Editor's Note: With many significant elections occurring in 2024, RANE is publishing a series of scenario analyses focused on different outcomes of major elections occurring this year, describing how an election outcome might unfold with implications for each potential outcome. The first installment covered India's general election, the second covered European parliamentary elections, the third covered South Africa's general election, the fourth covered Mexico's presidential election, the fifth covered Iran's presidential election, the sixth covered the United Kingdom's general election and the seventh covered Sri Lanka's presidential election. The following is a scenario analysis for Nov. 5 U.S. presidential and congressional elections.

The Nov. 5 U.S. presidential and congressional elections are a virtual tossup, with Democratic candidate and Vice President Kamala Harris polling slightly ahead of Republican candidate and former President Donald Trump nationally, but locked in a virtual dead heat with Trump in the Electoral College race that will decide the race. While the outcome of the presidential election will, of course, significantly impact future U.S. domestic and foreign policy, House and Senate elections will be an important factor regarding whether the next president will need to rely largely on executive power to implement policy, which can be constrained by the courts, or will have enough allies in Congress to push through more substantial policy through legislation. The outcome of the congressional election is more likely to shape the next president's domestic agenda, as typically the president has more freedom on foreign policy and courts tend to defer to the president on national security matters.

A Harris administration would largely result in continuity on most domestic and foreign policies as she has largely campaigned on a platform that builds upon the Biden administration's policies. On foreign policy, Harris would strongly support Ukraine in its war against Russia and would push Congress to authorize more financial and military aid for Kyiv, though the strength of the Republican Party — and Trump's personal political strength — after the election will shape the size of U.S. military aid packages. Harris would also expand technology-related restrictions on China targeting cutting-edge technologies going beyond semiconductors, quantum technologies and artificial intelligence, such as biotechnologies. Harris would also maintain U.S. support for domestic and international climate initiatives, though Congressional opposition would limit Washington's ability to help contribute to international climate finance through direct U.S. government assistance programs.

On the other hand, a second Trump administration would lead to significant changes in U.S. foreign and domestic policies. While certain policies, like national security-related technology restrictions on China would also be implemented in a Trump administration, Trump's priority focus on international trade matters would be on tariff policy, not technology policy. The United States would implement new tariffs on major U.S. trading partners, such as China, Vietnam and potentially even EU member states, triggering retaliation and undermining U.S. manufacturing growth dependent on imported intermediate goods. Trump would also support extending tax cuts implemented in 2017 that expire in 2025; and while these cuts would positively affect economic growth in the short term, they risk adding trillions of dollars to the U.S. debt long-term that increase the risk of budgetary control measures, including military sequestration, after he leaves office. Trump would also reduce U.S. support for Ukraine in an effort to quickly end the country's war with Russia, but this is unlikely to result in a cease-fire until the second half of his term at the earliest. Trump would also seek to reverse all of the Biden administration's climate policies and bring the United States back out of the Paris Agreement climate change treaty.

Finally, this U.S. election cycle also brings in a higher risk than normal for the United States of a disputed outcome and politically motivated violence. The worst case scenario would be for Harris to win a close election that Trump rejects and leads to his supporters violently responding by targeting U.S. government election officials and buildings in the lead-up to Harris' inauguration — a security threat that will require the new president to devote extensive political capital to deal with. But even a Trump victory would bring similar risks as legal challenges against his eligibility and efforts to squash legal cases against him could result in a constitutional crisis and balance of power concerns that require Trump to focus heavily on domestic political issues to start his new term.

Trump Wins the U.S. Presidential Election

In a second term, Trump's foreign and domestic policies would be shaped by a return to his "America First" approach to foreign policy and a mix of deregulation and protectionist economic policies. Regardless of whether Trump's return to the White House coincides with his Republican Party winning control of Congress, Trump heavily relies on executive action to implement foreign and trade policy — two areas where the president enjoys significant power with limited congressional oversight. Trump places significant tariffs on imports from China and moderate levels of tariffs on the European Union and select other countries. If the Republican Party controls Congress, then many of Trump's 2017 tax cuts will be extended in some fashion ahead of their end of 2025 expiration date, worsening the long-term U.S. debt outlook as significant budget cuts to offset the tax cuts extension are unlikely. If the Republican Party does not control Congress, then most of the taxes are likely to expire, though the negotiation process will be extremely chaotic, with Trump likely using aggressive tactics, including threatening a government shutdown, to attempt to get them extended. On foreign policy, Trump quickly reduces military support and foreign aid to Ukraine in an effort to start peace talks between Russia and Ukraine, though Kyiv will likely initially resist Trump's efforts and attempt to work more closely with other NATO countries to avoid large concessions to Russia. Trump's China policy is aggressive; while his personal focus is on placing new trade restrictions on China, his administration will also move forward with national security-related technology restrictions similar to the Biden administration. Finally, Trump attempts to reverse most of the Biden administration's climate initiatives, including reducing funding authorized by the Inflation Reduction Act, withdrawing the United States from the Paris Agreement and rolling back emissions and other environmental rules aimed at accelerating the decarbonization of the U.S. transport and power sectors.

Implications

Fiscal and Macroeconomic Environment

- If the Republicans win control of Congress, the United States is likely to extend most tax cuts included in the Tax Cuts and Jobs Act of 2017 that expire at the end of 2025, possibly through budget reconciliation. In the short term, the extensions largely benefit wealthier U.S. households with larger tax breaks, but do boost savings for investment. In the long-term, if reconciliation is used, they will likely sunset in the mid-2030s, setting up another dispute over the extension in a decade.

- If the Republicans win control of Congress, they are highly unlikely to win a filibuster-proof majority in the Senate. As such, Trump and the Republicans fail to offset any tax cuts or extensions of existing tax cuts with spending reductions, leading the U.S. federal debt to significantly increase during the Trump administration, adding as much as $5 trillion to $6 trillion to the U.S. budget deficit.

- If the Republicans win control of Congress and keep taxes low, the relatively fast accumulation of debt increases the likelihood of another round of U.S. budget sequestration after Trump's term, which would likely result in military spending and other discretionary spending growth being capped or reduced. For the military, this would most likely result in delays to the procurement cycle and outright cancellations of some projects as the military focuses on maintaining spending on personnel and locations.

- If the Republicans fail to win control of Congress, in 2025 there are likely to be contentious budget fights between Trump, Republicans in Congress and Democrats in Congress over passing new spending bills and extending the 2017 tax cuts that could see repeated and/or lengthy government shutdowns, which not only cause a temporary slowdown in economic growth, but also delays to various government contracting processes.

- Trump rhetorically presses the U.S. Federal Reserve to reduce interest rates to boost growth, but ultimately he does not make any decisions that significantly weaken the Fed's independence due to Congressional blowback on both sides of the aisle and opposition within the business community.

Energy, Environment and Climate Change

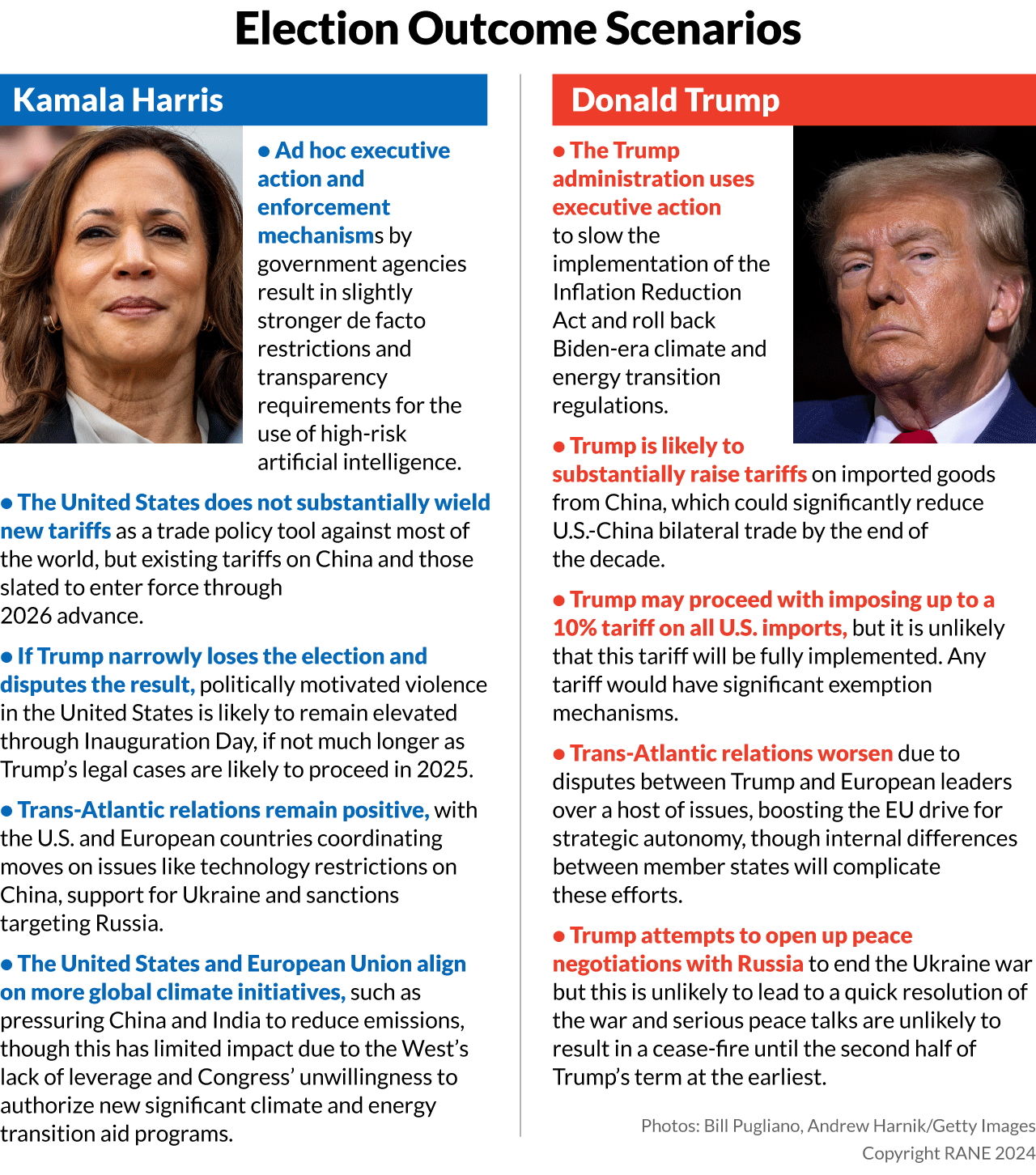

- Although the Inflation Reduction Act is unlikely to be overturned due to its funding benefiting Republican districts more than Democratic districts, the Trump administration is likely to use executive action to slow the implementation of the IRA, such as through changing requirements to the act's electric vehicle tax credit to make fewer vehicles qualify, for example by exiting critical raw materials agreements (or saying they do not qualify as free trade agreements) that then make fewer vehicles qualify for the tax credit.

- The Trump administration attempts to roll back virtually all of the Biden administration's rules and regulations related to climate change and the energy transition, including Securities and Exchange Commission disclosure requirements, tailpipe emissions regulations, and requirements on coal-fired power plants and new natural gas-fired power plants to reduce emissions dramatically by the mid-2030s, and the moratorium on new liquefied natural gas export capacity. Although regulations on companies will ultimately lessen, regulatory uncertainty is likely to remain high as each of these regulatory reversals is likely to be tied up in lengthy court battles.

- The United States is likely to withdraw from the Paris Agreement and reduce cooperation on global climate initiatives like climate finance. The lack of U.S. participation limits global pressure on large emitters China and India, reducing their climate ambition. The lack of U.S. participation in climate finance initiatives slows the pace of the energy transition in developing countries.

- The federal government expands support of the U.S. oil and gas industry through opening up more federal lands for drilling and expediting the permitting process for drilling and other activities in the Gulf of Mexico and on federal lands. While this supports the growth of the U.S. oil and gas industry, it does not reduce U.S. exposure to international oil price volatility due to the U.S. markets' interconnectivity with the rest of the world through imports and exports.

Immigration and Border Issues

- The United States is likely to implement an aggressive border policy, likely through passing new legislation or executive actions that increase personnel on the U.S. border and conduct more thorough inspections of cargo entering the country, though the significant delays this would cause mean that such measures are unlikely to apply consistently to all cargo. This will risk creating unpredictable disruptions to cross-border supply chains.

- The United States is likely to heavily restrict visa issuance and immigration from the developing world, including India, exacerbating the U.S. skilled workforce shortages in industries like the software and cybersecurity industries, as well as skilled manufacturing jobs for semiconductor manufacturing, the latter of which will undermine U.S. attempts to build its advanced chipmaking industry.

- The Trump administration will likely attempt to implement some degree of deportations of illegal migrants and potentially even attempt to remove some legal migrants. Whether Trump would be able to launch such a mass deportation project is unclear, but support for many of Trump's policies by a majority of Supreme Court justices decreases the likelihood that legislation or an executive order would be deemed unconstitutional. If implemented, such a policy would reduce available workers across a range of sectors, including agriculture, manufacturing, services and retail.

Technology, Trade and Industrial Policy

- The United States does not pass any new large subsidy programs for the high technology or clean technology sectors similar to the CHIPS and Science Act or Inflation Reduction Act, and instead relies on tax cuts and tax holidays, often approved and negotiated at the state and local levels, to attract investment in those industries. While this reduces subsidies available for these industries, the Trump administration will approve critical projects and subsidies already authorized under the CHIPS and Science Act for semiconductors as well as some in the IRA specifically geared toward manufacturing investment due to Trump's support of unions and the manufacturing industry.

- The United States is unlikely to pass expansive regulations on the artificial intelligence sector and the Trump administration is likely to reverse the Biden administration's executive order on artificial intelligence, but the practical impact is likely to be limited due to the order's already limited scope. Limited federal regulations on AI keep the United States as the global leader in both AI development and deployment, though concerns about AI lead more states like California to pass some AI-related legislation.

- Negotiations surrounding USMCA's July 2026 review clause are likely to be contentious and will lead to short-term investor uncertainty as Trump may trigger a U.S. exit from the United States-Mexico-Canada Agreement as a negotiating ploy against Canada and Mexico. Ultimately, the USMCA is likely to hold together with few changes. The most significant alterations will likely affect the pact's rules of origin requirements for the auto sector, which are likely to be tightened to make it more difficult for vehicles to qualify for USMCA benefits.

- Trump is likely to substantially increase tariffs on imported goods from China, perhaps by as much as 60%. Over the medium term, this will lead to bilateral U.S.-China trade to decline relatively quickly, with total trade potentially falling to just 1% of U.S. total trade by the end of the decade if Trump moves forward with higher tariffs. While negotiations could emerge on a trade deal, such talks likely fail to reduce tariffs significantly and are likely to concentrate on capping new tariffs' size or the scope of goods covered.

- Trump may move forward with placing up to a 10% tariff on all U.S. imports, but it is unlikely that this tariff will be fully implemented. If the tariff survives court challenges, it is likely to have significant exclusions for many U.S. trading partners that reach a new trade agreement with the United States designed to boost U.S. exports to those countries if the United States has a trade surplus or narrow deficit with them. Nevertheless, countries with large trade surpluses with the United States, such as Germany and Vietnam, are more likely to see tariffs implemented on them.

- The United States places more restrictions on China's technology sector, including tighter restrictions on semiconductors, AI, quantum computing, and other critical and emerging technologies. Western coordination on these efforts declines, however, reducing the effectiveness of U.S. restrictions and enabling China to circumvent them more effectively.

- The United States is likely to implement new supply chain requirements barring or restricting the use of Chinese communications, sensors and other similar technologies in some critical infrastructure sectors, including U.S. vehicles and ports and logistics. Companies in affected sectors are forced to reduce or completely cut out their proportion of Chinese suppliers.

Foreign Policy

- Trans-Atlantic relations worsen due to disputes between Trump and European leaders over a host of issues, including trade disputes, NATO policy, the Russia-Ukraine War and support for democracy. Poor trans-Atlantic relations will boost the EU drive for strategic autonomy, though internal differences between member states will complicate these efforts. Poor U.S.-EU relations could lead Brussels to offer concessions on trade-related issues with China if the United States places large tariffs on European goods.

- The United States remains in NATO, but Trump is likely to rhetorically weaken the U.S. commitment to the defense pact, for example, by suggesting the United States might not recognize the pact's collective self-defense clause for countries that fail to reach 2% of GDP on defense spending. This will continue to boost Europe's defense spending, but will also lead European leaders to deepen defense ties bilaterally and through institutions other than NATO.

- The Trump administration cuts military aid for Ukraine and attempts to open up peace negotiations with Russia to end the war. This will reduce Ukraine's negotiating leverage against Russia, but is unlikely to lead to a quick resolution of the war and serious peace talks are unlikely to result in a cease-fire until the second half of Trump's term at the earliest.

- The Trump administration is likely to slow down the approval of new sanctions on Russia and may even offer limited sanctions relief in exchange for Russia entering peace talks. While some companies may have new opportunities in working with Russia due the suspension of sanctions on Russia, EU and U.K. sanctions on Russia's oil and gas industry will likely remain, keeping most sanctions architecture in place given how sanctions targeting Russia's gas industry largely work by targeting the shipping industry due to Europe's large role in the industry and the financial services sector supporting it.

- Relations between the United States and Iran remain tense, leading to sporadic periods of escalation in places like Iraq and Yemen. High tensions in the region lead to the risk of supply chain disruptions in shipping and attacks on U.S. forces in Iraq, though Iran and the United States are likely to try to avoid direct conflict with one another. A nuclear deal between Iran and the United States is unlikely.

- The United States maintains strong support for Israel against Hezbollah, Hamas and Iran, keeping tensions in the Levant high and likely sustaining the Israel-Hamas conflict through at least early 2025. This keeps the risk of occasional escalation between Israel and Iran and its proxies high, including possible direct airstrikes on each other. These intense flare-ups force companies to draft contingency plans for worst-case scenarios involving regional escalation, which could include disruptions to operations in Gulf countries due to attacks or perceived threats that cause foreign staff to be pulled out.

- The United States reintroduces sanctions on Venezuela in connection to its 2024 presidential election. This will reduce U.S. and European oil companies' ability to work in the country's oil and gas sector, especially as the Trump administration also will likely remove key sanctions waivers allowing some companies like Chevron to do so right now. This forces Venezuela to work more closely with Russian and Chinese oil companies to develop oil fields, though it initially hurts investment in the sector, causing production to decline.

Social and Other Issues

- Federal pressure increases on U.S. companies to reduce ESG-related initiatives, including on emissions disclosures, preparing for net-zero scenarios, corporate DEI programs and other issues as Republicans in power increase scrutiny on federal contractors using these programs and launch more lawsuits and/or congressional hearings on related issues. This widens the gap between the United States and the European Union on ESG regulations and enforcement, forcing companies with operations on both continents to adhere to divergent rules.

- Inequality in the United States worsens amid tax cut extensions for the wealthy and regressive tariff policies that undermine the U.S. manufacturing sector due to the high dependence on imported intermediate goods and cause price hikes on staples like imported appliances from Asia. Heightened inequality foments further political polarization in the United States that leads to more contentious elections in 2026 and 2028 as well as a heightened risk of politically motivated violence from the far left and far right.

- Trump will almost certainly squash the federal charges brought against him by special counsel Jack Smith, leading critics to warn about a decline in the U.S. separation of powers. This, coupled with the Supreme Court's ruling on presidential immunity, increases the likelihood of Trump broadly interpreting his powers to not only try to implement various policy measures and forcing the courts to try to block his powers on issues like tariffs and immigration policy, but also to carry out politically motivated investigations of various Democratic leaders, further hurting U.S. standing among pro-democracy groups.

Harris Wins the U.S. Presidential Election

As president, Kamala Harris would largely continue the Biden administration's foreign and domestic policy. Harris would seek to boost funding and financial support for the U.S. manufacturing base in critical and emerging technologies, including artificial intelligence, semiconductors and clean technologies, though the extent to which new funding is authorized will depend on whether the Democratic Party controls Congress. Her administration only sparingly introduces new tariffs to shield the economy, but largely keeps tariffs inherited on China, global steel and aluminum, and Southeast Asian solar panels and modules in place. If the Democratic Party controls Congress, most of the 2017 tax cuts for the wealthy will expire, though some modest tax cuts or credits for lower income classes will pass. If the Republican Party controls at least one chamber of Congress, negotiations over the tax cuts and other fiscal issues will be contentious and potentially lead to short government shutdowns. On foreign policy, the Harris administration maintains support for Ukraine through additional military aid, though the amount the United States can provide depends on congressional control. The Harris administration also aggressively places restrictions on China's technology sector and imports of Chinese technology goods for economic and national security reasons, though a new round of expansive tariffs on Chinese goods is less likely. Finally, soon after taking office, the Harris administration intensifies pressure on Israel to reach a cease-fire with Hamas to end the war in Gaza, potentially even resorting to calls for early elections in Israel, sanctions on minor officials and increased diplomatic pressure through bodies like the United Nations.

Implications

Fiscal and Macroeconomic Environment

- If the Democrats do not control Congress, the United States is likely to extend some of the 2017 tax cuts when they expire at the end of 2025 as a part of a negotiation process between Republicans and Democrats, though this process could lead to government shutdowns that cause short-term economic disruptions.

- If the Democrats control Congress, the United States is likely to extend a limited portion of the 2017 tax cuts, as well as some additional tax credits for children, though Harris and her allies will likely struggle to raise the corporate income tax to 28% without some Republican support. This causes the U.S. deficit to grow on the order of $2 trillion to $3 trillion, sparking more concerns about U.S. debt-servicing and borrowing costs.

- Rising U.S. debt levels will lead to a new push by Republican fiscal hawks to reduce spending. Initially, this will have limited impact if the Republicans do not control either house of Congress, but could become a roadblock to new spending measures in the second half of Harris' term if they gain control of one of the houses. This would likely play out over negotiations for another budget control bill to freeze or limit the growth of discretionary spending.

Energy, Environment and Climate Change

- U.S. climate ambitions grow throughout the Harris administration, such as through stronger requirements for power plants, stricter emissions requirements and other federal regulatory requirements. This leads to U.S. emissions dropping faster than if Trump were elected, though the impact on climate change overall is likely to be limited in the short to medium term due to the slow nature of the energy transition.

- The United States and European Union align on more global climate initiatives, such as pressuring China and India to reduce emissions, but the United States falls behind in direct climate finance due to Congress blocking large authorizations, unless the Democrats gain control of the Senate with a 60-seat filibuster-proof majority.

- Although environmental requirements and enforcement on the oil and gas industry tighten, such as those covering methane emissions, the United States does not ban fracking and the United States remains a lucrative location for oil and gas investment, keeping its direct dependence on oil imports relatively low. Nevertheless, the United States remains exposed to international oil and gas prices due to the imports and exports of crude oil and petroleum products.

- U.S. government programs to implement the Inflation Reduction Act remain in place and the United States is able to successfully close more agreements to broaden the qualification mechanisms for the IRA's EV tax credit through signing new critical raw materials trade agreements with more countries and jurisdictions, like the European Union.

Immigration and Border Issues

- The United States is unlikely to significantly shift current border security policies, though the Harris administration will push for passing legislation increasing security at the border in order to reduce the risk of personnel becoming overwhelmed during periods of high migrant border crossings. This would reduce risks of unpredictable disruptions to cross-border supply chains.

- The United States is likely to weaken some visa restrictions on high skilled workers in the technology and technology manufacturing sectors in order to keep U.S. high technology competitive. This includes weaker restrictions on visa approvals from South Asia. However, this does not extend to asylum seekers and migrants from the Americas due to the U.S.-Mexico border crisis still being a concern for Democrats and Republicans alike.

Technology, Trade and Industrial Policy

- The United States is likely to pass new industrial subsidy programs targeting clean technology and critical and emerging technologies' manufacturing and adoption. Due to the fact that existing authorizations have not run out of funds, the new programs are unlikely to be as large as the Inflation Reduction and CHIPS and Science acts. Nevertheless, the larger programs help the United States attract more manufacturing investment over the medium term.

- Although the United States is unlikely to implement broad AI regulations through legislation, there are likely to be ad hoc executive action and/or enforcement mechanisms by government agencies resulting in slightly stronger de facto restrictions and transparency requirements for the use of high-risk AI tools, similar to such de facto policymaking done by the Biden administration's Federal Trade Commission. Nevertheless, these restrictions' reliance on such mechanisms keeps their scope narrow compared to the EU AI Act, positioning the United States to continue to lead the race to develop and deploy AI.

- Negotiations surrounding the USMCA's July 2026 review clause are not contentious and do not significantly increase business uncertainty. Any changes to the pact are primarily focused on tightening requirements for the auto sector's rules of origin, but the United States does not threaten to exit the trade pact as a negotiating ploy.

- The United States does not substantially wield tariffs as a trade policy tool against most of the world, however, tariffs on China remain in place as planned. This forces supply chains to continue to adapt to the Biden administration's May 2024 tariffs that come into effect between 2024 and 2026 on certain strategic goods, including permanent magnets and semiconductors.

- The United States is likely to implement new supply chain requirements barring or restricting the use of Chinese communications, sensors and other similar technologies in some critical infrastructure sectors, including U.S. vehicles and ports and logistics. Companies in affected sectors are forced to reduce or completely cut out their proportion of Chinese suppliers.

- The United States is likely to expand outbound investment screening processes, including giving the U.S. government the ability to block certain investments outside just the AI, quantum technologies and semiconductor sectors, likely including other critical and emerging technology sectors, such as biotechnology and AI. This will contribute to the fracturing of technology supply chains for affected technologies, gaps that will only widen as time goes on.

Foreign Policy

- Trans-Atlantic relations remain positive, with the United States and European countries coordinating moves on issues like technology restrictions on China, support for Ukraine and sanctions targeting Russia. This strong relationship allows most European governments to take stronger positions in their own relationships with Russia and China, such as by leading the European Union to offer fewer concessions on its trade dispute over EVs and other green technologies with China.

- Over time, the United States becomes more willing to negotiate with Iran over its nuclear program. Negotiations resulting in a broad new Joint Comprehensive Plan of Action-like deal are unlikely during a first Harris administration due to the limited time elapsed since the Israeli-Hamas War and Harris' 2028 reelection campaign. Still, a more limited deal that involves Iran freezing certain aspects of its nuclear program is possible in the second half of Harris' first term, if unlikely. Such a deal would reduce regional tensions between the U.S. and Iran.

- If the Republicans perform extremely poorly in the 2024 election, support in Congress for Ukraine is likely to increase, allowing the United States to pass new large military aid and other support packages for Ukraine. This gives Ukraine a better ability to withstand Russian military aggression, though is ultimately unlikely to be enough support for Ukraine to retake significant territory lost to Russia.

- If the Republicans retain control of the House, support for Ukraine is likely to remain constrained by House opposition to large new funding packages, though occasional packages are likely to be pushed through. Still, the close coordination between the United States and NATO allies to support Ukraine gives Ukraine significant backing to limit Russia from seizing large swaths of Ukrainian territory in new offensives.

- The United States is likely to have relatively relaxed limits on Ukraine's use of U.S.-made weapons in Russian territory, leading to a relatively high frequency of Ukrainian attacks on Russian energy and other infrastructure that disrupts Russian energy supplies, both internally and externally. Russia will warn that U.S. and NATO support for Ukraine risks a Russia-NATO conflict, but such conflict remains unlikely due to Russia largely still benefiting from the Ukraine War largely having frozen along its current lines.

- The United States is likely to place some limited sanctions on Venezuela in response to the country's disputed 2024 election, which cut off Venezuela's oil exports to Western buyers. The United States, however, is unlikely to fully impose sanctions on Venezuela over concerns that sanctions would contribute to more emigration to the United States and hurt Venezuela's lower class the most.

- The Harris administration will ramp up pressure on the Israeli government to reach a cease-fire with Hamas and other Iranian proxies in 2025, but even if one is reached, occasional attacks on shipping and Israeli interests by Iran and its proxies are likely in the absence of a nuclear deal between Iran and the United States. While the pace of attacks by the Houthis on maritime shipping persists, it drops to the point where most shipping is likely to resume through the Red Sea by early 2027.

Social and Other Issues

- If Harris wins the election by a narrow margin and Trump disputes the result, politically motivated violence in the United States is likely to remain elevated through Inauguration Day, if not much longer, as Trump's legal cases are likely to proceed in 2025 and his supporters will view the election as stolen. Heightened violence is likely to focus on elected officials and government buildings rather than companies, but vandalism and attacks targeting companies and corporate executives viewed as supporting Harris or opposing Trump cannot be ruled out.

- A Harris election victory, especially one in which Trump (and potentially other Republicans) do worse than polls expect, will lead to intensified debate in the Republican Party over its ideological and leadership direction as Trump, aged 78, is likely to recede as the dominant figure in the party over time as he continues to age. This process may not be fully complete by 2028, but would be accelerated if Republicans and Trump-backed figures suffer setbacks in midterm elections in 2026. An internally incoherent Republican Party would make it easier for Democrats to pass their favored legislation, as even moderate Republicans could support it.

- Four more years of Democratic control of the U.S. presidency will lead to more conservative-state pushback against policies seen as the federal government overstepping its bounds, particularly on social and economic issues like environmental policy, climate change legislation and reproductive rights. This leads to significant conservative-state legislation aiming to restrict federal government policies as well as lawsuits filed by both states and the federal government on the matter, leading to a high degree of policy uncertainty and regulatory unevenness in the United States for companies in affected areas.

- If Democrats perform well in the election, momentum behind ESG initiatives in the United States is likely to resurge by the end of Harris' first term in office, though not to the same degree as between 2021-22, as Supreme Court rulings on DEI-related issues and likely rulings against companies will limit the scope of corporate DEI programs. Support for equal pay, fair pay and emissions-reduction programs, however, likely rises.

- Regardless of the margin of a Harris election victory, Trump is likely to reject the outcome, but a close vote makes it more likely that his supporters act on his rejection and carry out large-scale demonstrations and/or violent actions targeting government officials, election workers and politicians. This violence will be at its highest during the lead-up to, and at the start of, Harris' term, but will likely slow down significantly as law enforcement arrests perpetrators and more Republicans publicly reject any acts of violence, similar to the decline in violence seen at Jan. 6, 2021.