Editor's Note: This two-part series explores the implications for global trade of a potential second Trump term. Part 1 focused on Trump's trade priorities, while part 2 focuses on what countries Trump could target, and how they would respond.

In a second term, Trump is likely to ramp up tariffs on China further, with a low prospect for a new trade deal between Beijing and Washington that removes or suspends any new tariffs, accelerating global changes in supply chains. Trump's threat to place 60% tariffs on China and broad focus on trade competition with Beijing suggest that he will pursue new tariffs on China, even if the final percent increase does not reach 60% or cover all imports from China. Compared to broader tariffs, new tariffs on Chinese goods would face less opposition on Capitol Hill, where there is much more support on both sides of the aisle for tough-on-China policies, though they would still negatively affect the U.S. macroeconomic environment and have a regressive effect on U.S. households. Trump can also clearly use a Sec. 301 investigation under the Trade Act of 1974 — the same mechanism he used in his first term to place tariffs on China — to put virtually any level of tariffs on any country the United States claims has harmed U.S. commerce. (The original investigation was based on alleged Chinese intellectual property theft.) While Trump may pursue another trade deal with China designed to get China to import more U.S. goods — and Beijing would be willing to entertain a trade deal that forestalls even a small amount of tariffs — any new trade deal is unlikely to result in a significant decline in existing tariffs because Trump would oppose lifting most tariffs, as he did in his first term. China failed to hit its purchasing commitments under the 2020 Phase One Trade Deal, reaching only around 60% of its import targets in 2020 and 2021 under the agreement — giving Trump little reason to expect China to meet any new import targets in a second agreement. The Phase One Trade Deal also did not include significant declines in Trump's tariffs on China as a part of the agreement, suggesting that in a second trade deal, Trump would expect most new tariffs he applied to remain in place.

- China would almost certainly retaliate to any new U.S. tariffs by increasing tariffs on certain U.S. goods, most likely goods from Republican states such as agricultural products. Chinese companies would also shift purchases away from the United States to other countries (such as Latin America for agricultural products). The Chinese government would also be more willing to make concessions in trade disputes it has with other countries, such as its ongoing dispute over electric vehicles with the European Union, where China could agree to voluntary export restrictions (e.g., quotas) on EVs and EV components exported to Europe.

- If the United States places tariffs on China that are closer to the 60% level that Trump has proposed, U.S. imports from China would decline significantly. In February, Bloomberg Economics estimated if the U.S. implemented 60% tariffs on China, it would result in imports from China declining from 14% of total U.S. imports in 2023 to just 1% by 2030 and compared to just 10% in 2030 if tariffs remain where they are now. The same analysis also estimated that it would boost imports from Southeast Asia in textiles and light manufactured goods by 5.1%, and electronics from Mexico by 3.5%, which would likely lead to a larger U.S. bilateral trade deficit with Mexico and Vietnam.

Trump is unlikely to place substantial tariffs on Mexico as a whole permanently, but will likely push for tighter restrictions on the auto trade as a part of the upcoming USMCA review mechanism and may even threaten to place tariffs on Mexico as a negotiating tactic, at least temporarily weakening investor confidence in Mexico. Unlike during his 2016 presidential campaign, Trump has not made broad tariff threats against Mexico or frequently threatened to pull out of a free trade agreement with Mexico and Canada, instead focusing his rhetoric more narrowly on any Chinese vehicles produced in Mexico, on which he has threatened to place up to 200% tariffs. Nevertheless, a second Trump presidency will see the USMCA come up for review in 2026, and negotiations over its renewal are likely to be contentious and create a high degree of business uncertainty that chills manufacturing investment and nearshoring into Mexico, at least temporarily. Since USMCA was initially signed in 2018, the U.S.-Mexico bilateral trade in goods deficit has ballooned from $77.7 billion to $152.5 billion in 2023, as electronics and other middle-end manufacturing supply chains have shifted away from Asia to Mexico to avoid U.S. tariffs on China. Due to Trump's disdain for high trade deficits, this figure will likely lead to him to threaten to leave USMCA and place tariffs or otherwise make significant demands of Mexico (and Canada) to renegotiate or modify aspects of the deal. Trump is unlikely to exit the pact or permanently place tariffs on Mexico (though he may threaten to do both) due to the immediate negative impact doing so would have on the U.S. economy, but he is likely to focus on boosting protection for the U.S. auto manufacturing industry and other heavy industries through strengthening the so-called Rules of Origin requirements in the pact. Those rules outline the percentage of "content" in a final product that can come from non-USMCA countries (such as the percentage of car parts produced outside North America) and still qualify for free-trade access to the United States. Tightening these requirements was a major focus of the USMCA negotiations to replace NAFTA, but in practice, these rules were slightly weakened in 2023 when a USMCA dispute panel sided with Canada and Mexico against the United States on a specific calculation method for rules of origin in the automotive industry. The panel backed a weaker method allowing for more vehicles to qualify for NAFTA benefits. As a part of these talks, Trump may also resurrect his planned quotas and tariffs on automotive imports that limit the number of vehicles produced in Mexico (and Canada) that can enter the United States duty-free.

- Trump may also again threaten tariffs against Mexico as leverage in negotiations on immigration and border policy, as he did in 2019 when he threatened 5% tariffs on Mexico as a pressure tactic to get Mexico to boost its security presence on its southern border with Central America to stem the flow of migration. While Mexico is likely to yield to U.S. pressure, just as it did in 2019, due to the high likelihood of U.S. tariffs causing Mexico to enter a recession, such a threat would only further chill investment and business confidence in Mexico.

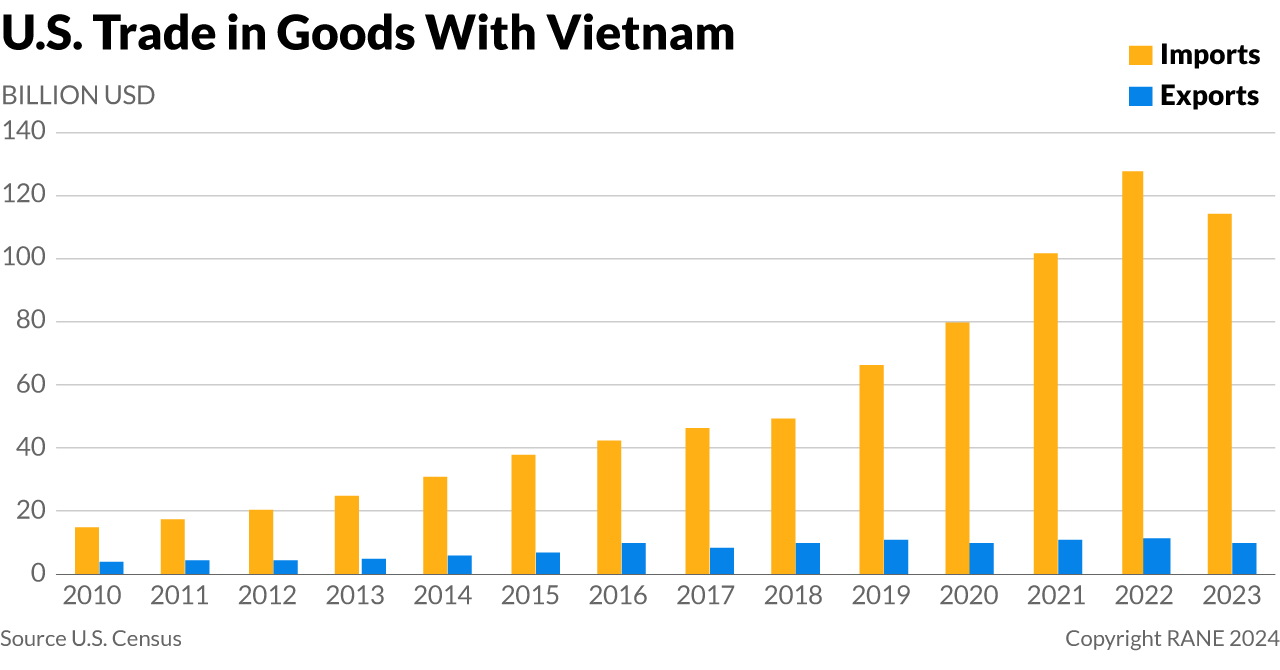

Vietnam's growing importance as a Chinese manufacturing hub and widening trade deficit with the United States are likely to lead a second Trump administration to place tariffs or other trade measures on Vietnam. Vietnam has been the clear beneficiary in Southeast Asia from high U.S. tariffs on China, as it has emerged as a major low-end manufacturing hub, especially as Chinese companies set up shop in the country to avoid U.S. tariffs. But this has resulted in Vietnam amassing the third-largest trade in goods surplus among U.S. trading partners, behind only China and Mexico, ballooning from just $39.5 billion in 2018 when the United States first applied new tariffs on China to a high of $116 billion four years later in 2022 and $104.5 billion in 2023. This makes Vietnam highly exposed to new tariffs or other protectionist moves under another Trump administration, especially given the perception that Chinese companies are using Vietnam to circumvent his tariffs. Even though Vietnam was not a focus country for Trump's tariff-heavy trade policy during his first term, at the very end of 2020 the Treasury Department labeled Vietnam a currency manipulator. The Commerce Department also changed its policy under Trump to consider currency manipulation as a form of export subsidies, allowing it to be investigated in antidumping/countervailing duty cases. Such concerns, coupled with the more recent development of Chinese companies using Vietnam to circumvent U.S. tariffs, are the two most likely issues that Trump is likely to focus on to open a new Sec. 301 investigation that would justify tariffs on Vietnam.

- Any tariffs on Vietnam would push more manufacturing to other Southeast Asian and South Asian countries, though they are less likely to see tariffs under another Trump administration since their trade surpluses with the United States are still relatively low and any increases in their trade surpluses with the United States would be unlikely to hit the threshold for action until after Trump exits the White House.

Trump's return to the White House would likely reopen trade hostilities with the European Union, including by potentially placing tariffs on European vehicles, which may ultimately push Europe to reduce trade hostilities with China. Under a second Trump presidency, trans-Atlantic relations will sour significantly, with rising trade tensions being just one of several points of contention between Trump and EU leaders. With Trump in office, tension is likely to reignite over two trade disputes, one over aluminum and steel tariffs and the other over digital service taxes. Ongoing U.S.-EU negotiations over a steel and aluminum agreement, which have led the United States to extend European access to U.S. tariff rate quotas for steel and aluminum and suspend some tariffs and the European Union to suspend retaliatory tariffs on 2.8 billion euros worth of U.S. imports, are likely to halt unless an agreement is reached prior to U.S. President Joe Biden's leaving office, given that Trump is strongly opposed to this detente. Moreover, under a second Trump presidency, several EU countries will likely proceed with digital services taxes suspended amid global tax negotiations on the assumption that Trump is unlikely to back the international tax reform agreed to in 2021 that would render those taxes irrelevant. The United States has threatened to place tariffs on several EU countries in response, which could provoke even further EU retaliation. Trump is also likely to resurrect his threatened tariffs on European vehicles and other industrial goods, as the U.S. bilateral trade deficit with many European countries has also widened in recent years. Europe will almost certainly retaliate with more tariffs on U.S. goods. While other countries subject to new U.S. tariffs are likely to engage in some talks with the United States, the EU economy is diversified enough that it can survive some of Trump's tariffs with only a limited economic impact. Moreover, European leaders would not want to offer concessions to Trump on trade, such as fresh voluntary export restrictions, at a time when trans-Atlantic relations over other issues — like NATO support for Ukraine — would likely also be worsening. Instead, greater tension between Brussels and Washington is more likely to push European leaders to enter negotiations with China over their brewing trade war over EU anti-subsidy tariffs on Chinese EVs. China may even be amenable to offering some concessions to Europe given that it would have an interest in amplifying a trans-Atlantic split under a Trump presidency and because it would also be dealing with higher U.S. tariffs on its exports.

- Trump's concern with European trade deficits has previously focused on Germany. The United States trade in goods deficit with Germany has risen from $56 billion in 2020, when Trump left office, to a record $82.5 billion in 2023, making it likely that it will draw Trump's attention should he return to the White House.