Officials from Germany, Ghana, Canada, Japan, the United Kingdom, the African Union, the European Union, France, the United States and Kenya participate in a working session at a G-7 Foreign Ministers Meeting in Muenster, western Germany, on Nov. 4, 2022.

The Group of Seven (G-7) major economies are generally well-positioned to ride out rising interest rates and the impending global recession without sliding into a broader systemic debt crisis. Italy, however, may be the one exception. As central banks around the world try to contain rising inflation, they are increasing their nominal interest rates for the first time since the global economic crisis in the late 2000s. Rising interest rates make government debt service more onerous. And since the government debt of developed nations is already high, worries about debt sustainability are on the rise. The United Kingdom recently exemplified this situation when yields on the country's long-term bonds (also called gilts) spiked following former Prime Minister Liz Truss's ill-considered fiscal policy decisions in early September. While Truss's resignation and the appointment of new U.K. Prime Minister Rishi Sunak in late October helped reverse bond and currency losses, some observers interpreted rising bond yields and the very negative market reaction to Truss's policies as a reflection of heightened sovereign default risks, which might also other developed nations. However, the economic fundamentals of most G-7 countries suggest that a debt crisis remains unlikely in the short-to-medium term.

- Shortly after taking office on Sept. 5, Truss announced billions of pounds in unfunded tax cuts against the backdrop of high inflation and central bank tightening. Increased volatility in the British gilt market forced pension funds to sell their long-term gilts to raise cash, further exacerbating the market sell-off and forcing the Bank of England to intervene by purchasing longer-dated government debt securities.

- From when Truss took office to the end of September, 10-year yields on U.K. government bonds increased from 3.5% to 4.5%, before falling back to 3.5% at the beginning of November (one prime minister later). Similarly, the U.K. pound's value fell from 1.16 against the U.S. dollar when Truss took office to 1.07 against the dollar at the end of September, before recovering to 1.16 in November.

- The yield curves of other G-7 countries remained relatively stable during the United Kingdom's mini-financial crisis, and volatility did not spike significantly.

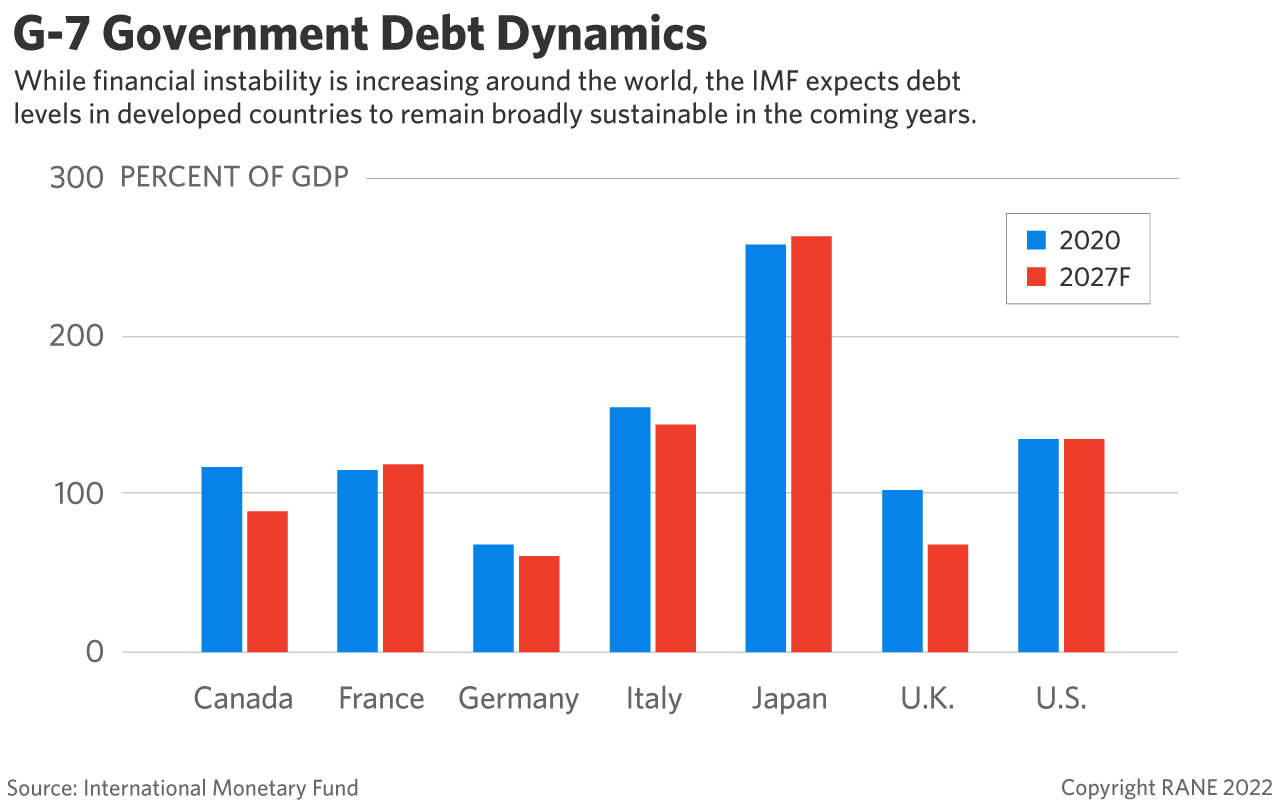

The United Kingdom's mini-financial crisis does not indicate a significant increase in present or future sovereign default risk in most G-7 countries because medium-term debt dynamics point to a declining debt-to-GDP ratio, or a manageable increase. While financial instability is increasing around the world, G-7 countries are overall poised to weather the global economic downturn without entering a wider debt crisis akin to what the eurozone experienced a decade ago, because they have greater flexibility to adjust to economic shocks than upper-middle income or low-income countries with less fiscal space and less robust public finances. The recent financial volatility in the United Kingdom instead largely reflected higher inflation premiums (investors requiring higher bond yields to offset higher inflation) and the liquidity position of U.K. pension funds. Structurally, British gilts and the pound had also been under pressure long before Truss took office due to rising U.S. interest rates, a stronger U.S. dollar and investment flight from high-risk assets due to geopolitical risks. This means the recent market turmoil triggered by Truss's controversial tax cuts simply accelerated an underlying trend and does not indicate increased risks of sovereign debt default in the United Kingdom or elsewhere in the developed world. In fact, according to the International Monetary Fund (IMF), gross government debt will not increase in Canada, Germany, Japan, Italy or the United Kingdom between now and 2027. While the IMF projects that gross government debt will increase in France and the United States within that time frame, France's debt increase will be small and manageable, and the United States can sustain higher debt levels since it is the dominant reserve currency issuer.

- Five-year British sovereign credit default swaps, whereby investors insure against a sovereign debt default, increased by 20 basis points during the United Kingdom's mini-financial crisis. But assuming a 40% recovery rate, the United Kingdom's five-year default risk remained at well below 1%, making it difficult to argue that the United Kingdom was facing a meaningfully increased risk of default.

- The IMF projects that U.K. public debt will fall from over 100% of GDP in 2020 to less than 70% of GDP by 2027. These projections may not account for Truss's proposed tax cut measures, but the institutional investment manager Schroders estimated that the measures would have added only 13% of GDP worth of debt, which would have been more than offset by the projected sharp drop of 30 percentage points in the United Kingdom's debt-to-GDP ratio.

- Germany and the United Kingdom are set to experience a tangible decline in their government debt-to-GDP ratios due to cyclically adjusted primary surpluses (an excess of government revenues before paying interest) over the next few years. The debt ratios in Italy and Japan are also set to remain unchanged due to a sufficiently favorable combination of real GDP growth, interest rates and primary fiscal balances.

- The United States will see a continued increase in its gross government debt levels, reaching 135% of GDP in 2027. While this will be substantially higher than in 2020 when the ratio stood at 109% of GDP, it is at virtually the same level as in 2021.

Italy, however, is the G-7 country most at risk of a sovereign default due to its high debt levels, very low economic growth potential, and significant vulnerability to market sentiment shifts amid rising interest rates in the euro area. Besides Japan, Italy has the highest government debt-to-GDP ratio and the lowest potential growth rate among G-7 countries. Italy will also face tangible risks over the next few years as the European Central Bank (ECB) increases interest rates and considers shifting toward a policy of quantitative tightening, effectively raising long-term interest rates. At high debt levels, even small changes to interest rates and the growth outlook can shift market sentiment and increase financial stability risks. The ECB will not deploy its entire balance sheet to support Italy's government debt dynamics unless the Italian government commits to sustainability-oriented economic policies, which may prove politically challenging. The ECB's efforts to add new monetary instruments to its toolkit will prove insufficient, particularly if ECB monetary tightening leads to structurally higher real interest rates. In this scenario, Italy will be faced with higher financing costs and deteriorating debt dynamics, which may increase sovereign credit risk.

- At 150% of GDP, Italy's government debt levels are high. Running a small primary surplus of 0.5% of GDP, as the country is currently doing, would be insufficient to offset a significant increase in real interest rates.

- If real interest rates rise to 2% from currently negative 8%, Italy would be forced to raise its primary surplus by 1% of GDP on an ongoing basis just to stabilize debt at current levels — highlighting the country's exposure to volatile market sentiment.

- In July, the ECB introduced yet another monetary tool — the Transmission Protection Instrument (TPI) — to pre-empt sovereign debt volatility in the eurozone. The TPI bond-buying program is meant to prevent ''fragmentation'' in the currency area, which occurs when the borrowing costs for some countries increase much more than others. However, it is difficult to see how the ECB could commit to purchasing unlimited amounts of Italian government debt to prevent Italian yields from increasing, as, for a start, this could trigger legal challenges that would further undermine the TPI's credibility. Such legal risks will force the ECB to wield the new instrument with great caution, thereby limiting its effectiveness. The new right-wing government in Rome may, in turn, have to adopt a tighter fiscal stance and more unpopular austerity measures to qualify for the ECB's main crisis-fighting tool (Outright Monetary Transactions), at the risk of weakening its political position.