An increasing number of emerging and developing economies are experiencing financial distress, raising the risk of a wave of sovereign debt defaults. This financial distress is occurring against the backdrop of higher food, energy and import prices. A few countries, including Sri Lanka and Zambia, have already defaulted on their external debt payment obligations, while a much larger number — including Bangladesh, Ghana, Pakistan, and Serbia — has approached the International Monetary Fund to request financing, often a precursor for sovereign debt restructurings. Though beset by a variety of economic and financial problems of their own, larger emerging economies like China, India, Mexico and Brazil have a fair net external debt positions on account of low debt, large foreign exchange reserves, or both.

- As of July, Bloomberg estimated that $240 billion worth of sovereign debt is trading in distressed territory, meaning at high risk of default. This amounts to almost one-fifth of the $1.4 trillion in emerging market sovereign external debt denominated in hard currency. Bloomberg also estimates that the nearly 20 countries at high risk of distress represent nearly 1 billion people.

- The Bank of Canada and Bank of England estimate that the total value of sovereign debt in default amounted to $376 billion in 2021. While this represents a 15% decline — due largely to the resolution of defaults by Argentina and Ecuador — compared to the $448 billion in default in 2020, larger arrears were registered in countries like Belize, Mozambique, Nauru, Puerto Rico, Suriname, Venezuela and Zambia. Worryingly, the number of distressed countries is increasing.

High levels of debt, combined with a sharp tightening of financial conditions, has made many developing economies vulnerable to economic and financial distress. Since the start of the year, the sharp and unexpected increase in U.S. interest rates has increased debt service costs. A stronger dollar has also put pressure on many poorer countries' balance of payments by increasing their debt servicing costs in local currency terms — putting pressure on borrowers' balance sheets, particularly those relying on local currency revenues to service foreign currency liabilities. Higher U.S. interest rates and the increasing prospect of a recession in both the United States and other advanced economies are also negatively affecting many countries' medium-term growth outlook. Moreover, many low and lower middle income countries have taken on substantial international debt over the past decade, whether through official borrowing from China (often in the context of the Belt and Road Initiative) or in the form of borrowing from international capital markets. The economic and financial shock due to COVID-19 and surging energy and food prices have also contributed to the substantial accumulation of government and external debt in many countries, undermining their ability to mitigate these various challenges.

- The U.S. Federal Reserve's federal funds rate is currently projected to reach 4.6% by end 2023, up from virtually zero at the beginning of the year.

- The trade-weighted dollar is at a 20-year high, adding to financial distress in over-indebted developing countries due to increasing debt servicing costs.

- The pandemic-related economic downturn and higher government spending have increased government debt levels virtually everywhere. The subsequent commodity price shock and energy and food inflation have exacerbated the economic and financial situation, particularly in low and lower middle-income countries.

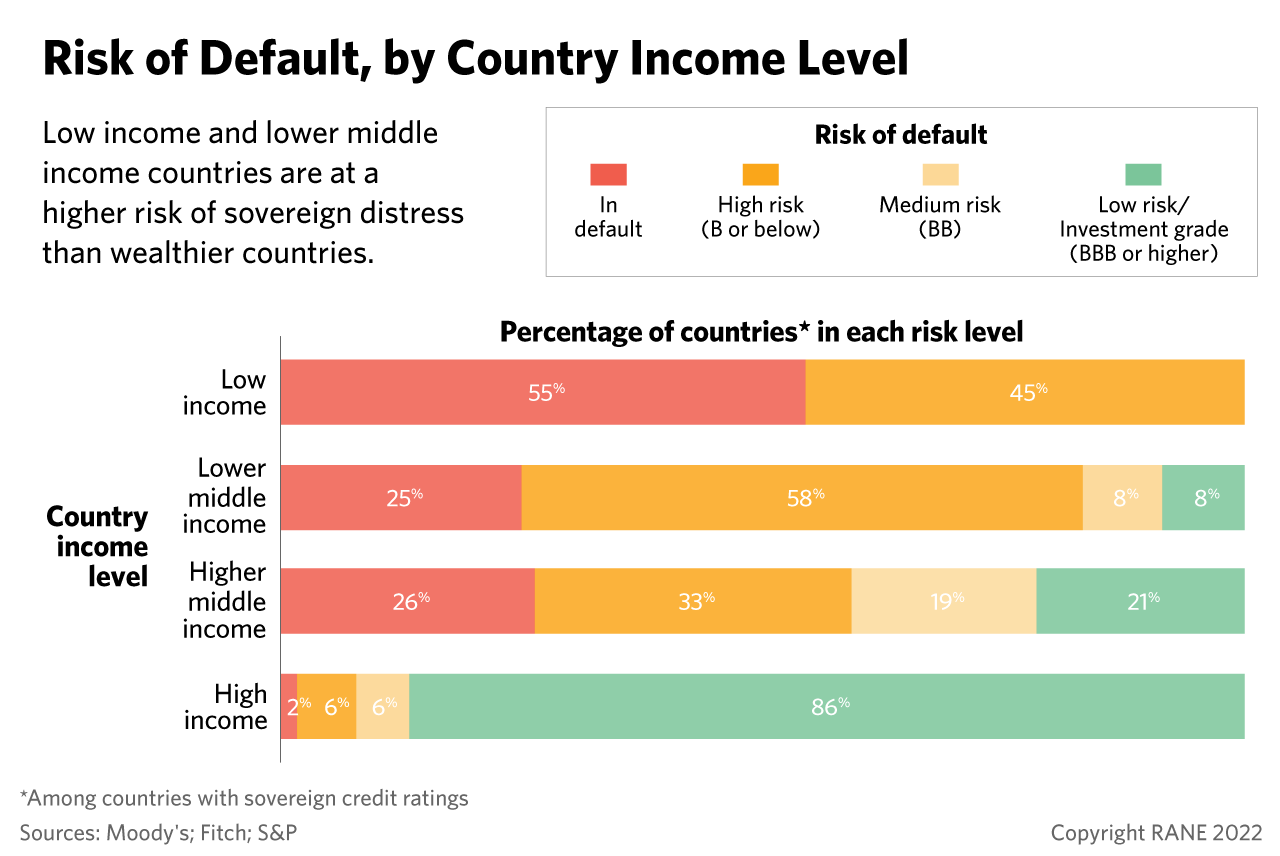

Financial distress in developing and emerging economies will worsen before it gets better, raising the risk of sovereign defaults over the next 24-36 months. Almost 50 countries are at high risk of economic and financial distress and sovereign default. Not all countries will be forced to restructure, but the restructuring risk will be particularly high for low and lower middle income countries facing higher food and energy prices and diminishing foreign reserves amid higher borrowing costs. Disorderly defaults typically cause the greatest degree of economic distress, but even if precautionary IMF programs can help stave off a default, the economic and financial adjustment necessary to stabilize a country will cause significant pain in developing and emerging economies. By contrast countries with high per capita income overall are far less likely to default or experience financial distress than poorer countries. Greater macroeconomic flexibility, more mature financial markets and the ability to borrow internationally in their own currency typically limit financial risks. High income countries, however, are by no means completely shielded from such risks. Slightly less than 10% of all rated high-income countries — including Barbados, Bahrain and the Seychelles – are rated B or below and hence face substantial default risk.

- The Fed is likely to err on the side of caution to reestablish its credibility following the recent surge in inflation and will continue to hike interest rates, causing greater financial distress in developing economies.

- Global foreign exchange reserves have fallen from $12.9 trillion at the end of 2021 to $12 trillion at the end of the second quarter of 2022, pointing to balance-of-payments pressures. Country-level data points to even steeper declines in reserves during the third quarter of 2022.

- Of the approximately 140 countries with a rating from one of the three major credit rating agencies, almost half are rated at B or below by at least one rating agency. This points to a future wave of financial distress and debt restructuring, particularly among poorer countries.

- For those countries where credit default swaps exist, Nigeria, Pakistan, Kenya, Argentina, Egypt, El Salvador Venezuela, Ghana all trade above 1,000 basis points, suggesting they face a high risk of sovereign default.