Editor's Note: This article is part of an ongoing RANE series on the shifting patterns of global trade. The first installment provided a broad overview of the geopolitical and economic implications of these shifts. Other installments have examined trade patterns in the Americas, the Strait of Hormuz, Japan and South Korea, India, Turkey, ASEAN countries, the data flows, Mercosur, maritime chokepoints (part one and part two), digital trade and Congo. The first and second parts of our installment on East Africa can be found here and here.

Faced with the risk of U.S. financial sanctions, China and some other countries have sought to de-dollarize their international trade. While this will fragment the international trade financing regime to some extent, it will do little to undermine the position of the dollar as the preeminent international trade and finance currency over the next decade. Thanks to the size and liquidity of U.S. domestic capital markets, the dollar remains the preeminent currency used in international financial transactions. It also remains the dominant currency for international trade invoicing and settlement. Nonetheless, several governments have begun to make greater use of their own currencies to conduct international trade. China, in particular, has sought to internationalize the renminbi for many years with some success. Its efforts have accelerated following the imposition of U.S. and European financial sanctions on Russia. While the currency composition of global and Chinese foreign exchange reserves has remained relatively unchanged, central banks have sharply increased their purchases of gold since the start of the Russia-Ukraine war, suggesting a desire for increased diversification of reserve assets amid the threat of U.S. financial sanctions and, more recently, volatile U.S. economic policies.

- The dollar accounts for 58% of central banks' foreign exchange reserves. While this is down from 71% in 2001, it is slightly higher than in 1996. Central banks, particularly the People's Bank of China, sharply increased their gold purchases starting in 2022, when the Russia-Ukraine war began, with purchases (measured in tons) more than doubling in 2022-24, compared with 2016-21. Over the past five years, central banks have roughly doubled their holdings of gold as a share of their foreign reserve assets, for a total of about 25%, up from 10% in the late 2010s.

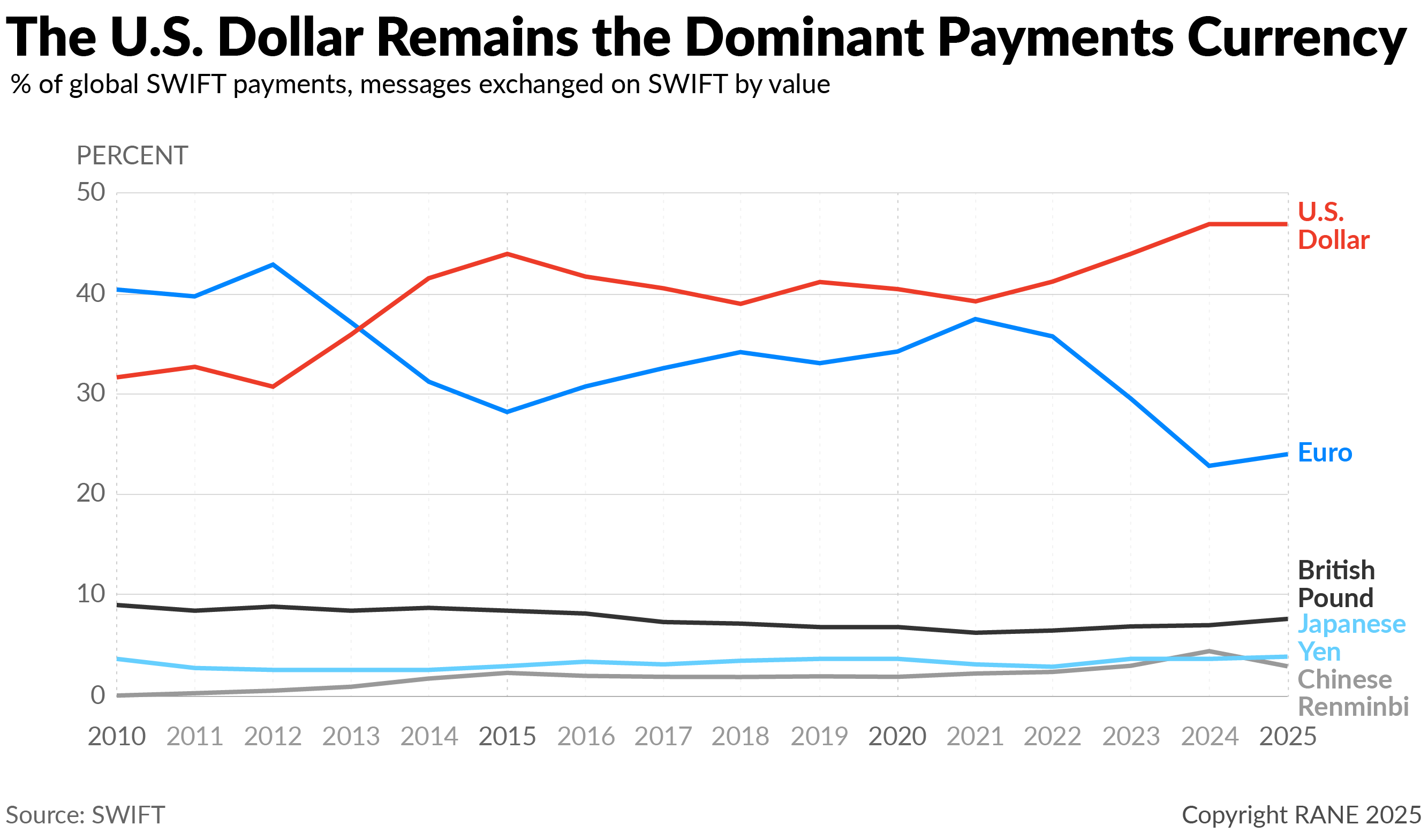

- The dollar accounts for 96% of trade invoicing in the Americas, 74% in the Asia-Pacific region and 79% in the rest of the world. In Europe, the main currency for trade is the euro, which accounts for 66% of all invoicing. International payments via SWIFT are a proxy for international payments. Including trade-related payments, the dollar share of SWIFT payments was 47% as of mid-2025, compared to an RMB share of less than 3%. Meanwhile, 90% of over-the-counter foreign exchange transactions involve the dollar on one side or the other, underscoring the dollar's continued centrality in global foreign exchange markets.

Government efforts to de-dollarize trade are largely a response to concerns about Western financial sanctions and the damage they would cause to a country's ability to engage in international trade. The United States and the European Union have imposed wide-ranging financial sanctions on Russia over the past decade, including the immobilization of the Bank of Russia's dollar- and euro-denominated central bank foreign exchange reserves, as well as restrictions on dollar and euro transactions. Relying on the dollar makes countries, particularly those with antagonistic relations with the United States, vulnerable to financial sanctions, which negatively affect trade flows. More recently, concerns about the stability of the dollar in the context of erratic U.S. economic policies and further increases in U.S. government debt have also incentivized central banks to increase gold purchases and diversify their foreign exchange reserves. Dollar weakness has been largely driven by Asian investors hedging their dollar exposure, including central banks, which hold the bulk of U.S. government debt.

China will continue to make the greatest strides in de-dollarizing its trade transactions, particularly with its Asian trading partners. In recent years, many countries (including India and the United Arab Emirates) have been exploring ways to increase the use of their own currencies in foreign trade. However, due to its significant economic size and importance as an international trader, China will have the most substantial impact on international currency diversification and the use of nontraditional international currencies to finance trade. U.S. and European exporters favor the dollar and euro due to better liquidity and funding access, making them less inclined to conduct trade with China using the RMB. Conversely, China's Asian (particularly Southeast Asian) trading partners are more amenable to using the RMB because of extensive trade ties and supply chain integration with China. For now, China lacks the ability and desire to replace the dollar as the dominant international currency due to wide-ranging restrictions on capital account transactions. Instead, by de-dollarizing trade, China is seeking to reduce its vulnerability to U.S. financial sanctions.

- China has been promoting the international use of the RMB, including in trade. It has established a cross-border interbank payment system, an RMB clearing and settlement system that reduces China's dependence on SWIFT, which has previously been targeted by U.S. sanctions. China also succeeded in including its currency in the IMF's Special Drawing Rights basket, in a bid to boost central bank demand for RMB assets. Additionally, China has made it easier for nonresidents to hold RMB assets and raise RMB financing. Beijing has established a number of international clearing banks to facilitate trade transactions as well, and the Chinese central bank has extended RMB swap lines with several counterparts under the same objective.

The RMB's greater use in cross-border trade will further fragment the international currency regime, marginally raising the costs of financing trade but not causing significant disruption. Although currency diversification away from the dollar may reduce the risk of trade disruption by reducing the effectiveness of dollar and euro sanctions, de-dollarization will also make trade financing more costly, given the lower level of liquidity and higher transaction costs associated with nontraditional international reserve currencies, such as the RMB. As a result, a more fragmented international currency and payments regime will structurally raise the cost of doing business for companies using nontraditional international currencies. It will not, however, significantly impact companies' ability to conduct trade or weigh on trade volumes, in contrast to tariff and nontariff policies and financial sanctions.

- Cross-border use of the RMB has increased significantly, particularly since the 2022 Russian invasion of Ukraine. For instance, in 2024, 52% of Chinese trade was settled in RMB, up from 40% in 2020. Additionally, the share of Chinese trade settled in dollars fell to 43% in 2024, from 54% in 2020. Meanwhile, the RMB accounted for close to 6% of the global trade finance market as of mid-2025, up from 2% in 2022, according to SWIFT, compared to a dollar share of 83% as of mid-2025.

China's growing use of the RMB in foreign trade will only marginally impact the currency's global role, as structural financial constraints and relatively closed capital markets will prevent it from challenging the dollar's dominance. Even if China's foreign trade is increasingly "renminbi-ized," particularly in relation to countries that do not issue an international currency (e.g., those in South and parts of East Asia), this will at best have a limited effect on the RMB's use by third parties. Third parties will prefer to use the dollar given its greater availability, fungibility and lower transaction costs, unless they fear becoming the target of U.S. financial sanctions. Moreover, there is no possibility of the RMB becoming a major international financial currency as long as China refuses to open its domestic capital markets and develop its financial sector, actions that remain very unlikely since they would destabilize the country's already fragile domestic economy. This is the case despite an increase in nonresidents raising onshore RMB debt, which currently is at least in part driven by lower RMB interest rates compared with the dollar.

- The U.S. Federal Reserve produces an index of international currency usage, which measures the importance of the RMB in terms of central bank foreign exchange holdings, international debt and loan issuance, over-the-counter foreign exchange trading, international payments and trade invoicing. According to this index, the RMB continues to rank far below the Japanese yen and the British pound.

- The broad-based access to the U.S. financial system enjoyed by nonresidents supports the issuance of international loans and bonds denominated in dollars. While China continues to impose significant restrictions on capital account transactions, Beijing has made it easier for nonresidents — especially foreign central banks — to hold and transact in onshore Chinese government bonds for reserve accumulation purposes. But as an international financial currency, the RMB remains relatively insignificant as far as international loan and debt security issuance is concerned, despite increasing issuance of onshore RMB debt by nonresidents.

The partial de-dollarization of international trade will not jeopardize the dollar's preeminence or drastically increase China's geopolitical leverage. In the coming years, the RMB will become more prominent in international trade, but mainly between China and smaller trading partners. U.S. and European companies are unlikely to use it at scale, and China's relatively closed capital account will continue to limit the RMB's appeal as an international financial currency. Meanwhile, the dollar benefits from incumbency such that only major U.S. policy failures — such as a debt default, capital controls or punitive taxation of foreign debtholders — could seriously threaten its dominance. Other alternatives remain constrained due to various factors. For instance, the euro suffers from weak fiscal integration; the British pound, Canadian dollar and Swiss franc lack sufficient government debt markets; and Japan's debt burden is even higher than that of the United States. As a result, most countries will still rely on the dollar unless sanctioned by the United States, and countries that do adopt more RMB settlement will do so to diversify risk, not to substitute dependence on the United States with dependence on China. The continued dominance of the dollar means the RMB will remain a limited borrowing and financial currency, despite the greater use of the RMB in lending by the Asian Infrastructure Investment Bank, the BRICS-backed New Development Bank and China's Belt and Road Initiative. Additionally, the RMB will not replace the dollar as the main unit of account for commodities, and its role as a store of value will remain modest given countries' continued reliance on dollar-denominated financial flows. Overall, the RMB will gain most as a means of exchange in small economies, slightly reducing China's exposure to U.S. sanctions but not significantly increasing Beijing's leverage over its trade partners.

- The U.S. government bond market stands at about $25 trillion compared with China's $20 trillion and Japan's $10 trillion. Debt issued by the major European government issuers (the United Kingdom, France and Germany) amounts to less than $5 trillion. Moreover, euro-denominated government debt markets are highly fragmented and characterized by varying degrees of credit risk.