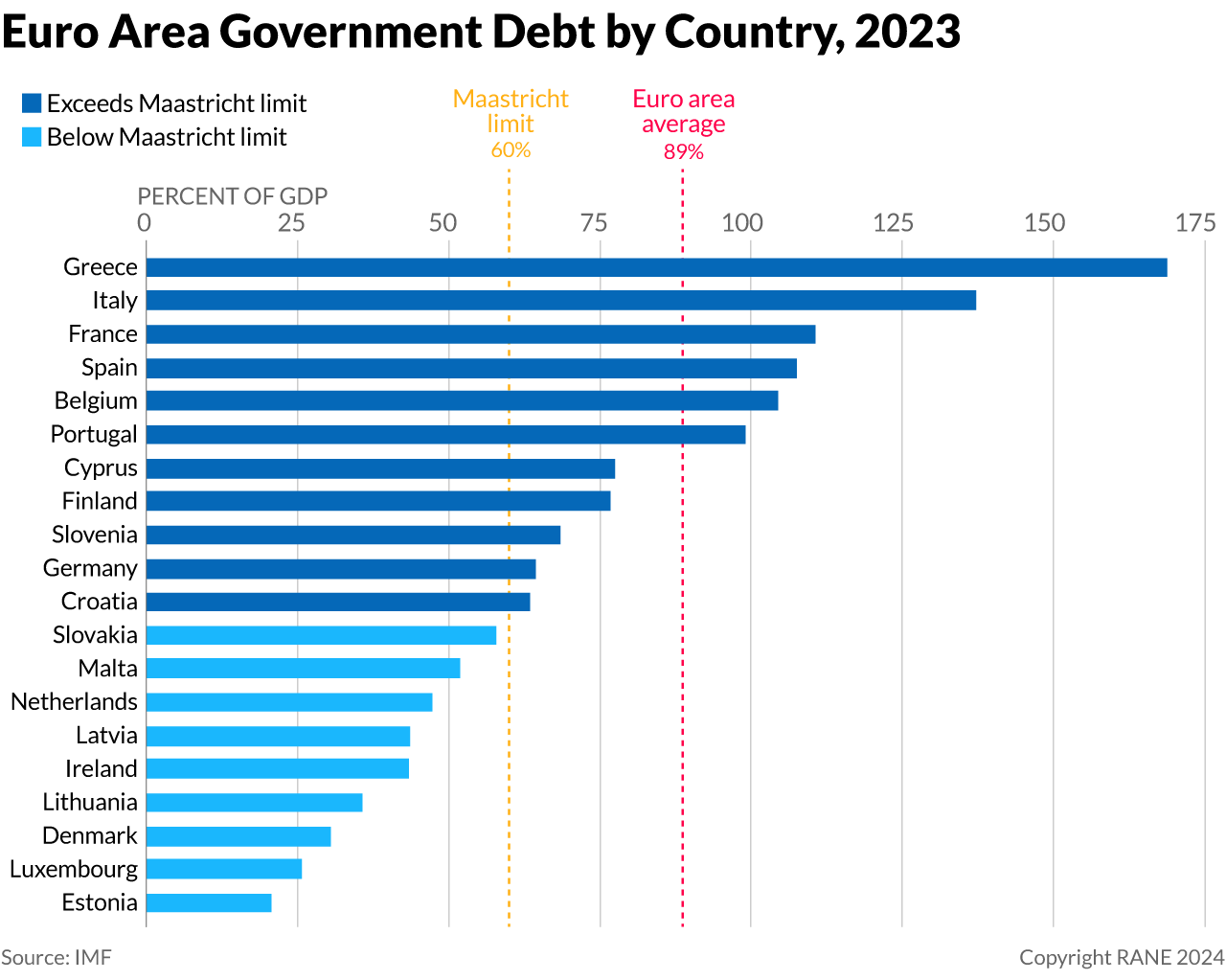

In the eurozone, the end of extraordinarily low interest rates and extensive quantitative easing policies will put increasing pressure on government budgets, while continued low growth and already high debt burdens will render government finances less than solid; while the extensive reform of the euro area over the past 15 years has made the single currency much more resilient, it is still more vulnerable to endogenous and exogenous shocks than regular national currencies, such as the U.S. dollar. France recently suffered a sovereign credit downgrade in the wake of an unexpectedly weak fiscal performance, large deficits and increasing government debt, which now exceeds 100% of GDP. Markets took the news in stride, and France's financing costs barely changed. While France is not at risk of financial destabilization, continued high government in two of the three largest euro area members is a reminder that fiscal risk continues to linger, particularly in the context of higher nominal interest rates and quantitative tightening in the euro area.

The financial reforms that were introduced in the context of the euro area crisis 15 years ago have since helped limit the risk of broader financial crises. The euro was created in 1999-2002. In the first decade of its existence, the currency contributed to economic and monetary convergence among its members, as capital flowed from the low-interest core to the high-interest periphery, leading to an economic and financial boom. However, it also led to a gradual build-up of financial vulnerabilities in the context of overborrowing by governments and excessive lending to the real estate sector by banks. Then, in late 2009, the Greek government was forced to acknowledge it had systematically underreported its fiscal deficit, plunging the euro area into a debt crisis that almost led to the financial and institutional collapse of the single currency, as it risked forcing significant losses on banks in the eurozone, and cast doubt on the creditworthiness of highly indebted governments. The fact that Greece's financial woes were able to pose such an existential threat to the eurozone was due largely to the constraints imposed by the bloc's Economic and Monetary Union (EMU), which was established in 1999 as an incomplete — or at least structurally vulnerable — monetary union. Among other things, the EMU included a provision that prohibited the ''bailout'' of member governments, which was meant to preserve monetary stability by forcing eurozone members to pursue fiscally prudent policies. But this ''no bailout'' clause also makes the euro vulnerable to destabilizing financial contagion by leaving the regime without a key instrument to backstop governments and the banking system in financial trouble, beyond the national level. And while other EU rules sought to obligate members to maintain low government debt and small fiscal deficits, the accompanying enforcement mechanisms were too weak. Once signs of financial distress emerged in 2009-10, investors thus began analyzing the various cross-cutting financial linkages — including those linking Greek government debt to European and Cypriot banks, as well as those linking weakened banking systems to generally financially solid sovereigns (like in Ireland and Spain). And this, in turn, forced the euro area to address the immediate consequences of the crisis and implement broader reforms to reduce the risk of future crises.

- Typically, central banks act as a lender of last resort, not just to the banking system but also to the sovereign. But when the euro area debt crisis emerged 15 years ago, the ECB was prohibited from playing this role due to the EMU provision that banned the bank from providing monetary financing to member states.

In the face of the quasi-existential debt crisis, the euro area has seen major institutional reform, which have helped make the single currency more resilient. In 2010, the European Union began cobbling together financial rescue programs to contain financial contagion and prevent a broader financial breakdown of the currency area. This included the European Stability Mechanism (ESM), which provides the euro area with financial resources to bail out distressed member states and (indirectly) provide financial support to backstop banking sector crises. The euro area also reformed its fiscal regime and made some, if limited progress toward establishing a banking union in an attempt to prevent future sovereign crises to spill over into the banking sector as well as minimize the risks of a banking crisis causing sovereign financial distress (so-called sovereign-bank nexus). However, it was the ECB — with its notionally unlimited financial resources and its commitment to do ''whatever it takes'' — that primarily helped stabilize the euro area. Greece received financial bailouts in 2010 and 2012, Ireland in 2010, Portugal in 2011, and Cyprus in 2013. Banking crises in Spain, Ireland and Cyprus led the respective governments to request financial bailouts, which, in the case of Cyprus, was accompanied by a bail-in of bank depositors. The Greek government also restructured its debt in 2012 and has engaged in several voluntary debt exchanges since then.

- During the initial emergency in 2010, euro area members were forced to provide financial support to prevent broader financial contagion and the systemic destabilization of the euro area. This took place, first, in the guise of the European Financial Stability Mechanism (EFSF) and the European Financial Stability Mechanism (ESFM). Due to their limited size, both funds were replaced by the newly established only euro area member-funded European Stability Mechanism (ESM) in 2012. The ESM today effectively functions as a euro-area International Monetary Fund, providing financial resources to distressed members in exchange for economic adjustment and reform.

- In the wake of the crisis, the ECB created new instruments to stabilize markets. Through the Securities Markets Programme (SMP), the central bank aimed to contain long-term interest rates in weaker countries. In 2012, it launched Outright Monetary Transactions (OMT) to backstop sovereign debt under strict policy conditions. In 2022, the ECB introduced the Transmission Protection Instrument (TPI) to ensure smooth monetary policy transmission and manage interest rate spreads by purchasing unlimited medium- and long-term debt securities, provided countries follow sound fiscal policies and EU rules. The ECB also established the Public Sector Purchase Programme (PSPP) for large-scale purchases of non-sovereign financial assets. During the COVID-19 pandemic, it created the 1,350 billion euro Public Emergency Purchase Programme (PEPP). Central bank purchases of sovereign debt help lower borrowing costs but are viewed by some as monetary financing of government debt.

- The euro area members also implemented several reforms of their fiscal regime. In 2011, the euro area introduced the so-called ''six pack'' of regulation aimed at tightening the rules of the Stability and Growth Act. In 2012, the fiscal compact was replaced by and rolled into the Stability and Growth Pact and further tightened the fiscal regime governing national financial policies in terms of restrictions and enforcement of rules, adjustment requirements and transparency. The fiscal compact subjects member countries' fiscal policies to European Commission surveillance, commits countries to a mandatory balanced budget rule, strengthens the excess deficit procedure, and requires convergence toward medium-term objectives, among other provisions. The EU fiscal rules were updated in 2024 to make them less complex and hence less complicated to enforce.

- Following the 2009 crisis, the euro area took steps to limit the risk of systemic banking crises as well. In 2014, it established a Single Supervisory Mechanism (SSM), which gives the ECB supervisory powers over large euro area banks (smaller banks largely remain under the supervision of national authorities.) It also created a Single Resolution Mechanism (SRM) to allow for the orderly resolution of banks, along with the Single Resolution Fund (SRF), which is meant to help resolve failing banks in case bail-ins are not viable and prevent disorderly bankruptcies in the banking sector through the bailing in of creditors or an orderly winding up. The SRF is funded by banks and is meant to cover 1% of all euro area deposits. In 2015, the European Commission(?) also proposed establishing a European Deposit Insurance Scheme to limit the risks and costs to governments of bank failures, but the proposal was never adopted. A recent reform, currently in the process of being approved, seeks to deploy the ESM as a backstop to the SRF through a revolving credit line.

Although the euro area proved resilient in the face of recent shocks brought on by the COVID-19 pandemic and the war in Ukraine, the current institutional architecture continues to make it vulnerable to severe shocks. The eurozone architecture is incomparably more robust than it was 15 years ago, but it still has key weaknesses, particularly compared with nation-states with national central banks and a more centralized fiscal authority. First, while the euro area's financial rescue mechanisms have made the system more resilient, their funding capacity is limited. This is why the ECB's OMT is an indispensable element of the euro area's financial architecture, as it provides the financial firepower to credibly backstop even larger member governments. Second, the financial firepower of the SRM is also quite limited. Again, while the ESM provides additional financing under certain conditions, the financial capacity — accounting for just 1% of euro area banking deposits — is small, particularly if there is no additional explicit or implicit actor able and willing to backstop the system in case of a severe crisis. In addition, national banking systems in many eurozone countries remain vulnerable given their government's limited ability to backstop the system and no common eurozone-wide deposit insurance. This will exacerbate bank runs in moments of crisis, as local depositors will move their money to euro area countries not at risk of default of currency denomination. Since the end of the euro area debt crisis in the mid-2010s, euro area governments have benefitted from low nominal interest rates and extensive central bank purchases of their sovereign debt. While they have thus far weathered higher policy rates, it remains to be seen how well they will cope with higher interest rates, as well as wider spreads. The medium- and long-term financial outlook will also prove challenging in view of the need to increase spending on defense and the green transition, as well as social welfare amid Europe's aging population — something that will be particularly challenging for countries with low economic growth, such as Italy. These pressures may, in turn, erode support among eurozone governments for prudent fiscal policies and compliance with euro-area fiscal rules, leading to increased conflict with national-level fiscal priorities and euro-area-level restrictions. This in itself has the potential to upset markets and lead investors to charge higher interest rates, thus exacerbating the financial outlook of financially challenged countries.

- Euro area government debt has increased significantly in euro terms, hence relative to the financing capacity of the ESM. Italian and French government debt amounted to around 3 trillion euros in 2023, or 140% of GDP and 110% of GDP, respectively. Domestic credit to the private sector — a proxy for the banking sectors' non-sovereign lending, as well as sovereign contingent liabilities in the case of a banking sector bail-out — stood at 70% and 120% of GDP, respectively. Meanwhile, the ESM's total lending capacity amounts to a measly 500-700 billion euros.

- The recently created NextGenerationEU or European Union Recovery Instrument, adopted in 2020, provides for common EU funding financed by EU-level resources. But the financially stronger, net payer governments have made it clear that it will remain a one-off, running from 2021-2027 and providing a mere 750 billion euros to support post-pandemic investment and reform. However, the financial challenges of many of the weaker euro area members are much larger in financial scope and time horizon. The new instrument is thus a drop in the bucket as far as the longer-term fiscal challenges are concerned.

The politics of euro area reform and crisis-proofing remain contentious, which will continue to impede progress toward such reforms in the coming years. Absent another major shock, the euro area will likely prove sufficiently resilient in the next few years. At the same time, the euro area is unlikely to suffer any defections due to popular opposition in member countries or adverse legal rulings that undermine key elements of the current financial-institutional architecture. The euro remains very popular in virtually all euro area countries, and legal challenges brought against the new financial architecture have been largely, if not completely defeated by national constitutional or European courts. This short-term stability will reduce the urgency for major progress toward crisis-proofing eurozone reforms, which have long proved controversial by pitting low-debt ''creditor'' countries in Northern Europe against high-debt ''debtor'' countries in Southern Europe. Although all member countries have an interest in increasing the resilience of the euro area to shocks, they disagree as to how to distribute the actual and potential costs of the reforms. Reforms that risk creating a so-called ''transfer union'' by enshrining the possibility of a permanent resource transfer are not attractive to creditors, financially, economically or politically. The creditor countries retain veto power of any such reform. This is also why any resource transfer and risk sharing is limited and typically conditional, whether this relates to emergency lending, banking resolution or banking union. Financially more vulnerable countries — namely, countries with large government debt and a banking sector that owns a large amount of that debt — are simply not in a position to significantly contribute to risk sharing. The eurozone's fiscally conservative countries will continue to resist reform aimed at substantially greater risk-sharing or resource transfers. And debtor countries will continue to oppose institutional reform that transfers the costs of financial distress — whether in terms of macroeconomic adjustment, sovereign debt restructuring or banking sector insolvencies — to financially weaker countries. Unless another major, systemic crisis emerges in the coming years that forces eurozone members to implement far-reaching changes to the present regime, reform will thus be slow. And this, in turn, means risk-sharing and direct or indirect resource transfers are unlikely to significantly increase in the near future.

- The interests of fiscally conservative, largely Northern European countries (like Germany, the Netherlands, Ireland and the Baltic countries, whose government debt levels are all less than 70% of GDP) continue to diverge with the interests of less financially disciplined Southern European countries (like Greece, Italy, France, Spain, Belgium and Portugal, whose government debt levels all exceed 100% of GDP). The former group broadly opposes significant resource transfers and significant direct or indirect risk-sharing, while the latter group opposes more rigid rules and a loss of policy discretion.

- Virtually all euro area governments face significant long-term fiscal challenges caused by a combination of aging populations and welfare systems, including pension and health spending. In addition, increased spending on the green transition and defense will also put upward pressure on fiscal deficits and, in most cases, government debt ratios. Significant fiscal reform necessary will prove politically controversial. It will make it unlikely for significant intra-euro redistribution to take place.

Without significant fiscal reform, the eurozone will remain vulnerable to both endogenous and exogenous shocks in the coming years and decades. An obvious longer-term challenge the euro faces is a combination of low economic and fiscal restraint that can undermine support for the euro and lead politicians and political parties to support euro exit. Although the economics of common currency areas are complicated, most voters in eurozone countries appear to intuitively understand the economic benefits of membership in the EU single market, and that if their country were to exit the euro area, it would prove a financial disaster by likely also forcing their country out of the single market. This has so far forced populist parties to back away from calls to leave the single currency. But while support for the euro is currently high in all euro area member countries, popular opinion can change quickly if euro area membership were to be associated again with economic conditionality and financial crises. Indeed, whatever the short-term costs of euro exit, politicians may support replacing the euro should electorates become fed up with the economic status quo of low economic growth. In the short term, an unanticipated shock could lead to economic and financial destabilization capable of overwhelming the euro area financial architecture. Such a scenario might materialize where one of the larger member countries refuses to abide by the euro area rules, submit its policies to policy review and becomes ineligible to receive rescue funds or benefit from an effective ECB bailout, perhaps in an ill-fated attempt to force the euro area to provide more favorable bailout conditions. In a more likely scenario, a larger euro area member country may also get into significant financial trouble at a time when the domestic political constellation prevents it from adjusting policies and where the available bailout funds prove potentially insufficient. In addition to sovereign debt crises within the eurozone, future external shocks could also trigger destabilizing crises in the currency area, such as those brought on by global conflicts and/or prolonged global economic stagnation.