more likely to specialize in services and higher-end products, given its higher educational attainment, Tanzania's lower wages and status as a gateway for the Democratic Republic of the Congo and Zambia's critical minerals will likely see it specialize in labor-intensive sectors and mineral beneficiation activities.

- The combined population of Kenya, Uganda, Tanzania, Rwanda and Burundi is set to rise from around 208 million in 2025 to 345 million in 2050, creating major challenges for national governments to create sufficient employment opportunities.

Uganda, Rwanda and Burundi will likely leverage Kenya and Tanzania's transport infrastructure buildup to diversify their trade routes, which will increase the resilience of regional supply chains and facilitate greater regional integration. The vast majority of Uganda's international trade currently runs through Mombasa, while Rwanda and Burundi heavily rely on Dar es Salaam to access global markets — meaning all three countries' supply chains are vulnerable to single points of failure. As alternative trade corridors become less costly, landlocked states around the Great Lakes will likely diversify their export and import routes to de-risk their supply chains. In turn, this will enhance the resilience of regional supply chains and mitigate the risk of severe trade disruptions during protests or unexpected logistical bottlenecks in Tanzania or Kenya. Moreover, the planned connection of Kisumu, Kampala and Mwanza to the region's standard gauge railway (SGR) network and ongoing expansion of fluvial ports will likely boost trade across Lake Victoria. However, landlocked states' push to diversify their trade routes could result in comparatively higher costs due to smaller economies of scale, especially if implemented at a company level. Nonetheless, Uganda, Rwanda and Burundi will likely leverage the rise of more cost-effective trade corridors to extract concessions from either Kenya or Tanzania, such as lower transit fees, smooth border checks or pledges to tackle nontariff barriers. Despite these de-risking trends, Kenya appears likely to remain Uganda's preferred transit destination as both countries' economies and urban networks are well integrated — especially if the Naivasha-Kampala SGR section is swiftly completed.

- While Kenya is Uganda's preferred export route, it decided to have its East Africa Crude Oil Pipeline terminate at the Tanzanian port of Tanga. Although this decision was driven by a variety of factors, it will enable the Ugandan government to mitigate its reliance on Kenya.

Tanzania and Kenya's diversification of funding sources to finance their port and rail projects mitigates their reliance on China, but the scale of investments means that their infrastructure buildup still entails long-term fiscal risks, especially if planned and ongoing upgrades fail to deliver expected returns. Since the 2010s, East African countries have diversified their financing for large infrastructure projects, with a preference for blended finance over large loans from Chinese banks. Even when Chinese entities play a pivotal role in an infrastructure project, Nairobi and Dodoma now often favor handing over the project's operatorship to investors for a predetermined period of time rather than relying on large Chinese loans, as seen with the planned expansion of Kenya's SGR and the refurbishment of the Tazara rail line. This has enabled states in the region to reduce their overall reliance on Chinese financing and the dependency risk it entails by attracting more investment from international and multilateral banks as well as state-linked entities from the Middle East and India. However, this financing strategy is not without risks. Private sector lending is likely to be in foreign currency and often entails higher financing costs when compared to large state-owned Chinese banks. Moreover, the loss of operatorship will see governments lose revenue generated by these infrastructure upgrades for years and sometimes decades, which could heighten debt-servicing challenges. Meanwhile, the financing requirements for infrastructure upgrades in Tanzania, and to a lesser extent Kenya, are very large when measured as a proportion of GDP. Should these projects not yield their expected economic and financial returns, Nairobi and Dodoma would face heightened financial challenges — especially in the event of an external shock, such as a global recession, steep surge in global interest rates or appreciation of the U.S. dollar, which would make their external debt more expensive. Meanwhile, the pivot toward blended financing could make hypothetical debt restructuring talks in the future more challenging, given the large number of creditors.

- The total cost of Tanzania's new SGR network amounts to an estimated $10 billion, with the Isaka-Mwanza and Tabora-Kigoma sections financed by China's state-owned Sinosure at a cost of $1.3 billion and $2.7 billion, respectively. The Tanzanian government also secured $1.2 billion in funding from an African Development Bank-backed syndicated loan as well as a $1.5 billion loan from Standard Chartered, but the source of outstanding financing is currently unclear. Together with the SGR extension to Burundi, this accounts for over 14% of Tanzania's GDP.

- Kenya's SGR extension from Naivasha to Malaba alone is expected to cost $5.3 billion, or around 4% of the country's GDP. While comparatively less expensive than Tanzania's SGR upgrade, Kenya is already facing major financial challenges that prompted its government to resort to an International Monetary Fund program in 2021. Despite the advancement of fiscal consolidation in recent years, the country's projected fiscal deficit still stood at 5.7% of GDP in the 2024-2025 fiscal year. Its debt-to-GDP ratio is 68%.

In addition to infrastructure upgrades, East African countries' ability to industrialize their economies will hinge on other factors, including the reliability of their power supply, shifting international trade dynamics, changes in the global economic outlook and technological progress. Although lower transportation costs will play an important role in increasing East Africa's attractiveness, they will not be the only factor determining manufacturers' and foreign investors' interest in the region. While the East African Community has made strides in lowering tariffs between member states, nontariff barriers remain a hindrance to the growth of regional value chains. Despite recent pledges by Kenya and Uganda to tackle nontariff barriers, Tanzania has shown little willingness to liberalize its trade policy with neighboring countries. Meanwhile, East African countries will also need to ensure that their infrastructure buildup also involves a rapid expansion of their domestic power supply if they are to ensure the growth of their manufacturing sector and the economy at large. Foreign investor interest will also depend on exogenous factors such as international trade dynamics. For now, East African countries can leverage lower U.S. tariffs than most Asian economies, as shown by the fact that several Indian manufacturers are reportedly seeking to expand their footprint in the region. However, this state of affairs could rapidly change in the event of a narrowing — or reversal — of the tariff gap between East African countries and their Asian counterparts. Changes in the world's long-term economic outlook, such as a potential steep decline in China's economic growth, resulting in less demand for East African exports, could also slow economic growth in the region by reducing global demand. Finally, progress in the fields of robotization and artificial intelligence will also play an important role in determining the future growth of East Africa's manufacturing sector. While these new technologies could reduce the importance of wage competitiveness, East African governments that do embrace technological changes — such as Rwanda — may prove successful in keeping pace with expected improvements in labor productivity globally, which would put them on a stronger footing to secure their long-term economic development.

- On July 30, Kenyan President William Ruto and his Ugandan counterpart Yoweri Museveni signed eight memorandums of understanding and vowed to tackle nontariff barriers hindering trade between their two countries. This came as Tanzania banned foreigners from working in 15 sectors, including small-scale mining and tour guiding.

- On Sept. 18, Reuters reported that Indian textile manufacturer Gokaldas was looking to expand its footprint in Africa following U.S. President Donald Trump's imposition of 50% tariffs on India. Gokaldas has already developed a footprint in Kenya and Ethiopia.

- As of early November, the United States has imposed 10% tariffs on exports from Kenya and Tanzania and 15% on Uganda, against 20% for Bangladesh and Vietnam and 19% for Indonesia and the Philippines.