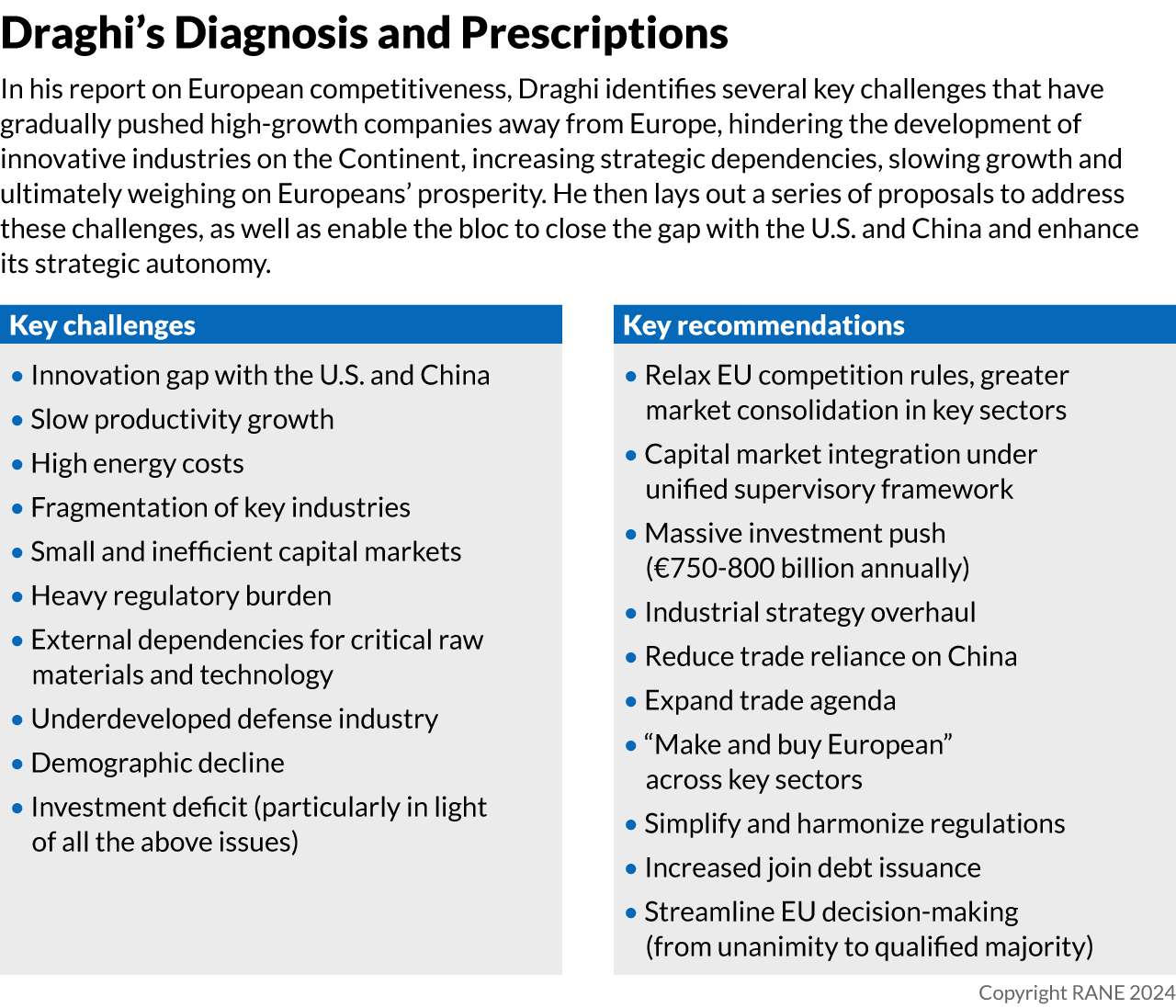

Mario Draghi's report on EU competitiveness will inform the new European Commission's agenda for the next five years, likely translating into proposals to create a more assertive and coordinated EU industrial policy, sweeping regulatory reforms, and measures aimed at spurring investment in advanced technologies, energy infrastructure, decarbonization and defense. However, political, financial and structural constraints will limit the extent to which Brussels will deliver on Draghi's ambitious targets. Former European Central Bank President and Italian Prime Minister Mario Draghi published his long-awaited report on the future of European competitiveness on Sept. 9. Requested by European Commission President Ursula von der Leyen in 2023, the report identifies several challenges to European competitiveness in areas such as defense, energy and advanced technologies that have gradually pushed high-growth companies away from Europe, hindering the development of innovative industries in the region, slowing growth and ultimately weighing on Europeans' prosperity. The report thus lays out a series of proposals to address the root causes behind the European Union's weakening competitiveness and for the bloc to enhance its strategic autonomy, such as relaxing competition rules, streamlining regulations and decision-making processes, adopting a more coordinated and assertive industrial policy, and pursuing a massive investment push supported by increased common spending. While von der Leyen is not obligated to act on Draghi's recommendations, the report will influence her commission's work program for the next five years.

- According to the report, Europe's socio-economic model has thrived on a combination of high domestic competition, open trade and a strong welfare state for decades. However, European growth has lagged behind that of the United States and China for the past twenty years, and the wealth gap between households in the European Union and the United States has widened since the 2009 global financial crisis. Moreover, as the external conditions that previously supported EU growth are fading — namely, reliance on cheap Russian energy, Chinese exports and U.S. defense guarantees — Europe will need to increase productivity to fuel growth, reduce the gap with its global competitors, and maintain its social model and high living standards, which will become increasingly urgent as its population inevitably declines over the coming decades.

- The report also underscores that Europe's defense industry is highly fragmented due to divergent national regulations and limited collaboration among EU member states, which leads to inefficiencies, prevents the formation of economies of scale and complicates efforts to integrate new technologies and form a cohesive defense strategy. According to the report, Europe also remains heavily dependent on external suppliers for key defense technologies and components, particularly from the United States, and it struggles with insufficient investment in research and development, which stifles technological innovation.

- The report argues that the main challenge to Europe's competitiveness is high energy prices, as the European Union relies heavily on imported fossil fuels and is incurring even higher costs as it shifts to renewable energy. This disadvantages energy-intensive industries such as chemicals and steel, as their operational costs in Europe are considerably higher than those of their competitors abroad. Furthermore, the rapid adoption of renewables is exposing weaknesses in Europe's grid infrastructure, which requires substantial investment to accommodate the intermittency of renewable sources like wind and solar. Finally, hard-to-abate sectors such as steel and cement will need massive capital infusions to meet the European Union's ambitious climate goals.

- Finally, the report claims that the fragmentation of Europe's telecom sector has led to inefficiencies and low profitability, hindering investment in advanced platforms that are critical for industries relying on digitalization. Europe is also losing ground in artificial intelligence and computing innovation, with fewer global tech leaders than the United States and China, making the region reliant on non-EU platforms and creating a strategic vulnerability, while the slow adoption of AI is affecting Europe's competitiveness across various industries. Europe's semiconductor industry is concentrated in a few niche areas, lacking capabilities in high-value segments like advanced processors for AI and graphics processing units, for which it remains heavily reliant on Asian suppliers.

The report urges EU member states to enhance joint arms development and procurement, consolidate the defense market and increase funding for common defense projects, but differences over financing and concerns about Brussels' role in defense procurement will likely limit progress in forming a unified European defense industry. To address the challenges affecting Europe's defense industry, the report urges member states to increase joint arms development and procurement (favoring European companies over global competitors), incentivize market consolidation, and increase funding for common defense projects and the development of dual-use technologies. Many of these proposals, including greater demand aggregation and joint procurement and development, already feature in the European Defence Industry Programme, or EDIP, proposed by the European Commission in March and will likely translate into concrete policy measures over the coming years, boosting industry integration on both the supply and demand side. Meanwhile, EU countries' spending on defense will increase, as will cross-border cooperation in defense research and development. However, significant differences remain among member states over the scale and type of financing, as well as what role Brussels will have in coordinating aspects of arms sales and procurement. Anything requiring additional EU financing or joint borrowing will likely meet the resistance of fiscally conservative member states, including Germany, which will limit the amount of resources the European Commission will be able to mobilize for the development of a pan-European defense industrial complex. Moreover, reluctance by member states to cede Brussels key aspects of defense procurement or — especially among smaller countries — to loosen anti-trust legislation for fear of national champions being eaten by foreign competitors will obstruct the formation of large European companies that can compete with U.S. giants on the global market.

- In his report, Draghi mentioned the need for a new ''Defence Industry Commissioner, with the appropriate structure and funding to define, coordinate and implement an EU defense industrial policy fit for today's new geopolitical context.'' The new European Commission that will convene in November or early December is expected to include such a new role in its College of Commissioners. The new commissioner will be tasked with overseeing the implementation of the EDIP. However, this new portfolio will likely be largely symbolic, at the least at the beginning, with limited powers and financial resources.

- Several member states are skeptical of the European Commission centralizing certain aspects of defense procurement. France, Germany and Italy have already pushed back against some aspects of the European Defence Industry Strategy published in March, demanding Brussels remain focused on the initial stages of development instead of expanding its influence into procurement, where they believe maintaining competition is crucial.

- Shortly after the publication of Draghi's report, German Finance Minister Christian Lindner promptly rejected the idea of issuing more Eurobonds, saying that ''Germany will not agree'' to increased joint borrowing.

- The European Commission has so far only earmarked 1.5 billion euros for the EDIP until 2027, against the 100 billion euros annually Draghi's report called for in additional spending on collaborative defense projects across EU member states, a considerable part of which he proposed would come from common financing. A recently approved review of the European Investment Bank's lending policies (which previously did not allow direct investment in weapons) will facilitate access to financing for European defense companies absent significant public financing at the EU level. However, this alone would still fall short of the ambitious targets that the EDIP and Draghi's report advanced.

- Draghi called for ''substantive incentive mechanisms'' to encourage governments to buy European products, which could be tied to EU funding through eligibility criteria similar to those already provided by the EDIP and the European Defence Fund. However, while eastern and northern countries that see Russia as a more imminent threat than their Western counterparts would certainly welcome increased joint financing to fund their rearmament, they would rather prioritize commercially made, readily available systems from whoever is ready to provide them faster and at better terms. This makes them more skeptical of the buy-European approach recommended by the report and endorsed by member states with sizable defense industries like France, Germany and Italy.

The report also calls for energy market reforms and major investments in green technology and decarbonization, but internal resistance will force national governments to bear most costs, with variable state support, rising trade barriers and structural constraints keeping Europe at a disadvantage compared with global competitors. The massive scale of investment Draghi's report said will be needed to boost the manufacturing of green technologies, accelerate the decarbonization of energy-intensive industries and develop large-scale cross-border grid infrastructure in the bloc, as well as the proposed creation of new common financing mechanisms to do so, will likely face opposition from fiscally conservative EU member states. Despite efforts to increase EU-level industrial policy coordination, the bulk of resources mobilized to finance these projects will thus continue to come from national governments, meaning that companies based in member states with greater fiscal capacity will remain the main beneficiaries of rising state support in these sectors. Meanwhile, over the coming years, state support will increase for industries where Europe enjoys comparative advantages and future growth potential, such as wind turbine or electric vehicle manufacturing, while trade barriers against subsidized Chinese imports will rise. This strategy will have mixed effects on Europe's energy transition and decarbonization efforts. While green tech manufacturers will benefit from increased financial support, the parallel rise in trade barriers against Chinese competitors could drive up costs for certain clean technologies in the short-to-medium term, slowing the deployment of renewable energy in Europe and raising costs downstream for project developers and consumers. Finally, efforts to simplify permitting procedures for renewable energy projects and instruments — such as joint natural gas purchases and long-term contracts to increase EU bargaining power and drive down prices, as well as purchasing agreements and contracts for difference to incentivize investments in decarbonization projects — will gradually reduce energy prices in Europe. Still, energy prices will remain higher than in the United States in the long term due to structural factors beyond the European Union's control, such as a lack of natural resources and subsequent dependence on imports.

- Many of Draghi's recommendations align with the Net-Zero Industry Act adopted by the European Union in June and will contribute to shaping the Clean Industrial Deal that will guide the new commission's industrial strategy.

- Draghi suggested that Europe ramp up support for industries such as EV and wind turbine manufacturing, for instance by introducing minimum quotas for local products and components in auctions and public procurement. He also emphasized the need to increase tariffs to level the playing field against subsidized competitors.

- This means that, besides tariffs, the European Union will seek to favor domestic green tech manufacturers over Chinese competitors through de facto local content requirements in auctions and public procurement procedures, either explicitly or in the form of environmental and security-of-supply considerations that would seek to favor Europe-based manufactures over their Chinese competitors.

- However, Draghi also acknowledged the need to adopt industrial policies tailored to the circumstances specific to each sector. This means sectors where Chinese dominance appears beyond repair, like solar panel manufacturing, will largely remain open to cheap Chinese imports. Here, diversification of suppliers, not trade barriers, will be the priority to reduce strategic dependencies.

- Draghi identified significant investment needs for Europe's decarbonization and energy transition efforts. Specifically, the four largest emission-intensive industries (chemicals, metals, cement and refining) will require 500 billion euros over the next 15 years to fully decarbonize, while investment in transport infrastructure will require approximately 100 billion euros annually between 2030 and 2050.

Finally, Draghi advocates for greater telecom consolidation to create European champions, but this will face challenges from EU competition rules and structural barriers, while Europe's fragmented market and limited capital access will hinder its ability to compete globally in sectors such as AI, advanced computing and semiconductors, even if investment grows and regulations are simplified. Draghi called for greater consolidation in the telecoms sector to allow for the creation of so-called European champions, or companies that can gain the scale necessary to compete globally and advance the massive infrastructure investment needed in Europe, while advocating for stronger action in keeping high-risk suppliers (like China's Huawei and ZTE) out of Europe's advanced networks. The new European Commission will likely incorporate calls for deregulation in the telecoms sector into its work program for the next five years, but consolidation will be more challenging to pursue as it would require significant reforms to the European Union's competition rules, which more market-oriented member states have long opposed and that could now face increased resistance in the European Council as nationalist parties gain growing influence in national governments. Meanwhile, simplifying regulation in areas like AI and privacy could help spur innovation and improve the commercialization of research in these areas. Yet, even with more relaxed competition and privacy laws, European companies will largely continue to lag behind global competitors because of structural constraints in the European Union that do not burden sovereign countries like the United States and China, such as a fragmented regulatory landscape across member states, language and cultural barriers that complicate the swift adoption of AI-systems across the bloc, and comparatively less access to capital. Finally, since Europe is unlikely to grow a truly globally competitive AI and advanced computing sector, this also means domestic demand for high-end semiconductor chips is unlikely to ever reach the point that it would justify massive investment in advanced semiconductor research, development and manufacturing that the Draghi called for in the report.

- Consolidation, coupled with deregulation, would help the bloc's largest telecommunications companies improve their profitability and stimulate investment into advanced networks needed for the European Union to accelerate its digital transition and increase productivity. However, smaller market players in the sector and consumer associations have criticized consolidation, arguing it would only empower large companies and enable the formation of oligopolies imposing higher prices.

- The report also suggests expanding the EU Chips Act to boost funding and coordination for advanced semiconductor research, development and manufacturing, in an effort to reduce the bloc's reliance on third countries. However, there are significant structural constraints toward boosting domestic production of advanced chips, such as skilled labor shortages, supply chain gaps, high energy prices and significant environmental costs in Europe. To overcome these constraints, Europe would at least need assurances for growing domestic demand, but this is unlikely to materialize without a competitive AI and advanced computing sector.

- Draghi called for the simplification of EU privacy, data and AI regulations, including through the harmonization of AI sandboxes, better implementation of the General Data Protection Regulation (GDPR), and the adoption of an ''EU cloud and AI Development Act'' to harmonize cloud architecture requirements in the bloc and accelerate the deployment of AI applications across industries. Draghi estimated that achieving full gigabit and 5G coverage across the European Union (and closing the digital divide between urban and rural areas in the bloc) would require a 200 billion euro infrastructure development.