The headquarters of the European Central Bank (ECB) is pictured in Frankfurt, Germany, on July 21, 2022.

Recent moves by the European Central Bank (ECB) should reduce the risk of a new sovereign debt crisis in the eurozone, but highly indebted countries will still have to step up fiscal consolidation efforts as borrowing costs will continue to increase. On July 21, the ECB announced a combination of measures to contain rising inflation in the eurozone while keeping the gap between member states’ sovereign borrowing costs from widening excessively. The bank increased interest rates for the first time in 11 years, surprising markets with a hike of 50 basis points that brought the ECB’s deposit rate to zero. The ECB also unveiled its new Transmission Protection Instrument (TPI) bond-buying program to prevent individual countries' bond yields from increasing beyond what is justified by economic fundamentals and diverging too much from one another. While the ECB has not signaled any intention to activate the new TPI scheme anytime soon, its creation sends a message to investors that the bank will keep market dynamics from disrupting its monetary policy transmission and that it is ready to aggressively intervene if spreads continue to widen out of control. In ECB President Christine Lagarde’s words, the bank is “capable of going big” on that.

- The ECB had initially indicated it would raise its main interest rate by only 25 basis points in July. But higher-than-expected annual inflation in the eurozone's 19 countries that reached a record 8.6% in June (up from 8.1% in May) prompted the bank to take a larger step toward policy normalization.

- The ECB is now expected to hike rates by another 50 basis points in September (which would bring its deposit rate to 0.5%) in the likely case that inflation either remains at current levels or increases further.

- In June, the ECB announced it would end its bond-buying program and raise interest rates out of negative territory the following month. Bond yields between Europe’s highly indebted countries (notably Italy, Spain, Greece and Portugal) and Germany (whose debt acts as a baseline because of its perceived safety) significantly widened in response to the announcement, reflecting market fears that weaker economies will struggle to cope with debt repayment as the bank tightens its monetary policy.

- The TPI is meant to prevent “fragmentation” in the eurozone, which occurs when the borrowing costs for some countries increase much more than others. The eurozone — in which 19 sovereign governments share one currency and one monetary authority (the ECB) while maintaining their own individual fiscal policy and bond markets — is particularly exposed to this risk, as markets perceive economic and political risks differently from country to country.

While the TPI is meant to calm market concerns over rising borrowing costs and sovereign debt levels in some eurozone countries, the ECB’s capacity to intervene when spreads increase due to political risk remains to be tested. The TPI’s task is to shrink spreads on bonds between the eurozone’s core and more vulnerable peripheral members without raising concerns of institutional overreach. The bank announced the scheme the same day as its interest rate hike in the hopes of avoiding a bond market panic, which would risk pushing up weaker countries’ borrowing costs to levels that tip them into a financial crisis. But this attempt to keep markets calm following the ECB’s unexpected 50-point hike has only partially succeeded. While they haven’t significantly widened, spreads between peripheral and core government bond yields remain high, which indicates investors remain unsure over the ECB’s ability to effectively intervene in the case of a debt crisis. This risk is particularly pronounced in Italy, where the recent collapse of former Prime Minister Mario Draghi’s government has paved the way for a far-right victory in early elections scheduled for September. By further denting investor confidence in the long-term sustainability of Italy’s debt, the political upheaval has led to a selloff in Italian bonds and stocks. According to the ECB announcement, the TPI can be activated to counter “unwarranted, disorderly market dynamics.” But it’s unclear whether widening spreads due to political risk (as is currently being seen in Italy) would be considered an “unwarranted”, as well as what mandate the bank would have to intervene in such instances and how it would do so.

- The price and yield of bonds are inversely related. Falling bond prices send yields higher which, in turn, increases the borrowing costs countries pay when they issue new debt. This sparks fears among investors over debt sustainability, further widening spreads in a self-fulfilling prophecy.

- Italy already paid the highest borrowing costs on its debt since the eurozone sovereign debt crisis. On June 30, Italy auctioned 2 billion euros worth of 10-year bonds and 4 billion euros worth of five-year bonds. The bonds were sold at yields of 3.47% and 2.74% respectively — the highest in almost a decade, although still well below the levels reached at the height of Europe’s debt crisis in 2011-2012.

- Following the ECB announcement on July 21, markets are still showing signs of uneasiness, particularly for Italian bonds. The spread between Italian and German 10-year yields has widened back to around 2.3%, close to the levels that had prompted the ECB to call for the emergency meeting on June 15.

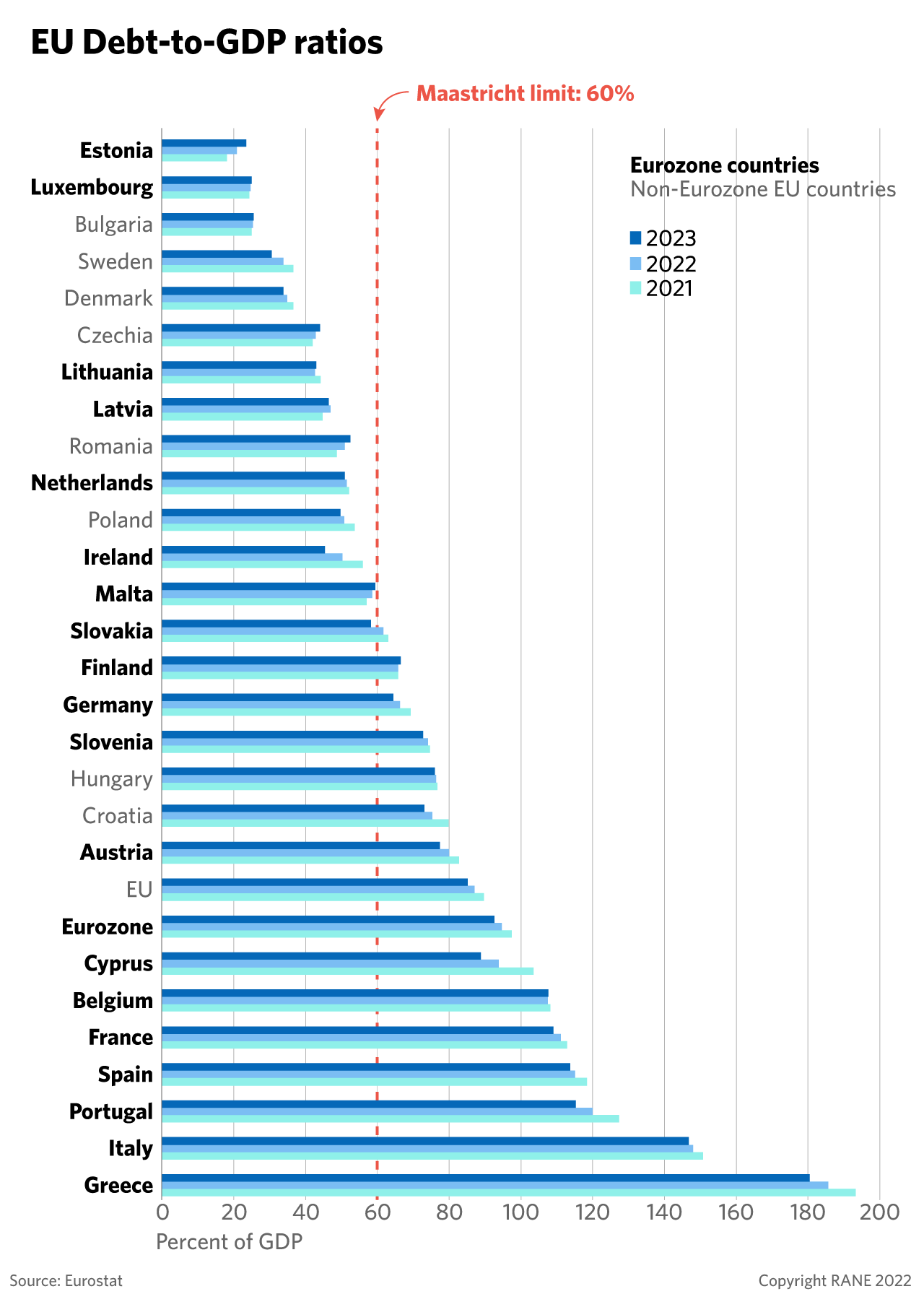

Despite persisting economic, political and legal constraints, the TPI should help keep the eurozone from entering another sovereign debt crisis, as the European Union is in an overall stronger economic and political position than it was when the bloc entered the 2010-12 debt crisis. Markets are currently worried about weaker countries’ capacity to service debts, but the economic fundamentals in highly indebted eurozone countries are more solid than they were during the debt crisis in the late 2000s and early 2010s. While higher than a decade ago, debt-to-GDP ratios are still trending downward for most countries in the currency area — thanks to still-low borrowing costs, continued economic growth and rising inflation. Inflation, at least in the short term, makes national debt levels look more manageable because they are measured against nominal GDP (which is higher when prices rise); government deficits also tend to decrease in an inflationary environment, as tax revenues grow faster than public expenditure. Moreover, the European Union’s 750 billion euro COVID-19 recovery fund is expected to sustain modest growth rates for the next few years, although the ongoing war in Ukraine presents serious downside risks that could still tip the euro area into a temporary recession (particularly with a worsening of the energy crunch brought on by further disruptions to Russian gas). All taken together, the difference between the interest paid on debt and nominal GDP growth is set to remain favorable over the next few years, while debt servicing costs are expected to rise only very gradually alongside interest rates — partly because of the lengthening of the maturity of sovereign debts in the last decade. Moreover, unlike the 2008 debt crisis (which was largely the result of internal economic mismanagement among eurozone countries), Europe’s current economic instability is being driven by external shocks (including the Ukraine crisis and residual fallout from the ongoing COVID-19 pandemic) that have so far been leading to increased solidarity at the EU level. While northern countries like Germany, Austria, and the Netherlands fear the ECB may overstep its mandate to keep yields low for highly indebted southern countries and encourage fiscal profligacy, there seems to be sufficient political alignment within the bloc on the need to prevent a new financial crisis. TPI’s implementation will also be facilitated by much looser fiscal conditionality compared with the ECB’s earlier asset-purchase program, the Outright Monetary Transactions (OMT), which will significantly reduce the political costs for beneficiary countries.

- The difference between interest and GDP growth rates is key to assessing public debt sustainability. When the interest rate is higher than the growth rate, a government must maintain a budget surplus to prevent the country’s debt-to-GDP ratio from rising.

- The new TPI scheme is attached with conditions designed to prevent it from becoming “monetary financing” (the “printing” of money by a central bank to bolster a country’s budget, which would violate EU treaties). But this conditionality is light. The TPI has only four, loose criteria: compliance with the EU fiscal framework; no severe macroeconomic imbalances; sustainable public finances; and “sound and sustainable” macroeconomic policies.

Highly indebted eurozone countries are not in immediate danger of a financial crisis thanks to long debt maturities at very low interest rates. But rising political risk could eventually trigger one. Greece and Portugal — which are among the so-called PIIGS countries with the highest debt levels in the eurozone, which also includes Ireland, Italy and Spain — should be able to cope with higher yields, as the relatively high economic growth both countries are enjoying has left them in a comfortable fiscal position. Most of Greece’s public debt is held by official creditors who have granted the country very favorable conditions at very low rates and maturities above 18 years. Most of Spain’s and Italy’s debt, by contrast, is financed at very low interest rates; the lengthening of debt average maturity — at above eight and seven years, respectively — largely shields the two countries from an abrupt rise in interest payments as well. Based on estimates compiled by the International Monetary Fund, the debt-to-GDP ratios in debt-laden PIIGS countries should continue to fall over the next five years, as long as spreads are kept in check. However, concerns remain over Italy and France, where the political situation is unstable. What worries investors the most in the short term is Italy, where a nationalist and mildly eurosceptic coalition of right-wing parties is positioned to win the early election in September. While Italy currently matches all criteria for the TPI’s activation if spreads continue to widen, markets fear that a new government could abandon the existing fiscal consolidation efforts and put Italy’s debt on an unsustainable path. In the medium term, however, France may also see investors growing increasingly nervous over its growing debt-to-GDP ratio (which has almost doubled in the past decade) amid the country’s worsening political environment. French President Emmanual Macron’s party recently lost its majority in the National Assembly, where opposition parties are now eager to demand concessions in exchange for political support, increasing pressure on public finances. While France is in less imminent danger of entering a financial crisis compared with Italy, debt sustainability concerns could emerge if legislative pushback impedes the Macron administration’s ability to implement key structural reforms aimed at reducing budget deficits and boosting economic growth.

- Whoever is elected to lead Italy’s next government will likely maintain the bulk of outgoing Prime Minister Draghi’s economic reforms, which still need to be implemented as part of the country’s EU-funded recovery plan (the completion of such reforms is also one of the conditions for TPI eligibility). Until a new executive is in place, however, markets will remain volatile. It’s thus possible that TPI purchases of Italian sovereign debt may start even before the country’s election on Sept. 25, should spreads widen further.

The ECB’s laser focus on fighting inflation will come at the expense of short-term economic growth, which will leave eurozone governments with less room to implement fiscally expansive policies amid higher borrowing costs. The TPI will only address “unjustified” market dynamics triggered by the overall tightening of monetary policy. Bond yields will thus remain above pre-pandemic levels for most eurozone countries, as will interest payments for governments, companies and households. This will ease inflationary pressures by dampening consumer spending and business investment. But it’ll come at the cost of hurting short-term economic growth. Even a very strong central bank intervention would still leave reduced fiscal space for fragile eurozone countries, as borrowing costs will remain higher than in the past. The currency area’s more fragile countries (such as Italy) will, in turn, have to ensure their debt-to-GDP ratios remain on a downward path through deficit reduction, which will largely hinge on their government’s ability (and willingness) to effectively use EU recovery funds and impose unpopular austerity measures if needed. This means that while the risk of new financial crises emerging in the eurozone is currently low, it cannot be ruled out — especially in countries with high political risk or populist governments that insist on expansive fiscal policies regardless of the worsening economic climate.

- TPI will aim to remove some of the speculative volatility in bond spreads to bring them back to the market's view on fundamentals. But it will not actively seek to lower yields across the eurozone, as this would go against the ECB’s overall monetary policy direction.

- The ECB’s statement says that “the scale of TPI purchases depends on the severity of the risks facing policy transmission,” which means the bank will go as far as it deems necessary with its application.

- While an economic recession for the eurozone is an increasingly likely possibility, the ECB is operating on its base case forecast, which sees output slowing down but still growing. In July, the European Commission cut its forecast for GDP growth in the euro area to 2.6% for 2022 and 1.4% in 2023.