Editor's Note: This article is part of an ongoing RANE series on the shifting patterns of global trade. The first installment provided a broad overview of the geopolitical and economic implications of these shifts. Other installments have examined trade patterns in the Americas, the Strait of Hormuz, Japan and South Korea, India, Turkey, ASEAN countries, the data flows, Mercosur, maritime chokepoints (part one and part two) and digital trade.

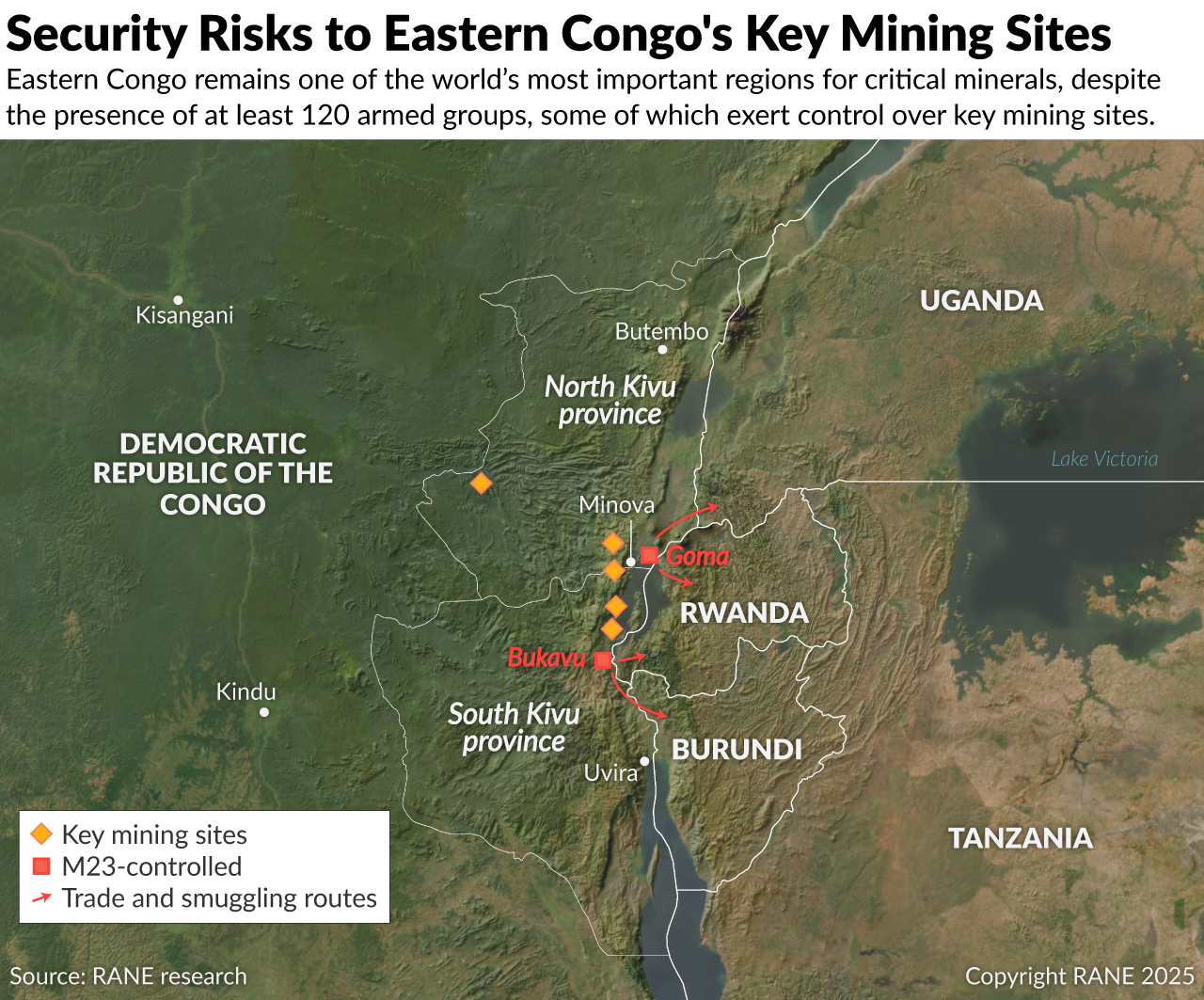

The Democratic Republic of the Congo is likely to remain a high-risk location for sourcing critical minerals in the coming years, sustaining various legal, financial and reputational pressures. The potential easing of Western regulations could temporarily reduce these risks, though it would also incentivize due diligence shortcuts that increase exposure to conflict-linked minerals over time. According to numerous metrics, Congo is the world's highest-risk location for so-called "conflict minerals," meaning those extracted from areas experiencing typically prolonged conflict often driven by competition over resources, intercommunal violence, proxy wars and insurgencies. The conditions under which these minerals are extracted often include human rights violations, at times spanning from their initial extraction process through to their final sale. In Congo, conflict minerals are concentrated mainly in the eastern region, an area home to more than 120 armed groups. Within eastern Congo, the most common conflict minerals are tin, tungsten and tantalum — commonly referred to as the 3Ts — which are sometimes grouped with gold, another conflict mineral. These are typically sourced from many informal artisanal mines and small- or medium-scale enterprises, many of which are controlled or taxed by rebel groups that use the proceeds to fund their operations. Even with the persistent influence of these armed groups, Congo remains a major player in the global supply chain for several critical minerals due to its large deposits and high global demand. While many multinational companies have conflict-free sourcing policies, activist groups, global watchdogs and others frequently find evidence of conflict minerals still making their way into global supply chains.

- Since the mid-1990s, Congo has experienced persistent conflict that has created conditions for rebel groups in the east to grow territory they control and strengthen their capabilities, driven by competition over natural resources, a weak state presence, ethnic tensions and the involvement of neighboring countries in regional power struggles.

- Throughout North and South Kivu in eastern Congo, numerous gold, tungsten and tantalum deposits are often subjected to informal taxation by groups such as the Rwandan-backed M23, the Democratic Forces for the Liberation of Rwanda (FDLR), Mai-Mai militias and remnants of the Coalition of Congolese Resistant Patriots-Strike Force (PARECO-FF). These groups and many more continue to take advantage of porous borders and weak customs enforcement to move minerals along well-established smuggling routes, mostly into Rwanda, Uganda and Burundi, where they eventually enter the legitimate global market.

- According to the U.S. Geological Survey, in 2023 Congo accounted for roughly 40% of global output of coltan (from which tantalum is extracted), making it the leading producer. Other major contributors included Australia, Canada and Brazil. However, neighboring Rwanda plays a major role as nearly 60% of Rwanda's coltan exports are sourced from Congo. Congo produces over 70% of the global supply of cobalt and is a significant source of tin and tantalum, underscoring its central role in the supply of key conflict minerals. Coltan, cobalt, tin and tantalum are essential for high-tech and green industries, including electric vehicle batteries, semiconductors, smartphones, laptops and renewable energy technologies.

While the M23 serves as a prominent example of how an armed group can assert control over mining in the eastern Congo, it is just one facet of a wider conflict environment, leaving companies sourcing from the region vulnerable to operational disruptions, legal liabilities and reputational risks amid tightening international compliance standards. The trade in conflict minerals in eastern Congo has long been linked to local power structures and economic incentives, and continues to influence global markets today. Some foreign firms rely — both directly and indirectly — on supply chains partly originating in Congo. These are often fragmented and informal, contributing to factors that allow armed groups to maintain their ability to control mines, impose taxes and enforce compliance. A clear example is the Rubaya coltan mine in North Kivu, now under the control of the M23 rebel group. This site produces around 15-20% of the world's coltan. Since assuming control in 2024, the M23 has reportedly earned nearly $800 million through mining, trade and taxation. The M23 also has established administrative structures, replacing local chiefs, introducing a business registration system to regulate and tax operators and managing strategic transit routes, such as tin- and gold-rich Walikale, and customs posts along the Rwanda border. These developments both strengthen the M23's influence and create ongoing risks for international supply chains as sourcing companies remain exposed to conflict-financing concerns and the potential for changes in territorial control to disrupt supply chains. Rwanda's involvement further complicates the situation. Accused of providing military support to the M23, it has simultaneously grown into a significant regional hub for mineral exports. As a result, businesses operating in or sourcing minerals from eastern Congo face intensifying compliance pressures, driven by increased global scrutiny, including the risk of substantial fines, legal action and reputational damage if they fail to ensure conflict-free sourcing. High-profile cases illustrate these stakes. In late 2024, the Congolese government filed criminal complaints against Apple in Europe alleging that its supply chains included minerals sourced from conflict-affected areas in Congo and Rwanda, raising questions about oversight and accountability. These developments have accelerated international regulatory responses, including the EU Conflict Minerals Regulation, which since 2021 has required companies to conduct rigorous due diligence on the 3Ts and gold to prevent financing armed groups, and U.S. sanctions targeting militias and exporters involved in illicit trade. Companies are now under growing pressure to implement comprehensive supply chain audits, third-party verification and traceability measures, not only to comply with the law but also to safeguard their brand reputation and maintain investor and consumer confidence in ethics-driven markets.

- The M23 has taken control of several other important mining sites in eastern Congo. These include Lumbishi and Numbi in Kalehe district, which produce gold, tourmaline and the 3Ts; Nyabibwe, a tin-producing village about 30 miles south of Minova, from which 186 tons of minerals were smuggled to Rwanda via Lake Kivu; Luhihi gold mine near Kavumu airport on the RN2; and Katasomwa, a gold-producing village at the northern edge of Kahuzi-Biega National Park. Together, these captures have allowed the M23 to consolidate control over a significant portion of the region's mineral resources.

- Many Western governments and international organizations have also stepped up efforts to disrupt the role of non-state actors who exploit eastern Congo's mineral resources to fuel armed conflict. For instance, in August 2025, the United States sanctioned the armed group PARECO-FF — which had controlled key mining sites such as Rubaya between 2022 and 2024 — alongside several associated mining companies and exporters. According to the U.S. Department of the Treasury, these actors diverted revenues from the illicit trade of coltan and the 3Ts to fund armed activity and further destabilize the region.

- Revenues from mineral exports in Rwanda amounted to over $1.1 billion in 2023, according to Reuters, illustrating the intersection of regional political interests and economic gains in the conflict mineral trade.

With demand for minerals such as the 3Ts likely to grow in the coming years amid ongoing insecurity in eastern Congo, armed groups face strong motives to expand control over mining, which would heighten legal and reputational risks for foreign companies as potentially weakening regulatory enforcement could further undermine supply chain transparency and compliance. In the coming years, armed groups in eastern Congo, including the M23, will likely face strong incentives to launch at least small-scale offensives to capture new mines in order to generate additional revenue. The fragile peace agreement between Rwanda and Congo, designed to limit external support for the M23 and stabilize the region, has seen limited implementation. Any failure to enforce its terms over time — including a negotiated settlement between the M23 and the Congolese government — is likely to trigger more frequent clashes. Surging global demand for critical minerals such as the 3Ts is likely to motivate other armed groups, such as Mai-Mai militias, to further assert control over both artisanal and industrial mining sites, risking intensifying competition and conflict with other groups. Combined with the informality of artisanal operations, porous borders, weak governance and periodic outbreaks of violence, on-the-ground audits, verification programs and traceability schemes — already hazardous and not necessarily reliable — are likely to face even greater challenges. As a result, foreign firms are likely to face continued challenges including restricted site access, physical threats and disruptions to operations from armed actors. Reduced access for independent monitors and nongovernmental organizations will also increase compliance and legal risks, including the physical diversion of minerals, misreporting of their origin and commingling of conflict-linked minerals. Meanwhile, regulations such as the EU Conflict Minerals Regulation and the U.S. Dodd-Frank Act, which have been putting pressure on foreign companies to ensure their supply chains are free from conflict minerals, may relax these requirements or deemphasize enforcing them as critical minerals are increasingly treated as vital strategic assets. In this event, companies could face tensions between meeting compliance obligations and securing access to critical minerals, potentially incentivizing shortcuts in due diligence, increasing exposure to reputational risks and further undermining transparency in already fragile supply chains.

- High unemployment and poverty in Congo, especially in the poorer eastern regions, have pushed local populations toward artisanal mining under armed group influence, fueling cycles of competition, extortion and informal taxation that entrench instability.

- According to the International Energy Agency, global demand for critical minerals, particularly the 3Ts, is likely to continue surging due to the renewable energy transition, proliferation of electric vehicles and the expansion of high-end industrial applications. For instance, tin is crucial for soldering in solar panels, wind turbines and battery systems; tantalum is essential for capacitors in EVs, energy storage and solar inverters; and tungsten is used in high-performance machinery and specialized electronics supporting renewable energy infrastructure. Demand for key minerals such as cobalt and nickel is also projected to double by 2040, while graphite demand could quadruple, highlighting the indispensable role of these minerals in powering clean energy technologies and industrial systems.

In the coming years, companies sourcing minerals from eastern Congo will likely continue to face compliance, operational and reputational risks, while regional frameworks could gradually improve supply chain integrity. However, progress is likely to be slow. Any easing of conflict-free sourcing standards in the West may reduce short-term compliance burdens but will increase exposure to conflict-linked minerals and long-term reputational harm. In the coming years, foreign firms sourcing minerals from eastern Congo will still face strong compliance pressures, driven by regulatory oversight, investor demands and public scrutiny — particularly regarding the M23's ongoing insurgency, allegedly backed by Rwanda. However, recent initiatives such as the U.S.-led Regional Economic Integration Framework (REIF), initiated in August 2025 by Congolese and Rwandan officials as part of the broader peace agreement signed in June, provide an opportunity for regional countries to begin achieving some level of supply chain integrity and traceability, with potential long-term impacts. The minerals deal under this framework carries strong economic incentives and could generate large returns for both countries. This could be achieved through formalizing artisanal mining via registration, licensing and technical training on safe and sustainable extraction practices. Additional measures could include implementing mineral tagging systems, conducting joint cross-border audits and utilizing digital shipment tracking from mine to export. Cross-border cooperation would further strengthen customs oversight, harmonize export regulations and ensure minerals are transported legally and transparently. But even with political will, achieving these goals will be difficult and likely take years due to entrenched informality in artisanal mining, armed group control, corruption, weak governance and limited infrastructure for tagging and digital tracking. In addition, historical mistrust between Rwanda and Congo could hinder genuine cross-border cooperation, leaving companies exposed to various sourcing risks. Moreover, while schemes such as the International Tin Supply Chain Initiative (ITSCI) aim to enhance traceability, their impact is likely to remain constrained by limited oversight capacity, operational inefficiencies and persistent insecurity. Mining companies operating on the ground will face ongoing risks of site closures, license suspensions and operating disruptions from insecurity, while downstream companies sourcing these minerals will remain exposed to legal, financial and reputational risks. Finally, while companies may face laxer regulation or enforcement from regulators in the United States, Europe and elsewhere, thereby reducing their compliance burdens in the short term, this could also incentivize shortcuts in due diligence, increase exposure to conflict-linked minerals and undermine long-term supply chain transparency and reputational safeguards.

- While some companies outside of the REIF could look for alternative sources of minerals that are not from conflict regions such as eastern Congo, this process will take years. Obstacles include the limited availability of suitable deposits and the extremely high costs and time required to develop new mining operations. As a result, Congo, at least for the medium- to longer-term, will remain one of, if not the, biggest source for key minerals such as the 3Ts.

- ITSCI relies on a tagging system at mine sites. However, these tags are often sold on the black market and affixed to minerals from unapproved sources. Moreover, armed groups frequently infiltrate ostensibly "clean" sites, which means physical audits can become risky or even impossible when security conditions deteriorate. Finally, due diligence audits are typically announced in advance, allowing local actors to temporarily stage compliance measures and conceal illicit activity.

- Nearly 75% of the world's cobalt is extracted from Congo, though from the southern Katanga region in the south, not east of the country. Cobalt is frequently extracted under high-risk conditions — marked by child labor, unsafe artisanal practices and corruption — which have prompted increasing calls to classify it as a high-risk mineral. As a result, many companies and investors have begun voluntarily incorporating cobalt into their supply chain due diligence, particularly as global demand rises.