The dollar's weakness against the euro will likely persist amid ongoing trade and fiscal policy uncertainty in the United States, negatively impacting European exports but also reducing the risk of potentially destabilizing U.S. financial policies. Despite expectations that protectionist U.S. trade policies would lead to an appreciation of the dollar, the U.S. currency has depreciated since Donald Trump returned to the White House in January. Meanwhile, U.S. equity markets have reached or remain close to all-time highs, despite the continued risk of trade-related economic disruption from Trump's sweeping tariff strategy. But while the value of the U.S. currency has fallen, domestic and foreign investor interest in dollar-denominated equities appears to be robust, which is somewhat unusual. Dollar depreciation has also been orderly, suggesting it is driven by a gradual shift by private investors into non-dollar-denominated, including euro-denominated assets.

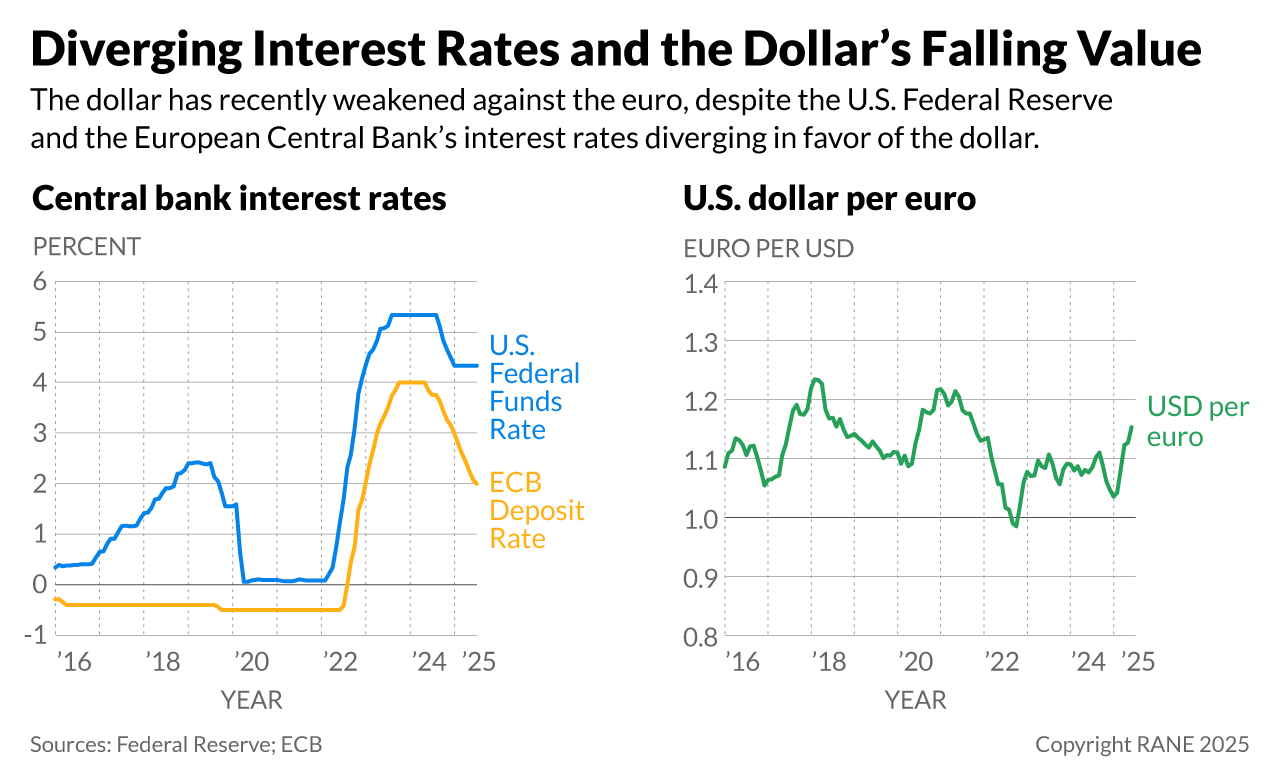

- Since Trump took office in January, the dollar has depreciated 11% against the euro. The U.S. currency has also experienced a slightly smaller depreciation in trade-weighted terms, meaning against a broader basket of currencies.

- The dollar-euro interest rate differential has widened year-to-date. The U.S. Federal Reserve has left its policy rate unchanged at 4.25-4.5%, while the European Central Bank has lowered its policy rate by a cumulative 100 basis points to 2%. A widening rate differential in favor of the dollar should have, all other things being equal, led to dollar appreciation.

A weaker dollar and relatively high U.S. interest rates indicate that investors are concerned about erratic U.S. economic policies, including Trump's attacks on the Federal Reserve, as well as large fiscal deficits and increasing government debt. While a combination of high U.S. interest rates and sizable fiscal deficits has historically led to a strong dollar, the significant uncertainty surrounding U.S. trade and foreign economic policies is driving investors to increase their holdings of non-dollar assets. This uncertainty stems from multiple factors, beginning with the April 2 announcement of Trump's sweeping reciprocal tariffs on U.S. trading partners, which prompted a sell-off of both the dollar and U.S. treasuries. There is also increased concern about the Federal Reserve's independence amid Trump's criticisms of Fed Chair Jerome Powell over high interest rates. Additionally, U.S. government debt dynamics are expected to further deteriorate following the approval of the Republican Party's landmark budget reconciliation bill, which will help keep fiscal deficits high. At the same time, however, U.S. equity markets remain strong, which suggests investor optimism in the context of the ongoing AI boom, the Trump administration's deregulation agenda and the relatively favorable, if narrower, U.S.-euro area growth differential.

- In May, U.S. headline and core personal consumption expenditure inflation, the Federal Reserve's preferred inflation gauge, remained above the Fed's 2% target, reaching 2.3% and 2.7% year-on-year, respectively.

- The Federal Reserve's Summary of Economic Forecasts, published on June 18, projected 50 basis points worth of interest rate cuts this year. Similarly, markets assign the highest probability to 50 basis points worth of cumulative rate cuts by the end of the year.

- Trump has repeatedly criticized Federal Reserve Chair Jerome Powell for keeping interest rates too high, and media outlets frequently publish stories about Trump's alleged plans to sack him. In response to these rumored plans to fire Powell, Trump on July 17 said, ''I don't rule out anything, but I think it's highly unlikely.'' It is unclear whether the U.S. president has the legal power to dismiss a Fed chair.

- U.S. unemployment was 4.1% in June, suggesting a fairly tight job market that is not conducive to rapid disinflation.

- The Congressional Budget Office estimates that the sweeping tax cuts in Republicans' newly passed budget reconciliation bill will add $3-4 trillion worth of government debt by 2035 (roughly 10% of projected U.S. GDP in 2035), compared to a scenario where the cuts would have expired. Continued large fiscal deficits will increase the United States' debt-to-GDP ratio, which currently stands at 100% of GDP.

If the dollar remains weak, it will help limit the incentives for the Trump administration to pursue unorthodox, risky and potentially destabilizing financial policies aimed at further weakening the dollar. Uncertainty about U.S. economic policy, including trade policy, will continue to weigh on the dollar. An escalation of the president's attacks on the Fed would further weaken the currency. Meanwhile, the interest rate differential is unlikely to notably shift in the dollar's favor in the coming months, as the European Central Bank will likely lower interest rates by 25-50 basis points this year, while the Federal Reserve will likely only lower rates by 0-0.75 basis points. It is unlikely that recent dollar weakness or high U.S. tariffs will substantially narrow the U.S. trade deficit. But even if some narrowing occurred, it would not prompt the Trump administration to pursue less protectionist policies. However, a weaker dollar will reduce the likelihood of other, risky ''unorthodox'' financial policies aimed at weakening the U.S. currency in the context of continued large U.S. trade deficits. Such policies, which have been floated by various Trump administration officials, include taxes on capital inflows or foreign holdings of U.S. assets, or a restructuring of foreign-held U.S. debt. Anecdotal evidence suggests that Trump suspended his sweeping tariffs in April in response to unusual instability in the U.S. Treasury market, and the Treasury Department will oppose any market-destabilizing financial policies aimed at further dollar weakening. This means even Trump may hesitate to pursue these unorthodox policies, which would raise the risk of significant dollar and U.S. Treasury market volatility by seriously undermining foreign investor confidence.

- On the campaign trail, Trump proposed imposing a tax on foreign capital inflows. Members of his administration have also floated the idea of asking allies to restructure their holdings of U.S. government debt to reduce U.S. interest payments. Congress almost approved a so-called ''revenge tax'' in the context of the recent budget reconciliation bill that would have allowed U.S. authorities to impose additional, targeted taxes on foreign holdings of U.S. assets. In addition to further weakening the dollar, such highly destabilizing policies would risk undermining the dollar's appeal as the dominant reserve currency.

- A weaker dollar will somewhat help alleviate financial pressure in countries with large net dollar debts, even though high U.S. interest rates limit the degree to which indebted emerging and developing countries will benefit. Meanwhile, higher U.S. tariffs make it more difficult for these countries to earn foreign currency revenues.

For Europe, higher U.S. tariffs combined with a stronger euro will lower inflation but negatively impact economic growth. Increased government spending in Europe, particularly by Germany following the reform of its debt brake, will help support domestic demand. However, a stronger euro and higher U.S. tariffs will weigh on Europe's exports, which will, in turn, dampen the growth outlook of euro area economies that export a lot of goods to the United States, such as Germany. Nonetheless, the outlook for increased investment and defense spending will continue to attract investment into the euro area, further helped by erratic, dollar-negative U.S. economic policies. More predictable euro area policies will continue to support the greater diversification of international investors' portfolios into euro-denominated assets. A stronger euro has helped and will continue to help lower inflation and lead to lower interest rates, which will help ease financing conditions as well.

- Euro area inflation declined to the ECB's 2% target in June. Markets and analysts expect the ECB to lower interest rates by another 25 basis points this year, bringing the policy rate to 1.75%. The ECB lowered its policy rate from 3% at the beginning of the year to 2%.

- In its April World Economic Outlook, the International Monetary Fund projected U.S. GDP to grow by 1.8% in 2025 and 1.7% in 2026, a notable reduction from the IMF's previous estimates of 2.7% and 2.1% growth for those years. In contrast, the IMF's revisions for the euro area's GDP growth were more modest, with forecasts of 0.8% in 2025 and 1.2% in 2026, representing only a 0.2% downward adjustment.

- France and Italy — the euro area's second- and third-largest economies, respectively — have limited room to increase fiscal spending. But Germany, the largest eurozone economy, has committed to spending an estimated additional 1 trillion euros on infrastructure and defense over the next few years, which is a sizable amount given the euro area's GDP of EUR 15 trillion. This has helped make previously undervalued European equities more attractive to investors, in addition to the narrowing U.S.-euro area growth potential and uncertainty of U.S. economic policies.