Editor's Note: This article is part of an ongoing RANE series on the shifting patterns of global trade. The first installment provided a broad overview of the geopolitical and economic implications of these shifts. This second installment explores how recent changes to U.S. trade and tariff policies will affect nearshoring trends in Canada, Latin America and the Caribbean.

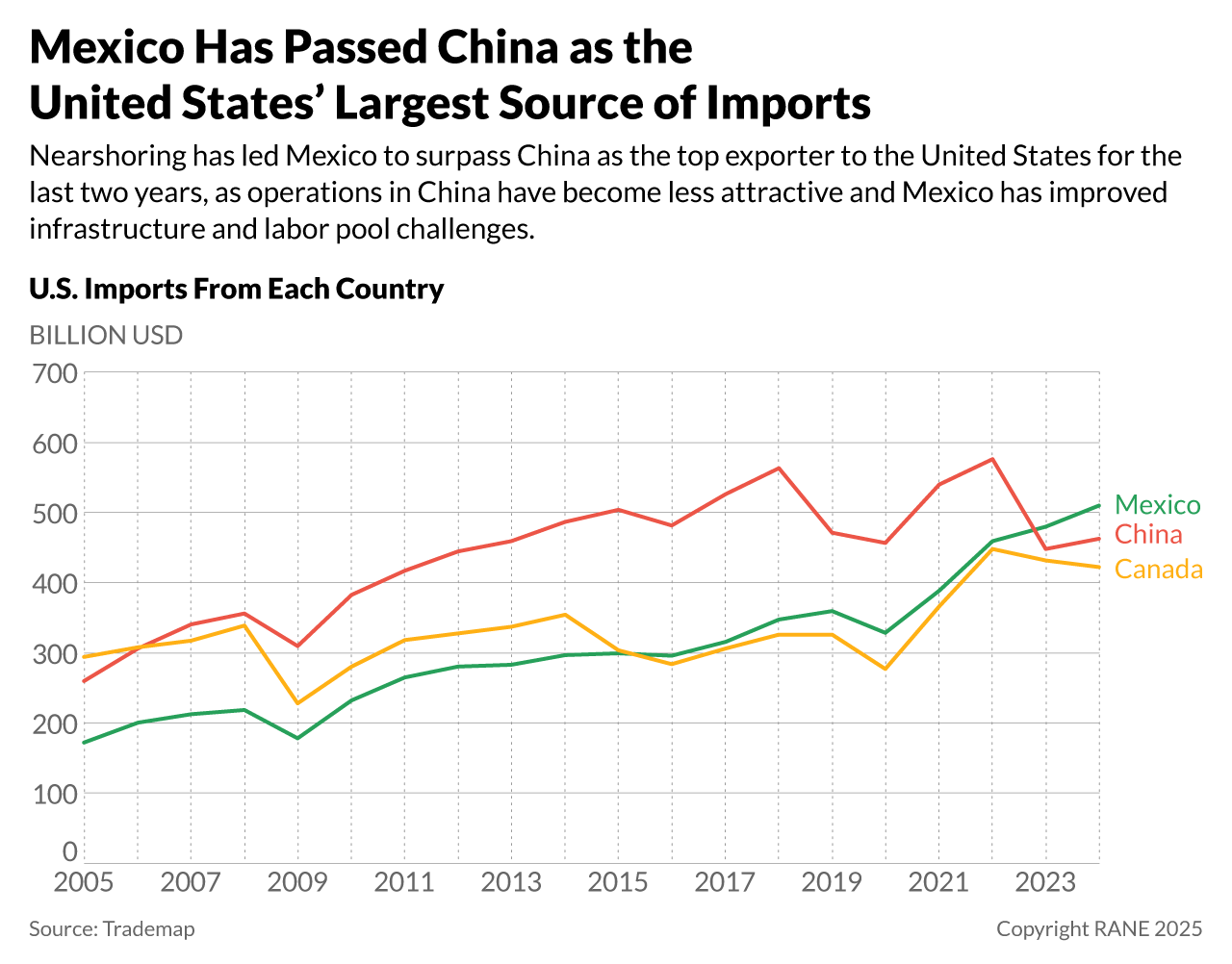

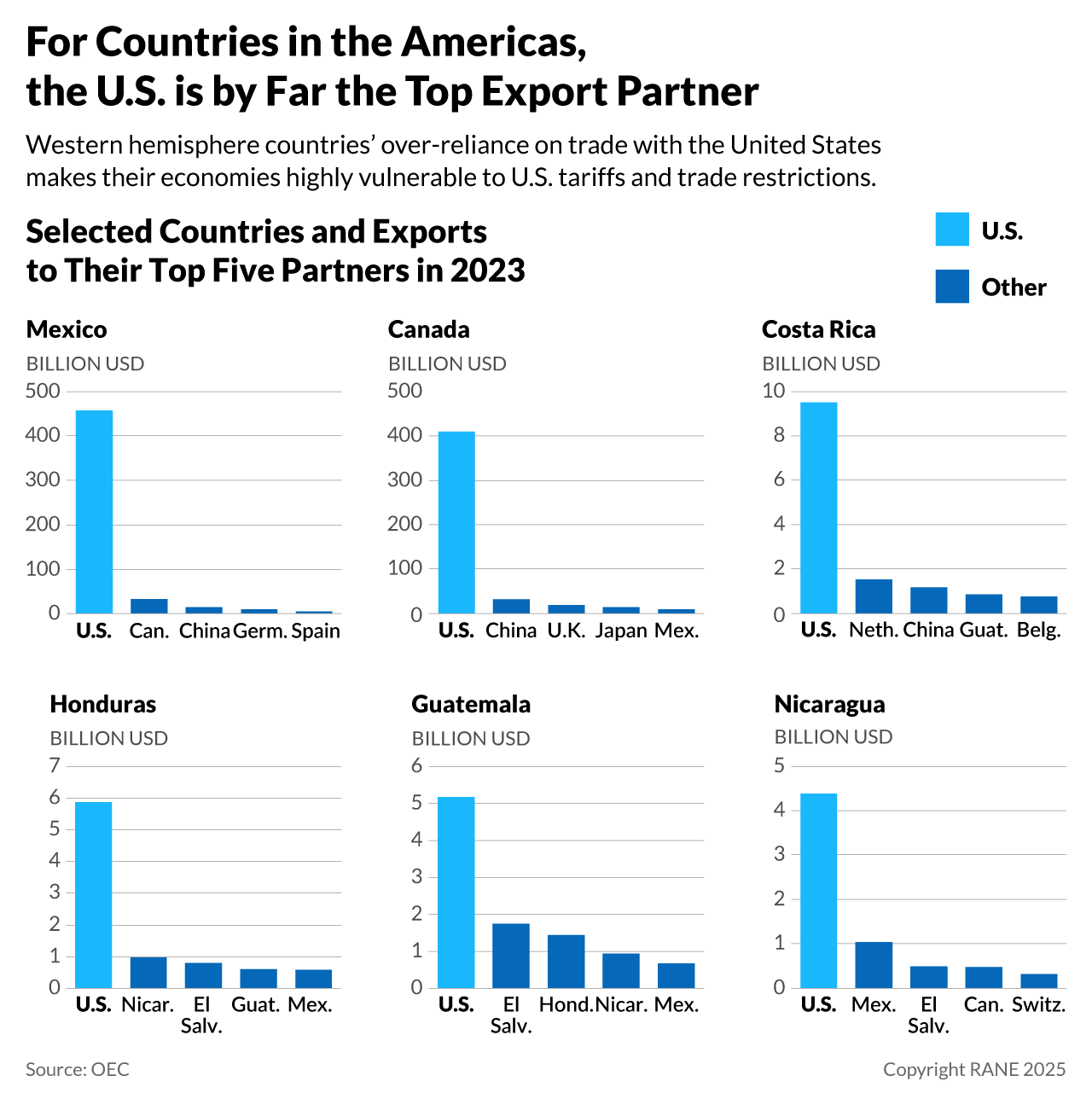

Trump administration policies will create new challenges for nearshoring manufacturing closer to the United States, but a reversal that substantially damages major manufacturing countries' attractiveness for nearshoring is unlikely. In 2023, Mexico surpassed China as the top exporter to the United States for the first time in decades, a position Mexico held for the second year in a row in 2024. Canada, for its part, is the largest recipient of U.S. exports (though China exports a larger amount to the United States), illustrating the deep interconnectivity of North American supply chains and, amid broader shifts in global trade, pointing to an ongoing uptick in manufacturing in parts of the Western Hemisphere to supply the U.S. market. Nonetheless, U.S. President Donald Trump's tariffs on Canada and Mexico, even if narrowed compared to their original imposition, are generating growing uncertainty about the attractiveness of these and other regional countries for nearshoring, especially as Trump threatens further tariffs that would also hit Canada and Mexico, among other countries. Trump's other trade-related threats — such as to significantly renegotiate, or potentially even leave, the United States-Mexico-Canada Agreement (USMCA) — are only adding to this uncertainty, as the White House seeks to reshape global trade and increase domestic manufacturing.

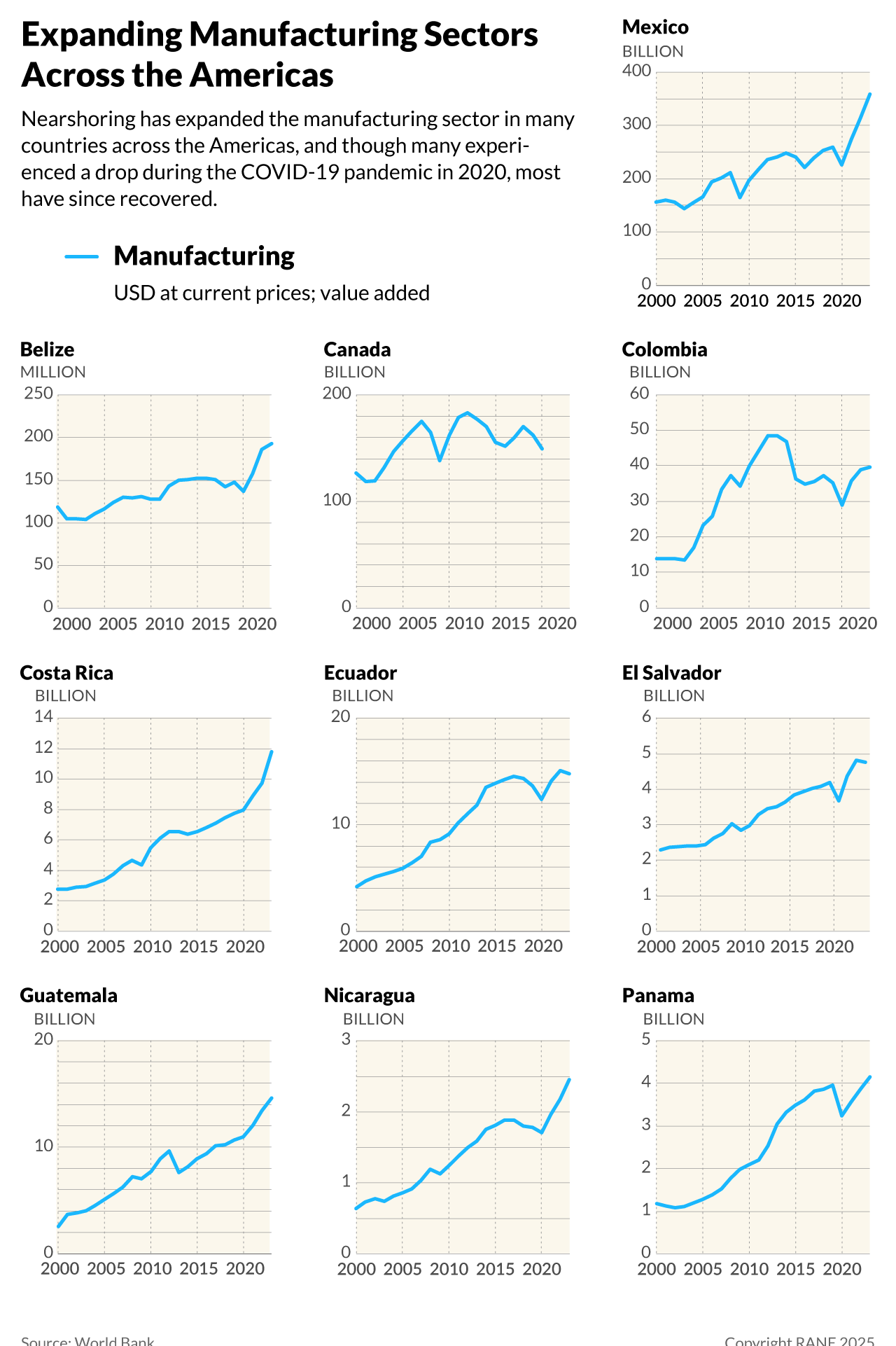

Multiple factors have driven nearshoring closer to the United States, including rising manufacturing costs in Asia (especially China), the growing attractiveness of operations in the Americas (especially Mexico), and Washington's expanding push for more resilient and secure supply chains. Due to proximity, shipments from Central American countries or Mexico reach the United States much faster than those coming from Asian countries like China, which provides significant cost benefits and makes supply chains more efficient. Nonetheless, for decades, manufacturers focused on expanding their supply chains in China and other Asian countries due to cheap labor, their larger pool of skilled workers, and better production capacity and infrastructure. But in recent years, these benefits have eroded. First, rising production costs in Asia due to increasing wages and energy costs have meant that while countries like China remain more cost-effective for manufacturing than the United States and Canada, they are now less competitive than countries in Latin America, such as Mexico. Second, Mexico and select other countries in the Americas have improved their availability of skilled workers and infrastructure. More recently, the U.S. government has pushed for more diversified and resilient supply chains, specifically away from China amid rising tensions with the United States. To help achieve this, Washington has expanded investment in Latin American countries to overcome local challenges that make manufacturing unattractive. This has included investments in education programs to assist with the low level of skilled workers, as well as security assistance to tackle high levels of organized crime and corruption. Furthermore, expanded investment by foreign companies has provided Latin American governments with funds to improve infrastructure capabilities. Finally, free trade agreements between the United States, Canada and Mexico have allowed certain products to enter the United States with no import taxes, bolstering the attractiveness of manufacturing in North America. These agreements include the North American Free Trade Agreement (NAFTA), which took effect in 1994, and its successor, the USMCA, which took effect in 2020 and continues the free trade environment established under NAFTA, albeit with more restrictions, including with regard to labor rights, environmental protections, and intellectual property. The USMCA has substantially increased trade in North America and has specifically bolstered nearshoring to Mexico.

- China Briefing reported in 2022 that while average wages in the manufacturing sector in China were $840 per month in 2022, they were only $480 in Mexico.

- Demonstrating the expansion of U.S. private sector investment in Latin America, foreign direct investment (FDI) stock from the United States to Latin America increased from $556 billion in 2007 to $1.065 trillion in 2023. According to the U.S. Congressional Research Services, countries in Latin America and the Caribbean received a total of 16% of U.S. FDI abroad in 2024.

- The USMCA has generated $1.8 trillion in total trade, supporting 17 million jobs across North America as of 2024, according to the Brookings Institution.

The United States has also promoted nearshoring by making China less attractive for manufacturing operations, including through sanctions, tariffs and trade restrictions. In addition to natural changes in the economics of manufacturing in China that have dented its appeal, U.S. trade restrictions on China have further incentivized manufacturers to move their operations closer to the United States. These include U.S. export controls preventing the shipment of high-tech products to China (limiting companies' ability to make certain products in the country), U.S. efforts to crack down on Chinese imports using anti-dumping rules, and U.S. tariffs that have increased the cost of a range of Chinese goods. The U.S. Uyghur Forced Labor Prevention Act, despite being primarily focused on human rights in China's western Xinjiang province, has also created additional compliance challenges for businesses operating in China by requiring them to ensure their products contain no components made in Xinjiang. In addition to these tools making China less attractive for production, their growing usage indicates to companies the U.S. government's willingness to expand restrictions in the future in response to further developments that worsen tensions, such as if concerns of a Chinese invasion of Taiwan grow. This signals to private sector organizations that challenges in China will continue to worsen, further necessitating the diversification of their supply chains. Finally, due to both human rights concerns and elevated anti-China sentiment in the United States and other Western countries, there are elevated reputational risks for companies manufacturing in China, creating concerns that they will face criticism from both Western populations and governments over the coming years.

- A survey by the American Chamber of Commerce in Shanghai published in September 2024 indicated that only 47% of U.S. firms were optimistic about the five-year outlook for their operations in China, a five-point percentage drop from 2023 and the weakest level of optimism since the annual survey launched in 1999.

- While companies currently sourcing manufactured goods from China are not leaving the country en masse, evidence suggests organizations are choosing to put new manufacturing operations in other countries. Demonstrating this, the U.S. State Department's 2024 Investment Climate Statements on China found that while the country remains one of the largest recipients of FDI in the world, inbound FDI dropped 13.7% from 2022 to $163 billion.

- Growing trade restrictions from the United States and other Western countries have also prompted China to impose its own retaliatory measures. While typically narrower by comparison, these Chinese measures have still made it less appealing for Western manufacturers to source products from China. For example, in February 2025 following Trump's initial imposition of U.S. tariffs on China, the Chinese government announced its decision to add clothing company PVH Corp. (owner of Calvin Klein and Tommy Hilfiger) to its ''unreliable entities'' list, which allows Chinese authorities to impose fines, prohibit import and export activities, and deny employees the ability to enter China.

However, new U.S. tariffs on Canada and Mexico — and the Trump administration's threats to impose more — are now casting doubt on the future of nearshoring. On March 4, President Trump made good on his threat to impose 25% tariffs on all goods from Canada and Mexico (with the exception of Canadian energy resources, which were hit with a smaller 10% tariff). The White House later announced a one-month tariff exemption for the auto industry on March 5 and, after calls between Trump and Mexican President Claudia Sheinbaum and Canadian Prime Minister Justin Trudeau, a one-month exemption for goods covered under the USMCA. Despite the delays and exemptions, Trump's imposition of the tariffs, even after acknowledging the harm they would cause to the U.S. economy, indicates his intent to impose a broad range of tariffs as a way to both pressure foreign governments and reduce the United States' trade deficit with targeted countries. While the tariffs were initially announced in response to U.S. complaints over fentanyl and migration flows across the Mexican and Canadian borders, the Trump administration has voiced a range of other motivating factors for the measures. Trump has said the current one-month exemptions are the last ones, but he has previously made similar statements, so it is unclear if this will hold true. There is also uncertainty regarding how long the tariffs will remain in place. But over time, the tariffs would significantly increase the cost of Mexican and Canadian goods (both finished products and inputs) sold in the United States, damaging their competitiveness and reducing the attractiveness of Canada and especially Mexico as manufacturing destinations, undermining nearshoring trends. Furthermore, the Canadian and Mexican governments have threatened to impose retaliatory tariffs, a move that would further undermine the attractiveness of nearshoring by reducing the benefits of USMCA and increasing the cost of even U.S.-made goods if they use Mexican and/or Canadian components, as many electronics, automotives and various other products currently do.

- On Feb. 13, Trump released his administration's plan to impose reciprocal tariffs to match the tax rates that foreign countries put on their imports, announcing investigations into a range of sectors to determine the scale of sector-specific tariffs. On March 7, Trump warned that the United States could impose reciprocal tariffs on dairy and lumber products from Canada within the following week.

Uncertainty over the future of the USCMA and the Americas' broader economic outlook add to pressures on nearshoring. The USMCA has a clause that requires it be reviewed and approved by all three countries every six years, with the first review required by July 2026. Though Trump approved USMCA during his first term, he has repeatedly criticized it over the last year and has said he plans to renegotiate the agreement during the 2026 review. This negotiation process will likely focus on reducing the U.S. trade deficit with Canada and Mexico, with specific attention to the automotive industry and with the ultimate goal of increasing manufacturing within the United States. During this process, the Trump administration may determine that it is not receiving enough concessions from Mexico and Canada, leading the United States to exit the USMCA altogether despite the extensive benefits the deal provides to the U.S. economy. This development would eliminate one of the major drivers of regional trade growth over the last three decades. Separately, but illustrating the same trend of greater uncertainty over the future of nearshoring, U.S. threats to place tariffs and sanctions on Colombia over a migrant deportation dispute in February additionally indicate that countries across Latin America (and the world) will be at risk of tariffs in retaliation for their perceived failure to meet the Trump administration's varying demands. This, in addition to the unclear outlook for USMCA, creates uncertainty for companies considering where to place their sourcing operations, which may make countries with governments seen as more at odds with the Trump administration (such as Brazil) unattractive for FDI and manufacturing operations in the next few years, further reducing drivers for nearshoring.

- USMCA includes requirements that the automotive sector must manufacture 75% of its vehicle content within North America to qualify for the deal's trade benefits.

Trump administration policies are creating more uncertainty surrounding the future of regional aid programs that have supported nearshoring as well. Despite vast improvements that have driven a major uptick in manufacturing investments, there are long-standing, ongoing challenges for nearshoring in Mexico and elsewhere across the Western Hemisphere, with high crime levels and related government corruption creating challenges for businesses. Violence makes some areas infeasible for manufacturing facilities, extortion increases operating costs, and the potential that local staff are bribing officials to accelerate bureaucratic processes creates compliance concerns. In some parts of Mexico, Costa Rica, Guatemala, Colombia, Ecuador and Peru, these challenges have only worsened in recent years, hindering these countries' ability to attract more FDI. U.S. funding for programs to support counter-corruption and democratization efforts has been uneven at best. But for many countries, U.S. funding to support counter-crime efforts has been central to boosting local security forces' resources and capabilities; while this does not necessarily assist in substantially reducing crime, it often helps to keep the most severe levels of violence at bay. However, Trump's effective suspension of the vast majority of funding for United States Agency for International Development (USAID) programs and planned efforts to further reduce foreign aid over the coming years as the Trump administration seeks to reduce government spending are weakening programs aimed at improving local education levels and reducing crime and corruption, broadly undermining the operating environment for companies. There remain significant uncertainties regarding if and when USAID funding will resume, but there have already been many reports of programs across the Americas pausing activities, laying off staff, narrowing operations and, in some cases, completely closing; if the cuts are not reversed or filled by alternative donors (the latter of which does not seem likely), it will risk allowing crime and corruption to worsen and reversing trends of expanding skilled worker pools and infrastructure modernization. While backsliding on these issues will not make Mexico and other Latin American countries completely unattractive for new investment, it will add to broader challenges that companies consider when determining where to locate new manufacturing operations.

- According to the Congressional Research Service, the administration of former U.S. President Joe Biden requested $2.2 billion for foreign assistance funds for the Latin America and Caribbean regions for use by the State Department and USAID. The budget request noted that the funds would prioritize countering narcotics trafficking, supporting democracy and human rights, cooperating in countering authoritarian threats, and offsetting regional migration. Though the Trump administration reported it was unfreezing funds for security programs, recipients continued to report that they did not have access to the funds as of late February, suggesting that there are ongoing bureaucratic hurdles even for funds excepted from Trump's foreign aid freeze.

- NGO Transparency International has long reported that countries in Latin America and the Caribbean experience among the worst levels of corruption in the world. In the organization's 2024 Corruption Perceptions Index, which measures perceptions of public sector corruption globally, out of 180 countries (in which a higher rank indicates worse levels of corruption) Mexico ranked 140, Guatemala ranked 146, Panama ranked 114, and Colombia ranked 92 — illustrating a sampling of the high regional corruption risks.

Despite likely dampening some countries' attractiveness to nearshore manufacturing, a reversal in nearshoring trends is unlikely as broader global dynamics mean major manufacturing destinations in the Americas will remain comparatively attractive for companies' sourcing operations. While Trump will continue to threaten and likely impose new tariffs against Mexico, Canada and other countries in the Western Hemisphere over his four-year term, the resulting backlash from the business community and increased consumer prices within the United States mean they will likely be narrowed (or in some cases fully removed). Demonstrating this, while Trump acknowledged in his March 4 address to the U.S. Congress that tariffs could cause economic pain within the United States, his move to later implement exemptions for tariffs indicates that concerns about the economic impact of tariffs against the two largest U.S. trading partners can affect his decisionmaking. In addition, it will likely be easier for Western Hemisphere countries to work with the Trump administration to have tariffs reduced or removed as Trump's greater trade and tariff focus will remain on China due to broader national security priorities. Demonstrating this, the Trump administration reportedly previously pressured Mexico and Canada to impose tariffs on China in order to avoid tariffs on their goods, suggesting that Trump is more focused on reducing the presence of Chinese components in products that enter the United States than decreasing trade with the United States' neighbors; members of the Trump administration ultimately walked back this demand, but the fact that it was voiced in discussions suggests it may resurface in future negotiations. Separately, the Trump administration is threatening to impose tariffs on a broad range of countries, including reciprocal tariffs. While countries in the Western Hemisphere will also face such threats, if comparable levels of U.S. tariffs are placed on countries across the board, including those with large manufacturing sectors in Southeast Asia, countries like Mexico will remain comparatively attractive due to their proximity to the United States and lower logistics costs. And so long as the USMCA remains in place and the Trump administration continues to provide exemptions for specific products, such as the automotive sector, the incentives for manufacturing in Canada and Mexico will remain. Due to these dynamics, challenges to nearshoring will likely only result in a more moderate slowdown in investment and manufacturing sector growth in Mexico and other Latin American countries that have recently attracted more manufacturing investment, such as Costa Rica, Panama, El Salvador and the Dominican Republic. It will also be unlikely that trends reverse and that companies begin pulling substantial investments out of the region. Furthermore, Canada's comparatively advanced infrastructure and workforce will mean the country remains an attractive destination for the manufacturing of higher-end goods, including in the aerospace sector. However, a broader drop in consumption in the United States due to tariff-related inflation and efforts among some to shift new manufacturing into the United States will likely slow the expansion of manufacturing operations, at least through the end of 2026, when companies will likely have a better idea of the scale of U.S. tariffs and trade restrictions. Furthermore, as businesses will be more hesitant to invest in countries facing more pronounced infrastructure challenges, many in the region, such as Nicaragua and Bolivia, will struggle to attract new investment, preventing them from attracting needed new jobs and funding.

- The Trump administration reportedly initially broached the topic of Mexico imposing tariffs on Chinese goods in exchange for avoiding U.S. tariffs on its goods during a Feb. 20 meeting, which President Sheinbaum later said her government was considering. On Feb. 28, U.S. Treasury Secretary Scott Bessent said that both Canada and Mexico should match U.S. tariffs on Chinese goods.

Indicators for Worsening Nearshoring Challenges

While a major decline, let alone reversal, in nearshoring to current major manufacturing destinations in the Americas is unlikely, it remains possible — particularly given the lack of clarity on whether Trump is using tariffs solely as a method to alter the policies of foreign governments on key issues, or if the tariffs themselves are the ultimate goal as part of Trump's broader effort to structurally change global trade over the longer term. If they occur, the following developments would demonstrate that risks to the attractiveness of nearshoring are becoming more severe:

- The 25% U.S. tariffs on Mexico and Canada remain in place for more than two months (when price increases in the United States will likely be felt), with Trump also threatening to impose additional tariffs targeting the two countries.

- Trump imposes higher tariffs on countries across the Americas in retaliation for their domestic policies, particularly left-wing governments viewed as not politically aligned with his administration, such as those in Colombia and Brazil.

- U.S. relations with Canada and Mexico significantly deteriorate, with regular rhetorical clashes between governments and discussion of reducing diplomatic relations.

- The United States leaves the USMCA, or the Trump administration renegotiates the trade agreement in a way that substantially weakens it.

- Multiple Latin American countries' manufacturing sectors contract.

- The United States does not re-implement canceled USAID programs.

- The Trump administration does not impose tariffs on major manufacturers in Asia, such as Vietnam and Thailand, or imposes substantially lower tariffs on these Asian countries than those on Mexico, Canada and other countries in the Western Hemisphere.

- U.S. FDI to Latin America and the Western Hemisphere drops, falling below $1 trillion.

- U.S. imports from a major trade partner such as Canada or Mexico drop by over 10% in a year.

The expansion of manufacturing operations provides benefits to Latin American countries and for companies operating in the region; a significant reversal of that expansion would thus worsen poverty rates, create regional political instability and reduce investment attractiveness for businesses. Many middle- and low-income countries across Latin America have experienced significant benefits as a result of nearshoring trends, including in particular Costa Rica, Panama and Guatemala. Though the region experienced major economic setbacks during the COVID-19 pandemic, with a majority of countries experiencing recessions that led to a resurgence in poverty levels, countries that have successfully integrated into supply chains for the United States have since recovered and are benefiting from expanding exports of manufactured goods to the United States. According to the United Nations, regional poverty levels fell to a 33-year low in 2023, to 27.3% of the population, down from 30.1% in 2015. While economic inequality and high levels of extreme poverty remain a concern, nearshoring has expanded formal economic job opportunities for the Latin American populations (though not always evenly distributed) and has provided funds for governments to improve education and other social programs. However, the region remains highly vulnerable due to its countries' high economic dependence on the United States as an export destination. For now, manufacturing operations are poised to keep growing as U.S. purchasing power remains strong. This will continue to benefit major manufacturing countries in Latin America, enabling them to further reduce the challenges that currently hinder investment, including poor infrastructure, high crime, widespread corruption and a low level of skilled workers. But if the expansion of manufacturing operations slows substantially or begins to reverse, such as in a more severe scenario in which the Trump administration takes more extreme actions to reduce imports, the impact would be devastating for many regional economies. Countries across Latin America would likely see an uptick in poverty rates, while higher unemployment levels would trigger greater frustration with regional governments, leading to an increase in unrest and, in some cases, organized crime. If instability rises, logistical challenges for businesses would also rise, making some countries less attractive for manufacturing and sourcing operations, subsequently further reducing FDI.