China's excess savings and investment — exacerbated by trade conflict with the United States — remain its greatest structural economic challenges, but Beijing, despite its fear of a further accumulation of domestic debt, retains the ability to partially offset any trade-related economic deceleration. The Trump administration has targeted China with broad tariffs, with most Chinese exports to the United States now facing duties of 55%, as well as broader sectoral restrictions. However, China's economy has continued to register strong economic growth. To be sure, the full impact of U.S. tariffs has not yet fully materialized. A further increase in U.S. tariffs targeting China remains possible, but in the context of increased uncertainty and higher tariffs, China has taken only modest measures to soften the impact of reduced exports on aggregate demand. This is despite the fact that, aside from declining exports, China's economy continues to suffer from excess savings and investment, which has translated into low consumer price inflation and outright producer price deflation, thereby increasing the real debt burden of the economy and financial vulnerabilities.

- The Chinese government has set a target of "around 5%" of annual real GDP growth for 2025. Q1 real GDP growth reached 5.4% year-on-year and 5.2% year-on-year in Q2.

- Chinese producer and consumer prices remain under downward pressure. In June, consumer price inflation increased 0.1% year-on-year after four months of year-on-year deflation. Producer prices have been in negative territory year-on-year since October 2022.

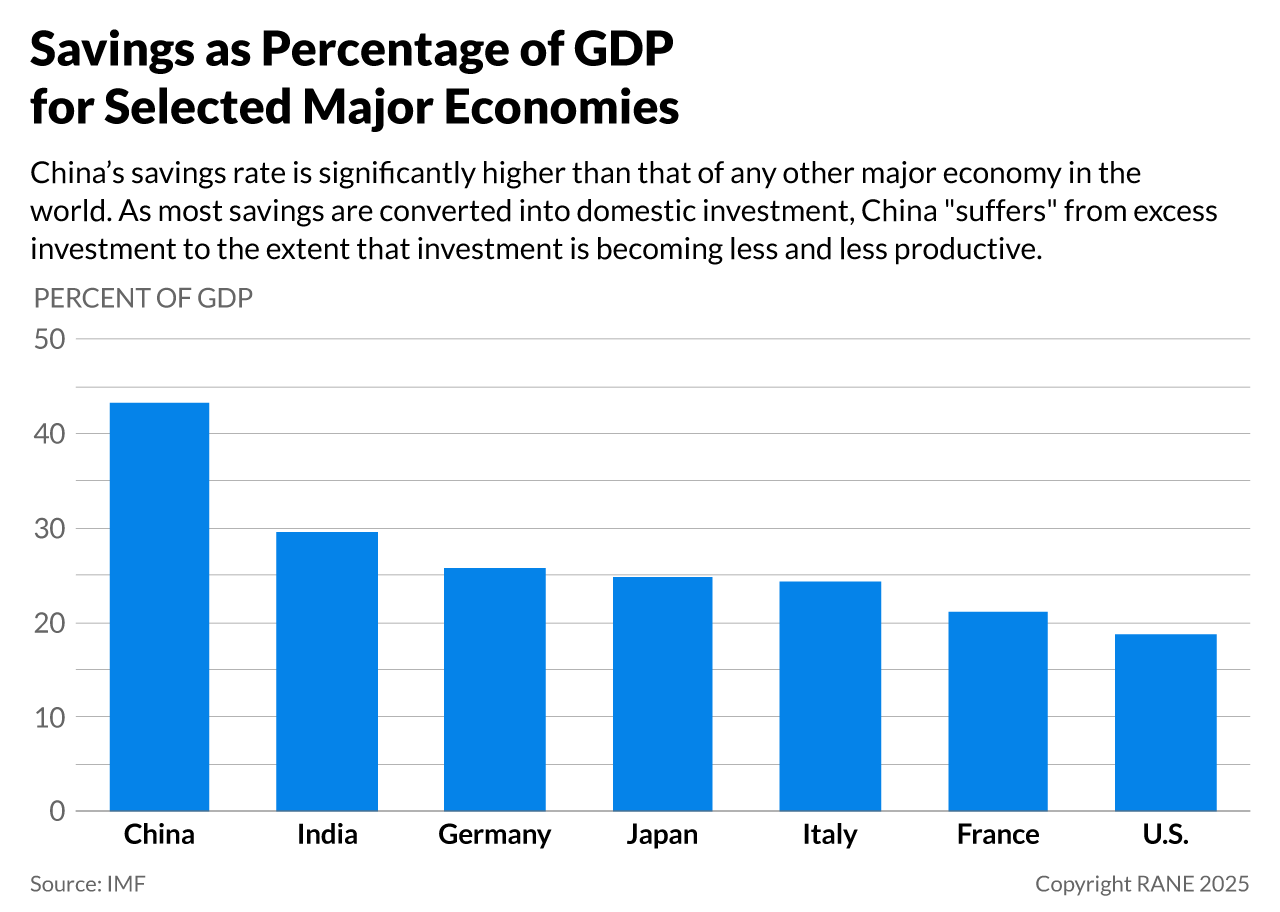

- China's domestic savings and investment rates exceed 43% and 41% of GDP, respectively. China's total social financing, a measure of total outstanding credit in the economy, exceeds 300% of GDP and is projected to increase further.

- Chinese exports to the United States were valued at $107 billion in February to May 2025, compared with $125 billion in February to May 2024.

The impact of U.S. trade restrictions targeting China will exacerbate its "excess savings" problem and further add to deflationary pressures. China depends less on exports than in the past, and high U.S. tariffs will be somewhat offset by the diversion of exports to third countries. Nonetheless, reduced exports will exacerbate already entrenched domestic producer price deflation in the short to medium term, while weaker economic growth will further weigh on consumer spending and consumer price inflation. While policymakers have voiced concern about intensifying producer price deflation, they have thus far only announced relatively modest measures to support prices (such as via consolidation of the polysilicon industry) or implement consumer-focused measures to support households. This has helped boost demand for certain categories of retail sales, but has not done much to increase domestic consumption. Structurally, the authorities have continued to channel excess savings into the so-called "new productive forces" — selected sectors including EVs — instead of increasing consumption. This has led to significant domestic overcapacity and sharply increased exports in certain sectors. Excess savings lead to a whack-a-mole situation, where the re-direction of savings from one sector, such as real estate, to another, such as EVs or technology, leads to excess supply and associated economic problems related to overinvestment, namely reduced profitability, deflationary pressure and financial vulnerabilities of borrowers. U.S. tariff measures will exacerbate this situation by reducing China's ability to export its excess savings and export production, thus putting downward pressure on domestic prices.

- Since January, U.S. tariffs on China have increased by roughly 30 percentage points, translating into average effective tariffs of 41% (as various exemptions pull down the average rate). The higher duties will lead to a reduction of Chinese exports to the United States, but the impact on Chinese aggregate demand will be manageable. Chinese gross exports of goods and services amount to 20% of GDP. Gross goods exports to the United States accounted for less than 2.5% of Chinese GDP. This is significant, but not excessive. The respective figures in terms of exports to the United States for Canada and Mexico are 20% and 30% of GDP, respectively.

- Various estimates put the immediate negative impact of recent U.S. tariffs at less than 1% point of Chinese real GDP growth. Discounting offsetting Chinese macroeconomic measures, this would translate into GDP growth of over 4%. The IMF has recently upgraded its forecast of China real GDP growth for this year to 4.8% due to a less damaging U.S. trade policy.

Beijing's ability to implement short-term measures remains adequate, even if policymakers would rather avoid providing significant stimulus given China's experience in 2008. Following the global financial crisis, Beijing launched a major credit-driven stimulus policy program. While it helped support economic growth, it also led to a significant increase in total debt, or total social financing, including household, corporate and public sector debt. This experience is a major reason why Beijing has so far been reluctant to pursue significant fiscal or quasi-fiscal demand stimulus. Another reason for Beijing's reluctance to introduce measures is that economic growth has held up thus far and central government is concerned about the downsides of vast additional consumer stimulus. Although Chinese public sector debt, including local government debt, is high, a relatively closed capital account and extensive control over the banking system — as well as further room to ease monetary conditions — mean that Beijing retains its capacity to support economic growth through short-term demand measures, if necessary.

- After downgrading China's growth forecast to 4.1% at the height of U.S.-Chinese trade tensions in April, JP Morgan revised its full-year 2025 forecast upward to 4.8%. Before the escalation of U.S.-China trade tensions, JP Morgan forecast growth of 4.6%. If these forecast are correct, this will limit the need for Beijing to launch significant demand stimulus in the near term.

- Even before U.S. President Donald Trump took office, Chinese policymakers had taken modest measures to support domestic consumption in the context of China's goal of rebalancing the economy away from excessive real estate sector investment.

If Chinese growth were to decelerate in the next few quarters, policymakers would respond by implementing further monetary and fiscal measures to support domestic demand, but Chinese policymakers remain unlikely in the near term to pursue broader structural economic reform. In theory, the bigger the projected economic slowdown, the greater the strength of any macroeconomic measures. While China's growth outlook for 2025 remains fair, more forceful measures from Washington, combined perhaps with a U.S. economic slowdown, could lead to a sizable, if manageable, real GDP growth slowdown to 4% or less. In this case, the Chinese authorities would take more forceful monetary and fiscal stimulus measures in order to avoid a further slowdown that would accelerate deflation and exacerbate financial sector problems due to an increasing real debt burden, including for local governments, which are already highly indebted due to their extensive low-yielding infrastructure investment and reduced real estate sector-related revenues. The People's Bank of China (PBoC) has scope to cut interest rates and is likely to do so if deflationary pressures intensify. Moreover, the central government, as opposed to cash-strapped local governments, is well-positioned to provide further short-term stimulus, much of which has so far been funded by so-called "ultra-long" special treasury bonds. If economic growth slows significantly, policymakers will provide further, if only modest, fiscal stimulus. Still, such measures will do little to address China's excess savings problems unless accompanied by broader reform aimed at a structural increase in household incomes and a reduction of precautionary savings (through government transfers) as well as a reduction of corporate savings (through higher taxes and reduced subsidies). Such reform remains unlikely in the short and medium term due to the need to manage the present, short-term economic and financial challenges, including the deleterious economic effect of aggressive U.S. trade policy.

- Chinese policymakers have begun to study the implications of a zero-interest rate policy, suggesting they are getting prepared for a further decline in interest rates and monetary easing, according to a July 2025 Financial Times article.

Over the long term, China will continue to seek to make itself less vulnerable to global economic instability, particularly hawkish and erratic U.S. economic policy, by reducing its dependence on foreign technology and limiting concentrated trade dependence and vulnerability to financial sanctions. In the context of intensifying geopolitical competition and the increasing use of trade restrictions and sanctions, Beijing is keen to reduce its vulnerability, particularly vis-a-vis the United States. Its so-called "dual-circulation" strategy seeks to increase domestic consumption and self-reliance while maintaining international trade. Other policy initiatives seek to loosen economic, financial and technological chokepoints. Beyond trade, Beijing will also continue to seek to establish alternative financial infrastructure to make China less dependent on the Western financial system and less vulnerable to Western sanctions. Beijing will continue to diversify its trade to reduce its vulnerability in the face of erratic and unfriendly U.S. trade policies, gradually making China less susceptible to U.S. economic pressure. In the meantime, more limited macroeconomic measures will help policymakers manage present trade-related instability.

- China remains keen to diversify its trade relations by supporting regional free trade blocs, including the CPTPP and RCEP. This will lead China to diversify its trade away from the United States and the European Union at the margin. Nonetheless, the U.S. economy remains the largest market for final consumption in the world, making it costly and difficult to completely replace.

- To reduce China's dependence on the dollar, Beijing has promoted the international role of the renminbi through its inclusion in the IMF's SDR basket, the establishment of an alternative financial clearing and settlement infrastructure in the guise of CIPS, the promotion of RMB through the AIIB and Belt and Road Initiative, as well as through PBoC swap lines.