Editor's Note: This article is the seventh installment in an ongoing RANE series on the shifting patterns of global trade. The first installment provided a broad overview of the geopolitical and economic implications of these shifts. The second examined how recent changes to U.S. trade and tariff policies will affect nearshoring trends in Canada, Latin America and the Caribbean. The third assessed how rising tensions between Israel, the United States and Iran could impact shipping in the Strait of Hormuz. The fourth installment assessed how U.S. reciprocal tariffs will have major economic and political impacts on Japan and South Korea, particularly as both East Asian countries prepare for summer elections. The fifth discussed India's evolving trade strategy of boosting key exports while protecting sensitive sectors. And the sixth assessed that Turkey's trade diversification strategy will continue to hinge on neutrality.

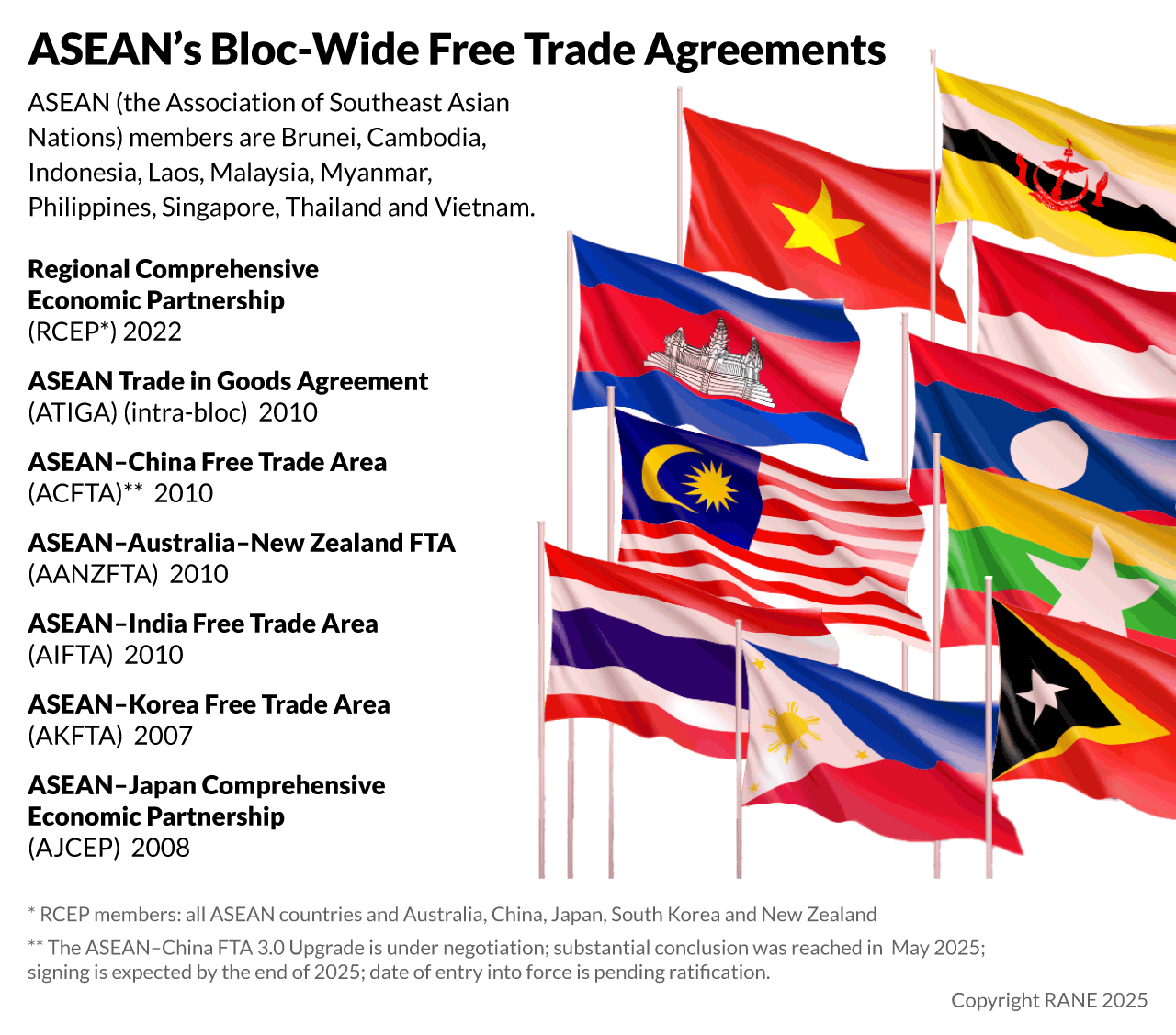

While the Association of Southeast Asian Nations (ASEAN) is attempting to use global trade tensions to strengthen economic integration, the bloc's diversity will limit the extent of this effort even as, over time, common concern about export dependencies on the United States will drive ASEAN members to seek alternative trading partners. On May 26-27, Malaysia, as the 2025 ASEAN chair, hosted a series of summits that underscored ASEAN's broad dual-track initiatives to bolster intra-bloc trade and trade diversification. The 46th ASEAN Summit, convened on May 26, brought together leaders from the ten-member bloc and produced a new five-year strategic plan aimed at deepening economic integration among member states, with goals such as further harmonizing trade standards, enhancing financial integration and promoting sustainable economic practices. Leaders also committed to finalizing an upgraded ASEAN Trade in Goods Agreement by October, which aims to further liberalize regional markets and boost intra-ASEAN trade beyond its current share of 20-24% of the bloc's total. Additionally, ASEAN leaders finalized the Digital Economic Framework Agreement, which seeks to harmonize regional digital trade rules and facilitate cross-border data flows, thereby strengthening intra-bloc digital integration. In parallel, ASEAN announced the completion of negotiations for the ASEAN-China Free Trade Area 3.0 upgrade, with formal ratification and signing also likely later in 2025. Moreover, on May 27, Malaysia hosted the second biennial ASEAN-Gulf Cooperation Council (GCC) Summit and the inaugural ASEAN-GCC-China Summit. These meetings aimed to bolster economic relations across China, Southeast Asia and the Gulf Arab regions, with discussions focusing on enhancing trade, investment and infrastructure development, while also laying the groundwork for future trilateral cooperation.

- The upgraded ASEAN Trade in Goods Agreement will introduce paperless customs procedures, harmonize technical standards, reduce non-tariff barriers and expand support for small businesses.

- The ASEAN-China framework will expand cooperation into emerging sectors, such as digital and green economy investment, enhance supply chain connectivity, and support sustainable growth.

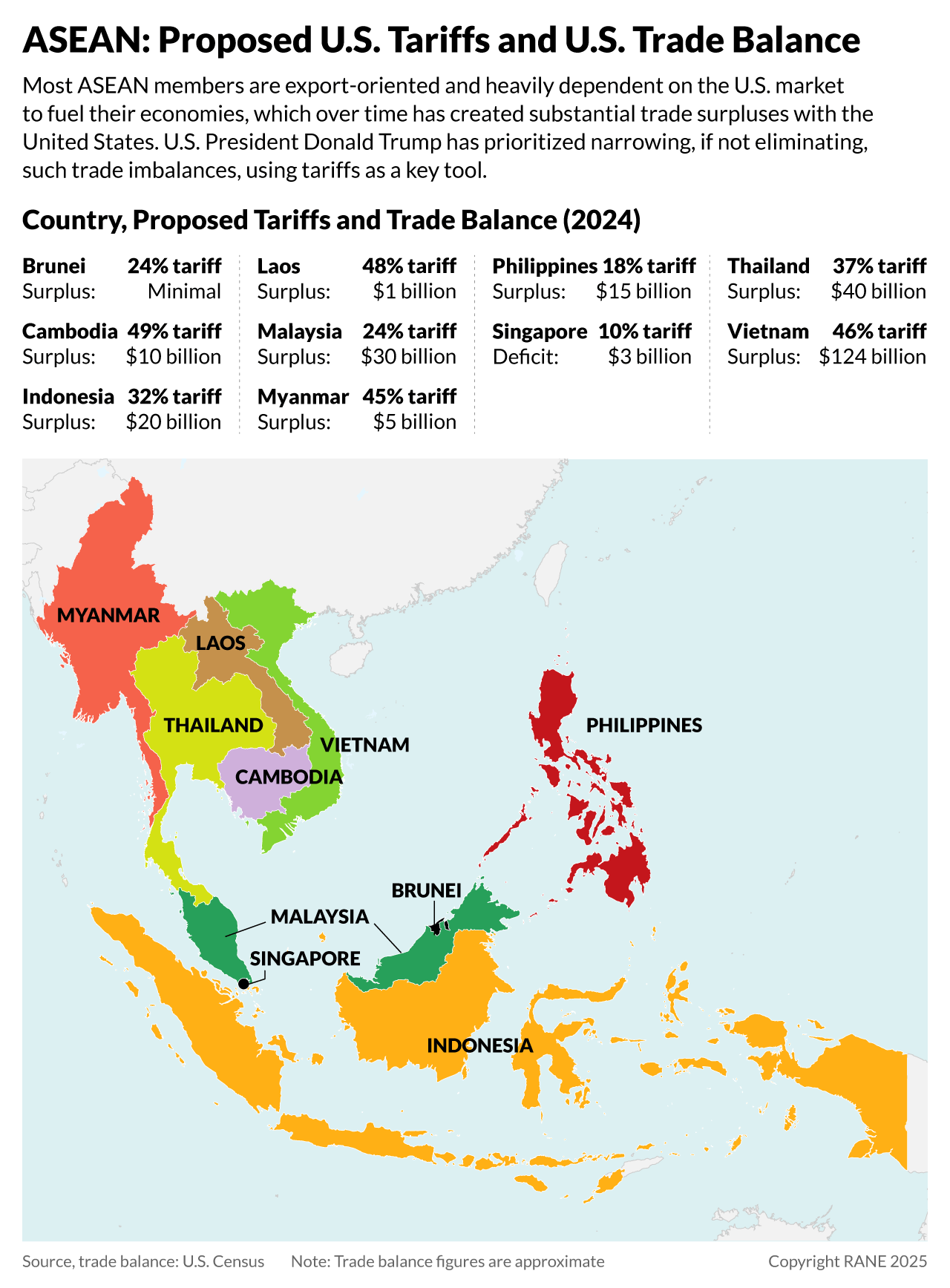

The urgency behind ASEAN's recent trade diplomacy stems from the impending full implementation of sweeping U.S. tariffs above the 10% baseline rate in early July. The recent summits highlighted ASEAN's efforts to diversify economic partnerships in light of rising U.S. protectionism and shifting global trade dynamics, as discussions emphasized opportunities for market synergy and the promotion of cross-regional investment — both of which are particularly relevant to trade. This proactive approach is largely a response to the steep "Liberation Day" tariffs announced by U.S. President Donald Trump in early April, which propose steep duties, some as high as 49%, on imports from most ASEAN countries. The White House paused those higher tariff rates for 90 days, with ASEAN states currently all facing a baseline 10% tariff rate. However, the looming July 8 expiration of the suspension has galvanized ASEAN to accelerate regional economic integration and broaden its trade partnerships. In doing so, the bloc is hoping to build resilience against external shocks and maintain economic stability once the higher U.S. tariffs take effect, which threaten to significantly (and perhaps catastrophically) disrupt established supply chains, reduce export revenues and hinder economic growth in Southeast Asia. This is because Trump's tariffs affect key sectors such as electronics and textiles, which are crucial to export-driven ASEAN economies and their governments' efforts to move up the manufacturing value chain to rise above middle-income status. Among ASEAN countries, Cambodia and Vietnam will be hit particularly hard because they face among the highest U.S. tariff rates and are also heavily reliant on exports to the U.S. market.

- Malaysian Prime Minister Anwar Ibrahim has called for a U.S.-ASEAN summit with President Trump to discuss the tariffs and protect the region's collective economic interests. The White House has yet to acknowledge this call.

- The Trump administration's "Liberation Day" tariffs were calculated based on each country's trade surpluses with the United States, with larger surpluses translating to higher tariffs. For example, Vietnam, which had a substantial trade surplus of $123.5 billion with the United States as of 2024 (which has only widened since), faces a proposed tariff rate of 46%, the third highest in ASEAN behind Cambodia (49%) and Laos (48%).

- Exports to the United States comprised 38% of Cambodia's total exports in 2024, and generated roughly 30% of Vietnam's GDP last year.

ASEAN member states continue to stress unity in the face of U.S. tariffs, but limited coordination mechanisms and divergences in economic exposure and domestic political calculus are driving most countries to pursue bilateral trade talks with Washington. ASEAN leaders have emphasized the need for a unified approach to mitigate the adverse effects of U.S. tariffs, though there are limited options, if any, to actually achieve this. As 2024 ASEAN chair, Anwar has warned that fragmented responses risk weakening the bloc's collective leverage and setting a dangerous precedent for future economic coercion. Indeed, his push for a U.S.-ASEAN summit reflects a belief that, while each country faces different levels of vulnerability, the structural threat posed by broad U.S. tariffs is shared. But such a summit is unlikely to materialize. Politically, the proposal has drawn rhetorical support but little binding alignment as each ASEAN state is prioritizing its own protection, at times at the expense of other members. Economically, countries like Vietnam and Thailand that have large trade surpluses with the United States are too exposed to delay mitigation efforts, while lower-income members like Cambodia and Laos lack the bargaining power to offer meaningful concessions to Washington. Singapore and Indonesia, each with unique leverage and exposure, are pursuing individual strategies shaped more by pragmatic self-interest than bloc discipline. Without enforcement mechanisms or shared legal instruments to structure a coordinated response, ASEAN's cohesion beyond intra-bloc agreements, such as regulatory harmony and reduced trade barriers, remains largely aspirational. Still, partial coordination — such as shared fallback options via trade agreements with other entities (like the GCC), or agreed norms on non-interference (as seen at the May summit) — could set meaningful precedent and help keep the idea of so-called ASEAN centrality in the emerging multipolar order. This means the bloc could still retain its role as a convening platform and regulatory reference point in regional trade in the face of disruptive U.S. tariffs, even if it cannot shape outcomes or negotiate as a unified economic actor.

- ASEAN centrality refers to the principle that the bloc should remain the convening hub and normative anchor of regional cooperation, shaping multilateral engagement through its platforms, processes and agenda-setting role. Though consensus has been reached among member states on this objective, the aspiration has long been constrained by structural asymmetries and divergent national interests. Accelerating trade bifurcation and great power competition have only further exposed these limitations, threatening to dilute ASEAN's cohesion and relevance. Should commitment to the doctrine falter, ASEAN leaders fear the region will become increasingly vulnerable to great power competition and, ultimately, fragment into pro-U.S. and pro-China camps.

- The moves taken by individual ASEAN members in response to U.S. tariffs illustrate their divergent strategies. Indonesia initiated early trade negotiations with the White House in April, offering U.S. agricultural access and regulatory concessions to reduce its 32% tariff exposure. Vietnam has courted Trump personally, in part via high-visibility business ties, and has also offered to implement origin-verification reforms and increase its purchases of U.S. LNG and aircraft imports in exchange for tariff relief. Thailand has formed a task force focused on rebalancing trade, increasing U.S. imports and enforcing stricter rules of origin. Cambodia, meanwhile, has rejected U.S. accusations of facilitating transshipments of Chinese goods while pivoting toward Chinese backing.

Facing coordination challenges, ASEAN will likely focus on improving select internal mechanisms that build practical economic resilience without requiring deep political integration. While high-level regional strategies such as the upgraded ASEAN Trade in Goods Agreement and the Digital Economic Framework Agreement are underway, short-term progress is more likely in smaller-scale initiatives where consensus is easier and the cost of implementation is lower. These include technical harmonization in areas like digital customs clearance, mutual recognition of product standards, and localized currency settlement mechanisms between already-cooperative economies like Malaysia, Thailand, Indonesia and Singapore. Such steps, though limited in scope, can incrementally improve trade fluidity and reduce exposure to dollar-based transaction risks, like potential future Western sanctions on member states, exchange rate swings or U.S. dollar shortages. While not legally binding, precedent-based alignment could materialize through meetings among ASEAN finance ministers or ad hoc working groups, offering at least some signaling value to external partners. In parallel, infrastructure interlinkages, particularly in transport corridors and power grid connections, will continue advancing under subregional initiatives like the Singapore-Johor high-speed rail project, even as bloc-wide coordination remains elusive. Still, ASEAN's default to non-interference, absence of enforcement tools, and diverging growth models will continue to inhibit more ambitious steps, such as pooled procurement, common external trade representation or industrial policy coordination. Moreover, the export slate for ASEAN countries is not complementary to each other, as members produce many of the same goods and lack a large, affluent consumer base, which represents another constraint on integration. Internal efforts will thus remain adaptive rather than transformative. However, ASEAN may still be able to preserve its relevance as a decentralized but functional hub of intra-Asian supply chain activity, especially if these efforts are framed as being non-confrontational to the United States' trade agenda (e.g., by simultaneously enforcing intellectual property laws to Washington's satisfaction and agreeing to crack down on Chinese transhipments), thus lowering the likelihood of U.S. retaliatory measures. Additionally, deep political integration among ASEAN members — such as shared sovereignty or legal enforcement powers akin to those seen in the European Union — is neither realistic nor needed for such technical initiatives, which can advance through ASEAN's typical intergovernmental and soft consensus mechanisms.

- ASEAN's new Digital Economic Framework Agreement will likely be finalized in 2025 and will establish shared rules on data governance, cross-border e-commerce and digital payments among ASEAN members, creating the bloc's first binding digital integration framework and enhancing intraregional trade connectivity in high-growth sectors while also reducing reliance on the U.S. dollar.

If the United States implements the full suite of its threatened tariffs, the impact will immediately disrupt ASEAN's export-reliant economies and fuel intra-bloc splits. Vietnam, Thailand and Malaysia, with the highest trade surpluses with the United States, will be hardest hit, particularly in high-end manufacturing sectors like semiconductors and precision assembly, where price sensitivity and stable logistics are preeminent. This risks leading to significant economic disruption and forestalling additional investments in high-end manufacturing that ASEAN countries need to move up the manufacturing value chain (in addition to disruptions to lower-end manufacturing, such as Cambodia's garment and textile sector). The economic fallout would, in turn, heighten political pressure on governments and raise risks of labor unrest and attendant protest activity in affected sectors, and potentially more broadly should there be wider layoffs. Additionally, Western companies are already shifting their supply chains under pressure to "friend shore" (i.e., relocate production to politically aligned or lower-risk countries) — a trend that large U.S. tariffs would only accelerate. To this end, Chinese firms using ASEAN countries, like Vietnam, as transshipment or origin-masking hubs will encounter new regulatory hurdles as these countries crack down on said practice as a means to placate U.S. trade pressure. Despite firms hedging against exposure to U.S. protectionism, investment sentiment in Southeast Asia would likely remain strong, especially for non-U.S.-bound exports. But investors would probably start favoring countries more compliant with U.S. origin rules and thus less exposed to tariff risks. Politically, ASEAN cohesion would likely deteriorate further, as steep U.S. tariffs would drive high-surplus economies to intensify their bilateral mitigation efforts with Washington, while driving lower-income members to lean more heavily into Chinese support. Anwar's bid for bloc-wide coordination on securing U.S. tariff relief would lose momentum, and intra-ASEAN tensions could rise over perceptions of preferential treatment or undercutting. Externally, the wider Southeast Asian region would deepen engagement with China while seeking fallback partners such as Japan, the GCC and the European Union for diversified market access.

Alternatively, if the Trump administration ultimately reduces or withdraws its threatened tariffs, ASEAN's trade environment would stabilize, though regional countries would continue to seek alternative trade partners to reduce their exposure to future U.S. measures. There is a chance that the looming U.S. tariffs on ASEAN members will either be scaled back or abandoned, whether as a result of bilateral negotiations, legal challenges in the United States, or White House recalibration. In this scenario, countries like Vietnam and Indonesia that have already undertaken costly steps to mitigate their exposure to U.S. tariffs (e.g., by increasing U.S. LNG imports and undertaking defense deals with the United States at the risk of angering China), would likely still pursue hedging behavior and deeper trade diversification to avoid future exposure. ASEAN cohesion could modestly improve, as the urgency for bilateral carveouts would lessen and regional discussions could pivot back toward collective resilience tools and longer-term industrial policy alignment. High-end manufacturing prospects would rebound fastest in Malaysia and Thailand, where foreign investors would be more likely to renew postponed projects, given these two countries' relatively more advanced high-end manufacturing bases. Supply chains disrupted by tariff anticipation could partially recover, particularly in sectors like electronics, where ASEAN remains competitive relative to China. Still, the episode would leave a lasting imprint, as ASEAN governments will likely remain wary of U.S. volatility and seek to accelerate trade links with more predictable partners. This includes deeper engagement with the Asia-Pacific countries that are parties to the Comprehensive and Progressive Agreement for Trans-Pacific Partnership, expanded infrastructure ties with Gulf Arab countries and China, and renewed efforts to reach a free trade agreement with the European Union.

- On May 28, the U.S. Court of International Trade ruled against Trump's use of the International Emergency Economic Powers Act to implement the majority of tariffs he has so far imposed in his second term, including his sweeping "Liberation Day" tariffs. But a U.S. appeals court reinstated the tariffs the next day, highlighting the current legal uncertainty surrounding the measures. The rapid reversal also signals that court challenges are unlikely to provide durable relief from such uncertainty, especially as Trump is highly likely to use other trade powers to maintain his aggressive tariff policy.

In the coming years, ASEAN will continue diversifying its trade ties, particularly with China but also with the European Union, Japan, the GCC and select Latin American partners; but while these efforts will help the bloc hedge against overexposure to the United States, they will also face constraints and introduce new risks. The ASEAN-China Free Trade Area 3.0, which upgrades the bloc's existing trade agreement with Beijing, will serve as the most immediate vehicle for ASEAN states to redirect trade from the United States. The inclusion of digital trade facilitation, green investment and logistics integration in the deal reflects Beijing's willingness to accommodate ASEAN priorities. However, ASEAN states are still set to become increasingly dependent on Chinese demand, especially lower-income members like Laos, Cambodia and Myanmar, but even middle-income members like Malaysia and Thailand will likely increase reliance on Chinese project finance and consumer markets. Then there is the Regional Comprehensive Economic Partnership (RCEP), the world's largest trade agreement that encompasses all 10 ASEAN members, along with China, Japan, South Korea, Australia and New Zealand. The deal provides a comprehensive safety net for intra-Asian supply chains, reinforcing ASEAN's institutional centrality and ensuring the continuity of trade in parts, electronics and raw materials. Its rules of origin provisions and streamlined customs procedures are also increasingly vital as ASEAN firms adjust supply chains in response to U.S. tariff pressures. Additionally, five ASEAN members — Brunei, Malaysia, Singapore, Vietnam and, most recently, Thailand — are parties to the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), which also includes Australia, Canada, Chile, Japan, Mexico, New Zealand, Peru and the United Kingdom. Japan, which is already embedded in ASEAN's industrial base, will likely lead further investment flows through the CPTPP framework, particularly in advanced manufacturing and green infrastructure. ASEAN countries continue to engage bilaterally with the European Union as well, though Brussels' preference for trade deals with individual countries will limit the bloc-wide impact in the short term. That said, ASEAN's alignment with EU rules on sustainability and governance may eventually yield reputational benefits and long-term market access. The May ASEAN-GCC (where leaders agreed to initiate negotiations for a comprehensive free trade agreement) and ASEAN-GCC-China summits also indicate that Gulf Arab countries are emerging as long-term capital and energy partners for ASEAN, particularly in infrastructure and logistics. Moreover, ASEAN engagement with Latin American partners — especially Brazil and Chile but also Mexico — remains limited but is growing, with discussions centered on food security, energy and minerals cooperation. Overall, these overlapping efforts reflect ASEAN's intent to remain a flexible trade node. However, limited internal alignment, infrastructure disparities and political asymmetries among members (regarding governance systems, strategic alignment and foreign policy autonomy) will, along with the lengthy timelines often needed to achieve major trade agreements, limit the extent and pace of diversification in the near term.

- The CPTPP grants access to major developed economies such as Japan, Canada, Australia and the United Kingdom. With provisions on labor, environment and digital governance, CPTPP participation also enhances ASEAN firms' competitiveness in high-value sectors.

- ASEAN engagement with the Organization for Cooperation and Development is growing. Vietnam, Indonesia and Thailand all aspiring to join, and are aligning tax, transparency and regulatory standards to that end. Indonesia is the furthest along in this typically multi-year process.

- Indonesia's January accession to the BRICS bloc (which also encompasses Brazil, Russia, India, China, South Africa, Egypt, Ethiopia, Indonesia, Iran and the United Arab Emirates) could help ASEAN further diversify ties and attract new investment. But BRICS remains peripheral to the bloc's core trade architecture due to the grouping's limited cohesion and lack of integrated market access. Malaysia, Thailand and Vietnam are also BRICS "partner" countries but lack formal membership.

- The proposed ASEAN-GCC deal aims to increase bilateral trade to $180 billion by 2032, a nearly 38% increase over the $130.7 billion reached in 2023.

- Brazil opened a dedicated mission to ASEAN in Jakarta in 2024 and held its first ASEAN-Brazil Ministerial Meeting in October 2023, focusing on food security and renewable energy. Chile has expanded outreach to ASEAN through the Pacific Alliance since 2022, emphasizing trade and minerals cooperation. Mexico has participated in ASEAN-Latin America and Caribbean forums and is exploring engagement in the agriculture and digital economy sectors, though formal ties remain limited.