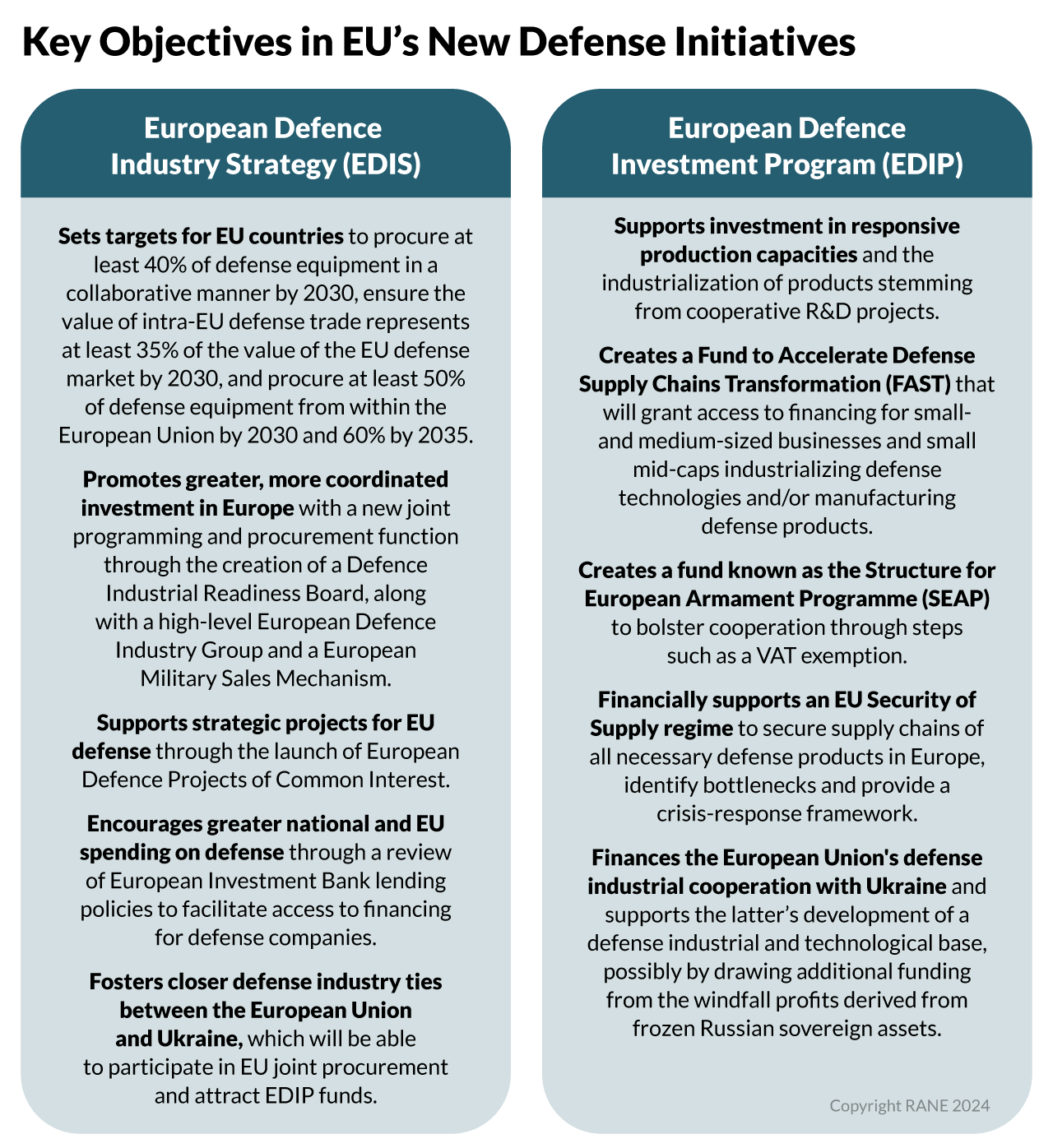

A new EU defense industrial strategy seeks to support member states' efforts to restock and acquire new defense equipment in the short term and boost the European Union's ability to enhance its defense capabilities and acquire more strategic autonomy on defense in the long term, but disagreements over joint funding and structural constraints to defense spending in Europe may reduce its efficacy. On March 5, the European Commission unveiled the European Defence Industry Strategy (EDIS) and the European Defence Investment Program (EDIP), both of which are meant to boost the bloc's defense capability development. Together, EDIS and EDIP aim to facilitate cross-border cooperation for arms production, purchase and ownership between EU member states, strengthen the bloc's defense technological and industrial base, and create an EU market for defense. The EDIS sets out to clarify how the European Union intends to support the European Defence Technological and Industrial Base (EDTIB) to achieve readiness and increased competitiveness, outlining a comprehensive plan to help member states enhance their collective defense capabilities by using existing frameworks, promoting cooperation in defense procurement, supporting research and development and boosting security of supply. The EDIP, in turn, aims to provide the regulatory and financial tools to pursue the goals laid out in the EDIS, mobilizing 1.5 billion euros from the EU budget through 2027 and providing a new legal framework (the Structure for European Armament Programme, or SEAP) to facilitate and scale up member states' cooperation on defense equipment.

- The EDIS entails the creation of a European Military Sales Mechanism, which would be Europe's version of the U.S. Foreign Military Sales mechanism, under which Washington helps foreign countries buy from U.S. companies. Set to be ready by 2028, the mechanism would enhance the availability of EU defense equipment by helping member states stock and sell weapons, as well as establish a single catalog for future defense framework agreements and contracts with EU-based arms manufacturers. With time, this could create greater competition for U.S. companies, as well as Japanese and South Korean companies, selling in Europe.

With these initiatives, Brussels is simultaneously seeking to support Ukraine against Russia, bolster European security, achieve greater strategic autonomy on defense, and strengthen its industrial base. The European Union is undergoing the largest rearmament process since the early stages of the Cold War, but the war in Ukraine has highlighted the bloc's many defense production constraints. This has placed defense-industrial strategy at the forefront of Brussels' agenda, both in terms of aiding Ukraine in the short term and bolstering European security in the longer term. The European Commission's plans aim to align these goals with two of the bloc's other main strategic objectives — namely, achieving greater strategic autonomy and fostering a more competitive and resilient industrial base. As European countries increase defense spending in the wake of Russia's invasion of Ukraine, Brussels wants to redirect at least half of EU governments' defense spending on procurement to local companies by the end of this decade, all the while incentivizing long-term orders, coordinating investment in expanded production capabilities, and facilitating joint procurement to more efficiently plug key capabilities gaps. The strategy also underscores a transition from the European Union's traditional free-market approach to more interventionist industrial policies on defense in response to structural challenges, such as rising global technology competition, supply vulnerabilities and geopolitical volatility (a trend already visible in other sectors, such as green technologies, critical raw materials and semiconductors).

- European Commission President Ursula von der Leyen has made transforming the European Union's defense industrial base a priority for a potential second term (2024-2029).

- A September 2023 study by the French think tank IRIS showed how the vast majority of European defense spending was going to foreign companies, with the European Union sourcing nearly 80% of its weapons from contractors outside the bloc (and more than 60% from the United States alone). Moreover, according to the European Defense Agency, only 18% of EU arms procurements are currently done in a cooperative manner, which Brussels aims to increase to 40% by 2030.

- The European Union's 2022 Strategic Compass called for adjusting the bloc's defense capability planning and development, and addressing critical deficiencies by 2025 in key strategic enablers like airlift, space communication assets and cyber-defense capabilities while prioritizing next-generation assets, such as main battle tanks. The same year, the Defence Investment Gap Analysis introduced the European Commission's proposal for a gradual transition toward a collective EU defense programming and procurement approach to assist member states in more effectively identifying and addressing capability needs.

- Donations to Ukraine are significantly impacting the readiness of European armed forces, which were unprepared to support a large-scale, high-intensity, prolonged conventional war. Where possible, donated equipment will be replaced and augmented in a process that will take several years in light of the underinvestment of the past decade.

Despite the European Commission's push, EU member states' disagreements over how to finance the initiative, as well as what role Brussels will have in coordinating aspects of arms sales and procurement, will pose significant constraints. The commission's strategy will need to be approved by the European Parliament and member states, which have traditionally been protective of their sovereignty when it comes to defense planning and spending. Moreover, the strategy's implementation into concrete policy proposals will hinge on the composition of the next European Parliament and European Commission following EU elections in June. Meanwhile, although the need to achieve strategic autonomy on defense and foster a resilient military-industrial base in the bloc is widely supported across the bloc, significant differences remain among member states over the scale and type of financing for the initiative, as well as what role Brussels will have in coordinating aspects of arms sales and procurement. While the European Commission has so far only earmarked 1.5 billion euros for the EDIP until 2027, significantly transforming the bloc's military-industrial complex will require much higher spending levels. European Commissioner for Internal Market Thierry Breton said as much as 100 billion euros were needed to achieve the goals of the strategy. But that would require joint borrowing — a highly problematic proposal for fiscally conservative member states like Germany and the Netherlands. Without a substantial funding increase, plans for a new joint procurement mechanism will not have a significant impact. Many of the initiative's objectives and proposals will likely be watered down once they're translated into concrete policy proposals due to disagreements on spending, centralization of responsibilities, and potential interoperability issues with NATO that could emerge over time. However, exogenous shocks like further Russian advances in Ukraine or a significant deterioration in transatlantic relations (as a result, for example, of former U.S. President Donald Trump being re-elected in November) could, at least in part, help overcome these constraints.

- France, Estonia and Poland are reportedly pushing for an EU joint spending approach on defense modeled after the bloc's response to the COVID-19 pandemic, calling for the issuing of EU-backed debt to finance common defense priorities in the bloc. Another option on the table would be using EU cohesion funds, while the European Commission's strategy explicitly mentions the goal of changing the European Investment Bank's lending policy to unlock financing for defense investment (something that is currently not allowed).

- Several member states are skeptical of the European Commission potentially centralizing certain aspects of defense procurement. Some member states — including France, Germany and Italy — are reportedly pushing back some aspects of the strategy, demanding Brussels remain focused on the initial stages of development instead of expanding its influence into procurement, where they believe maintaining competition is crucial.

- Smaller states in Eastern and Northern Europe see Russia as a more imminent threat, and thus see rearming as a more compelling priority, compared with their Western counterparts like France, Germany and Italy. These eastern and northern countries are, in turn, more skeptical of the buy-European approach of the commission's strategy and would rather prioritize commercially made, readily available systems from whoever is ready to provide them first and at better terms. Many of these countries' armed forces are deeply integrated with NATO standards and equipment, a significant portion of which comes from the United States, which gives ground to worries that European products may not be as interoperable with their current equipment. Should the European Union push to gradually develop its own standards in its efforts to boost its military-industrial complex (something the European Commission has ruled out), countries like Poland, as well as all the Baltic and Nordic countries, would likely push back against the initiative.

Achieving the goals of the strategy will ultimately depend on a sustained expansion of national defense budgets in Europe, but this will likely be curtailed by funding limitations and rising economic challenges in the short term, and changing spending priorities and unfavorable demographics in the longer term. Achieving an EU-wide defense industrial ramp-up hinges on a rise in the volume of orders by member states, which can only materialize through a sustained expansion of national defense budgets. Over the next few years, rising military spending in Europe will be directed at strengthening European countries' readiness levels and covering existing gaps in their weapon stockpiles that have been depleted by ongoing military support for Ukraine — a trend that will likely accelerate for as long as the conflict in Ukraine continues. However, a series of material and structural constraints will temper such spending increases. In the short term, low economic growth across the European Union — combined with high interest rates, debt servicing costs and energy prices — will continue to reduce the purchasing power of defense budgets and weigh on public spending decisions in Europe, likely translating into more modest defense investment than originally announced by many European governments in the wake of Russia's February 2022 invasion of Ukraine. In the longer term, other issues will also likely attract growing attention from European policymakers, potentially diverting resources from military rearmament. Both national governments and the European Commission will keep energy security and the net-zero transition at the top of their agendas. To this end, important state resources will be directed toward supporting the decarbonization of industrial processes and the expansion of manufacturing capacity for green technologies and products in the form of industrial subsidies, tax credits, state guarantees and public investment. Demographics will also play a major role in determining spending priorities in Europe for the rest of the decade and beyond. An aging population, particularly in Western Europe, means a growing share of public spending will be dedicated to maintaining an increasingly expensive welfare system across most countries as they grapple with rising healthcare costs and a shrinking workforce. Against this backdrop, European defense spending will continue to grow, but the extent to which it will do so will most likely depend on various socioeconomic developments and how they influence European governments' spending priorities.

- Following Russia's invasion of Ukraine in 2022, several European countries committed to meeting (or exceeding) NATO's target of spending at least 2% of their GDP on defense, in many cases accelerating existing plans to do so by several years. NATO estimates for 2023, however, show that while member states are pouring significantly more money into their militaries as a direct result of the ongoing war in Ukraine, most European allies are still largely lagging behind the 2% spending target.

- European military budgets through 2030 will also increasingly reflect a shift in priorities among most countries, with purchases of new equipment aimed at helping European militaries move away from counterinsurgency capabilities to combat systems designed to counter robust nation-state threats — most immediately, from Russia. As highlighted by new procurement contracts across most European countries, more investment will go into armored tanks (as opposed to only light-armored mobile fighting vehicles), air defense, drones and electronic warfare.

- Overall, defense spending projections will vary depending on the energy and economic situation in Europe and globally, and on the evolution of the war in Ukraine. If, as is likely, the war turns into a frozen conflict, it will reduce the sense of urgency among European politicians and citizens regarding the need to increase military spending.