Increasing security competition in Asia and Europe will lead to a significant acceleration of national defense spending over the next decade, but defense spending measured as a share of GDP will remain below levels seen during the Cold War, which will limit the extent to which unproductive defense expenditure will be a drag on economic growth. Recent remarks by former U.S. President Donald Trump about the need for European NATO member states to increase military spending have reignited a debate over the issue. While several EU and NATO officials have criticized Trump, military spending is nevertheless on the rise in Europe and elsewhere. Following the end of the Cold War, global defense expenditure declined sharply. The United States proved a notable exception among the world's largest economies against the backdrop of Washington's wars in Afghanistan and Iraq. As a share of global GDP, global military spending in 2022 was virtually unchanged compared with 2013. In aggregate, defense expenditure expanded in line with nominal GDP growth. But this masks important shifts in military spending on country-by-country and inter-regional levels. In real terms, U.S. defense expenditure increased less than 3% in 2013-22, while Chinese, Indian and Korean spending increased 63%, 47% and 37%, respectively. Japanese defense expenditure also increased by 18%.

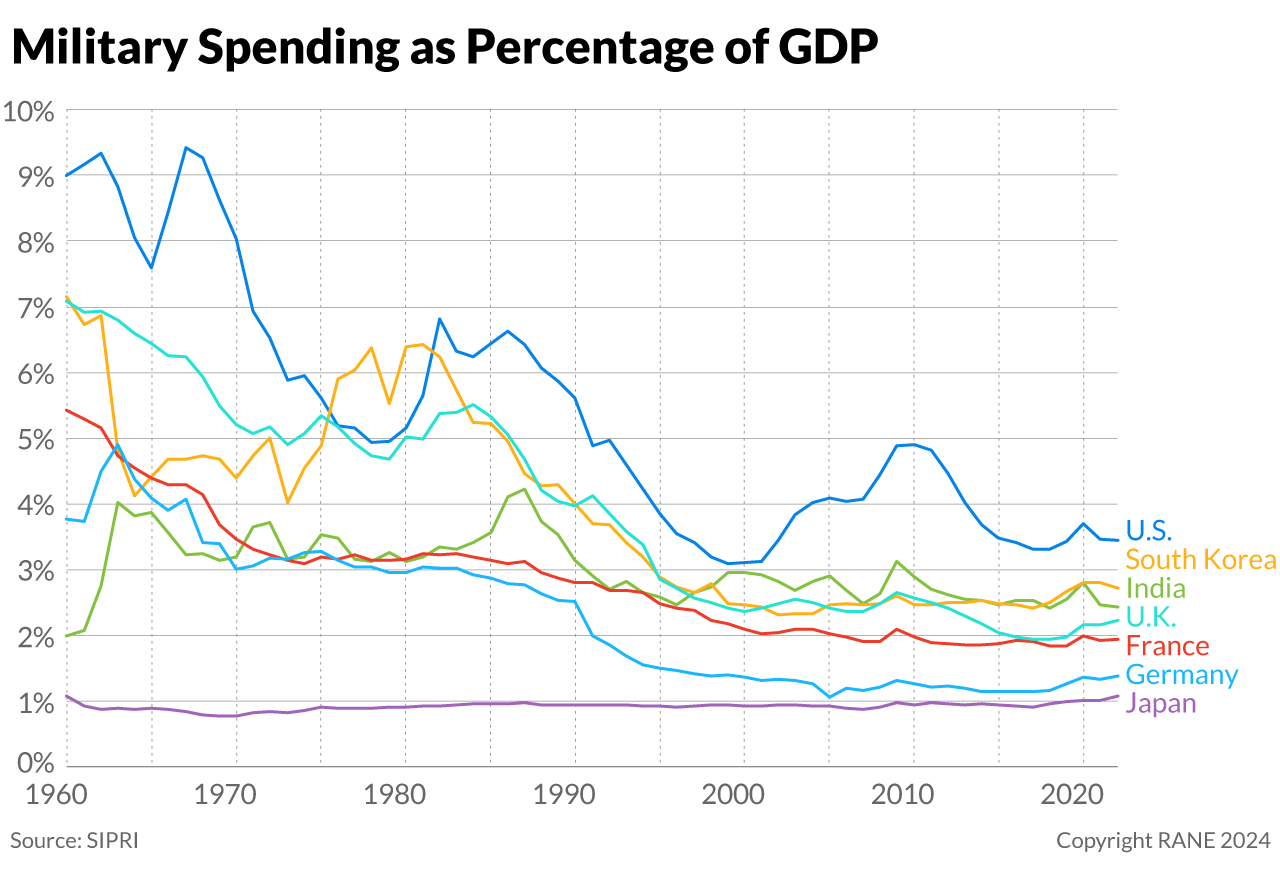

- In the three decades following the end of the Cold War, global defense expenditure as a share of global GDP fell from 4% to 2%. U.S. defense spending increased sharply in the early 2000s, peaked at just under 5% of GDP in 2010, and has since declined to below 3.5% of GDP.

- Global military spending reached $2.2 trillion in 2022, up from $1.8 trillion in 2013. The five largest spenders accounted for almost two-thirds of total spending. The world's leading countries by military expenditure in dollar terms in 2022, in order, were the United States ($877 billion), China ($292 billion), Russia ($86.4 billion), India ($81.4 billion) and Saudi Arabia ($ 75 billion). The fifteen largest spenders accounted for more than 80% of global spending.

- Defense expenditure as a share of GDP varies significantly. Among the top 15 countries, Russia, Saud Arabia, Ukraine and Israel spend more than 4% of their GDP on defense. Ukraine's defense spending in 2022 was estimated at a whopping one-third of its GDP amid Russia's invasion at the beginning of that year. In 2024, 18 out of 31 NATO members will meet the alliance's 2% of GDP target on defense spending. In terms of GDP, Kuwait, Qatar, Oman are also major military spenders. Defense expenditure in Europe and East Asia is increasing rapidly.

While defense spending as a share of GDP has not changed much in aggregate, it has accelerated since 2023, driven by intensifying international security competition in Eastern Europe and Asia. The war in Ukraine and geopolitical competition in the East and South China seas and the Indian Ocean are leading virtually all major powers to increase defense spending faster than nominal GDP growth. In contrast, expenditures in South America and Africa have not changed dramatically. The limited conflict in Ukraine since 2014 and the full-scale war since 2022 plus diplomatic pressure by the former Trump administration have forced Russia to raise its defense expenditures significantly. It has also spurred European countries, especially Eastern European countries, to raise their military spending. Against this backdrop of accelerating spending, global arms exports have also increased. Among the G7, Germany and Japan have announced significant increases in military spending over the next few years. Due to higher nominal growth and a larger spending base, the United States and China will account for the largest share of global spending increases, with an anticipated combined defense spending of $2 trillion by the beginning of the next decade.

- Russian defense increased dramatically after its failed attempt to rapidly overrun Ukraine in 2022. In 2024, Russia is set to spend 6% of its GDP on defense, compared to an estimated 4% in 2022 (and 2014). By comparison, Soviet defense spending in the 1980s is estimated to have accounted for 15-17% of GDP. In 2022, the Japanese government announced a 60% increase in defense expenditures by 2027, and Germany pledged to allocate an extra 5% of GDP to modernize its military forces and increase annual defense expenditure over the medium term.

- Many NATO members will increase defense expenditures above their level of economic growth in view of meeting the 2% target set in 2006 and to be reached in 2024. At present, just one-third of NATO members meet the spending target.

- International arms transfers fell 5% in 2013-17 compared to 2018-22. But global imports increased almost 50% in Europe and East Asia while declining in Africa, the Americas, the Middle East and North Africa, and Asia-Pacific as a whole. Imports by South Korea (61%) and Japan (171%) were up sharply. Japan's decision to increase defense expenditure should raise Asian arms imports further during 2023-27.

Defense expenditure will increase tangibly for the foreseeable future in light of military conflict and security competition, but as a share of GDP, it will remain well below levels seen during the Cold War. This means that the impact on fiscal deficit, government debt and medium-term economic growth will be less severe, at least absent the outbreak of hostilities in East Asia or a further significant escalation in the war in Ukraine. At present, the major powers have higher government debt and larger fiscal deficits than they did during the Cold War. Many of the Warsaw Pact countries, including post-Soviet Russia, faced severe financial difficulties, forcing them to sharply reduce defense spending. The end of strategic competition between NATO and the Warsaw Pact also led NATO countries and other U.S. allies to reduce defense expenditure. Since then, social welfare expenditures as a share of GDP is much higher, constraining governments' fiscal space even further. Absent major conflict, whether to increase defense expenditures can be politically challenging, since this often means curtailing social spending and public investment. So defense spending in Europe and East Asia will be gradual unless security competition heats up or military conflict breaks out, rapidly weakening political constraints on spending increases. While expenditures will increase faster than nominal GDP growth in any advanced economy, this may not be the case in the two countries with the world's two largest defense budgets in dollar terms, the United States and China, which account for half of all global defense spending. At 3.5% of GDP, U.S. defense spending is already fairly high and U.S. deficits are already high, while China has historically chosen to keep defense spending below 2% of GDP. Relatively faster economic growth in China, current economic challenges notwithstanding, will nonetheless translate into significant increases in dollar terms. China undoubtedly has far greater scope to raise defense expenditure during peacetime than does the United States, given that Washington already spends twice as much as a share of GDP than China does. Among the top 15 countries with the highest defense expenditures, China is best placed to increase spending in both dollar terms and as a share of GDP. This gives China a tangible advantage in terms of its ability to sustain significant increases in defense spending, something prompting the United States and its allies to cooperate more closely on defense in response.

- Government debt and fiscal deficits in most advanced economies are far higher than during the Cold War. Government liabilities, including future healthcare and pension expenditure, are also much higher and will constrain governments' fiscal space — namely, their ability to increase expenditure without unduly hurting the economy or causing financial instability — in the medium-to-long term. In the short term, political constraints on limiting non-defense expenditure — voters typically do not like to see government spending on public infrastructure or welfare curtailed to support defense spending — higher taxes to finance defense spending or increased borrowing will limit the speed of defense expenditure increases. The greater the perceived threat, however, the more forceful the government will move to spend more, as in Japan.

- In 2022, U.S. defense spending amounted to 3.5% of GDP, while Chinese defense spending was 1.7% of GDP. In dollar terms (at market exchange rates), U.S. spending is three times larger than China's ($880 billion versus $300 billion). Faster Chinese economic growth will allow it to increase spending faster, even without raising spending levels as a share of GDP.

- Under reasonable economic and financial assumptions, U.S. defense expenditures could reach $1.3 trillion by 2030, up from less than $900 billion today. Chinese expenditure is set to increase from $300 billion today to $500 billion. 2030 defense expenditure would be equivalent to 3.5% of GDP in the United States and 2.2% of GDP in China.

The coming decade will be characterized by higher defense expenditure, which at the margin will prove a drag on medium- to long-term economic growth, though perhaps not in the short term. The acceleration of economic growth and global prosperity after the end of the Cold War was underpinned by globalization, the integration of China into the world economy, supply-side reforms, and economic liberalization and technological innovation. Investment and economic growth also benefited from the significant reduction in military spending made possible by the end of the Cold War. Downsizing the armed forces and reducing relatively unproductive defense spending helped generate fiscal savings, lowered interest rates, increased non-defense investment and boosted the civilian labor force. Increased military expenditure going forward, like most deficit-financed government spending, may help boost short-term economic growth, particularly in the presence of spare capacity. But in the longer term, the diminished availability of savings, higher interest rates and more limited productivity-enhancing investment will weigh on long-term growth outlook. To the extent that governments run larger fiscal deficits or simply increase relatively unproductive military spending, this should weaken countries' medium- to long-term growth potential, particularly if the economy is already operating at full capacity. To the extent that an economy benefits from excess savings, like China's does, the scope to raise defense spending without unduly reducing growth potential is far greater than in, for example, advanced countries characterized by lower savings rates and more challenging medium-term budget and debt dynamics. Higher defense spending will tend to support economic growth in the short term, but in the longer term it will likely prove a drag. This is because military expenditure generates at best limited productivity gains than, for example, investment in public infrastructure or research focused on civilian technology.

- Over the next decade, real GDP growth (unadjusted for purchasing power parity) will average at most 2% annually in advanced economies, compared to 4-5% in China and 5-7% in India. This will allow China and India, already the second- and fourth-largest defense spenders in dollar terms, to significantly raise spending and invest in new capabilities. Less rapidly growing economies will not be able to match spending increases dollar-for-dollar even if they were to raise defense spending as a share of GDP. Defense expenditure as a share of GDP varies, ranging from 1.1%, 1.4% and 1.6% of GDP in Japan, Germany and China to 2.4%, 2.7% and 3.5% of GDP in India, South Korea and the United States.

- To the extent that China's economic problems are related to excess domestic savings, increased defense spending affords it far greater financial scope than more slowly-growing, more savings-constrained advanced economies in Europe and East Asia. China is the least savings-constrained economy, with savings amounting to almost 50% of GDP. By comparison, Japan has savings amounting to 23% of GDP and the United States 17% of GDP.