A man wearing a surgical mask walks in an empty square in front of a cathedral in Locri, Italy, on April 7, 2020. As of April 10, Italy had reported 143,626 COVID-19 cases with 28,470 deaths.

For many governments in Southern Europe, containing the COVID-19 contagion in the coming weeks may prove to be the easy part. After the immediate health crisis subsides in the region, much bigger economic and political troubles will quickly follow in the second half of the year. Countries including France, Italy, Spain, Greece and Portugal will experience deep recessions and severe fiscal problems, which in some cases will be made worse by the return of political instability and the strengthening of nationalist opposition parties.

Deep Recessions

Most, if not all, countries in Southern Europe will be in a recession this year because of the quarantine measures implemented to contain COVID-19. Many economies in the region were already slowing down before the pandemic. In the fourth quarter of 2019, France’s economy contracted by 0.1 percent, Italy’s by 0.3 percent and Greece’s by 0.7 percent. Countries such as Spain (+0.5 percent) and Portugal (+0.7 percent) saw some growth, but it was weak.

The data for the first quarter of 2020 will be negative, but the data for the second quarter will be worse. Southern European countries introduced their toughest quarantine measures in March, which means that normal economic activity in January and February will somewhat mitigate the impact of the COVID-19 in the first quarter. But with the quarantine measures in full force in April, and a progressive lifting of the measures potentially starting in May, the second quarter will probably show deeper GDP contractions in Southern Europe.

It is impossible to know the exact duration and depth of the recessions since they will depend on the evolution of contagions and the progressive lifting of the lockdowns. But because many companies have gone out of business during the quarantine, and hundreds of thousands of workers have lost their jobs, production, consumption and investment will probably remain weak in the third and potentially even the fourth quarter of 2020.

Higher Unemployment

Unemployment rates fell steadily in Southern Europe since the peak of the financial crisis in the early 2010s. In early 2020, unemployment was below 10 percent in Portugal, France and Italy, and around 14 percent in Spain and 16 percent in Greece. But these rates will increase significantly in the coming months because many of the workers who lost their jobs or were suspended during the quarantine will not find immediate employment once the outbreak is over.

The quarantine measures are destroying millions of jobs in Europe. In Spain, almost 900,000 jobs (in a labor force of roughly 23 million) were lost between layoffs and suspensions in the second half of March alone. In France, nearly four million workers (in a labor force of around 30 million) were on state-subsidized furloughs at the beginning of April. In Portugal, by late March, companies had asked for state permission to dismiss more than 500,000 workers (in a labor force of less than 6 million). Unemployment benefits and state subsidies are not a full substitute for salary, which reduces the affected workers’ ability to consume and further weakens the economy.

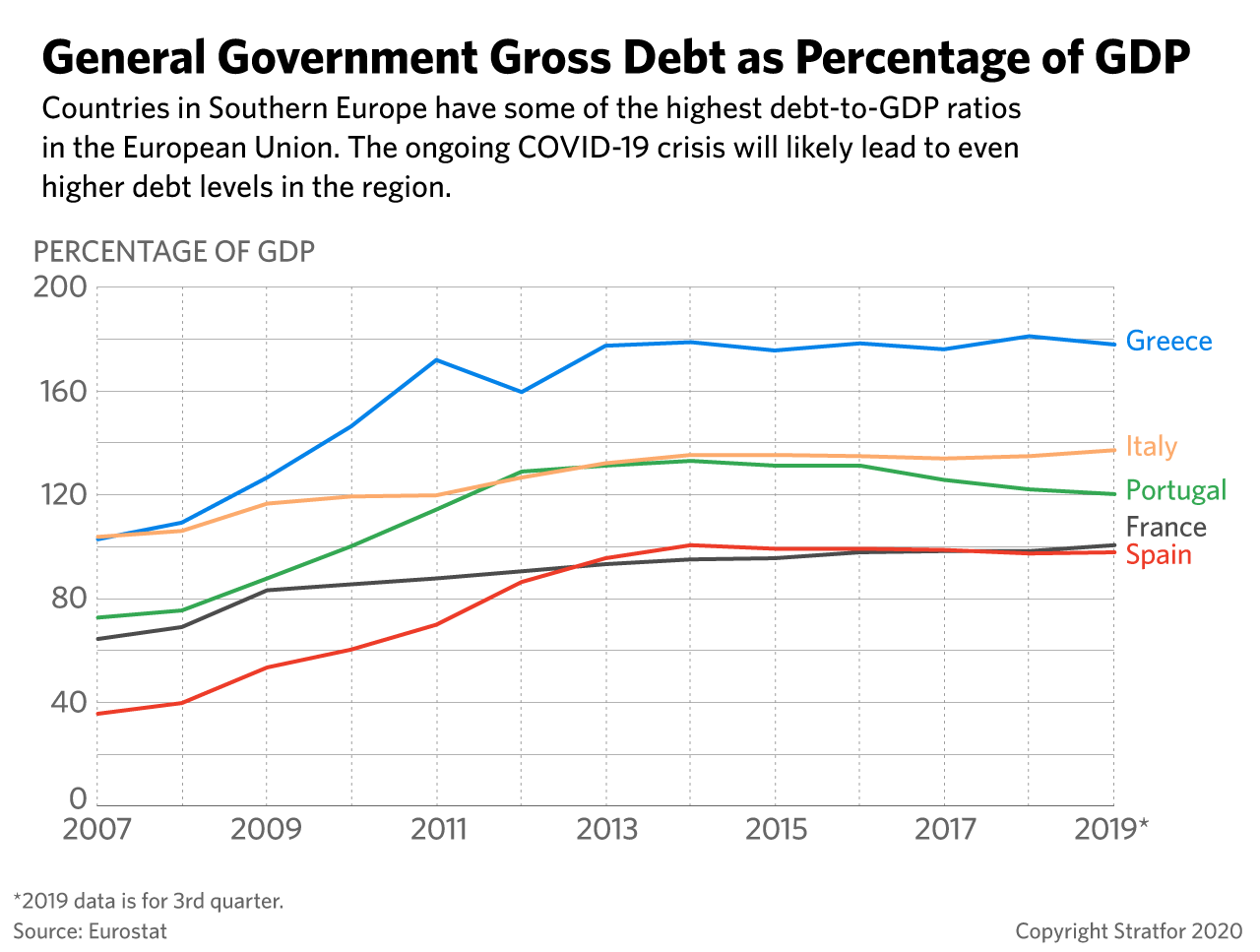

Higher Deficit and Debt Levels

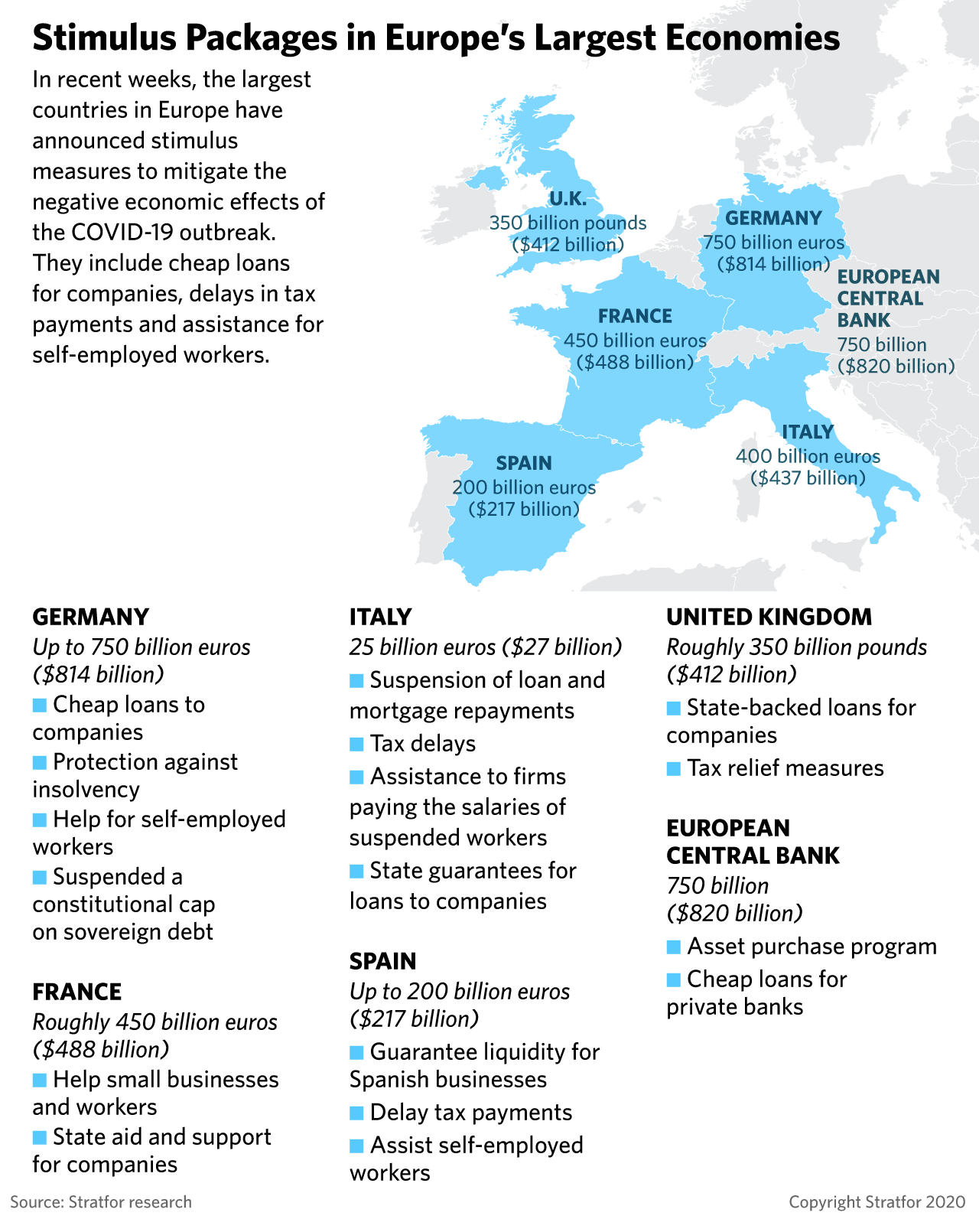

In recent weeks, national governments have pumped massive amounts of money into the economy in the shape of state-backed loans for companies, delays in tax payments for households, and assistance for workers who lost their jobs. A big part of these measures will be funded by taking on additional debt. So far, Southern European governments have been able to take on new debt at low-interest rates, partially because of the intervention of the European Central Bank in debt markets. But when the COVID-19 contagion is over, these countries will find themselves with higher debt levels amid deep recessions.

Italian business lobby Confindustria recently calculated that the country's debt could reach 147.2 percent of GDP in 2020 from 134.8 percent in 2019. Goldman Sachs, meanwhile, said that Italy's debt could reach as much as 160 percent of GDP this year. According to the Swiss financial services firm Credit Suisse, Spain’s sovereign debt will reach 105.3 percent of GDP in 2020 from 94.4 percent in 2019. And the Italian bank Unicredit said Portugal’s debt could reach 145.7 percent from 117.6 percent a year ago.

The main question that markets will try to answer after the COVID-19 pandemic is over is whether these levels of debt are sustainable. One of the places where they will look for answers is fiscal deficits, and the situation will not be reassuring. Before the current health crisis, some countries in Southern Europe were struggling to take their deficits below the EU-mandated threshold of 3 percent of GDP. But the broad trajectory was still toward compliance with the bloc’s requests. However, the massive stimulus packages in Southern Europe will lead to deficits that, depending on the calculation, could be between 5 and 10 percent of GDP in 2020 (some analysts suggest they could be even higher).

Credit rating agencies could react to these debt and deficit levels by downgrading the countries in trouble. This would make it more expensive for governments to borrow and, in countries such as Italy, would bring debt dangerously close to “junk” status, which means that many investors would not be able to purchase Italian debt because of their internal rules against the purchase of risky assets. A degradation in the quality of bonds would also have a negative impact on the assets portfolio of the banks that hold them — a problem that is particularly acute in Italy, where banks hold billions of euros in debt from the national government.

A heavier debt burden, combined with higher borrowing costs, would also constraint the Southern European government’s room to spend domestically because a significant part of public revenue would have to be used to service the debt. Over time, national governments may have to introduce spending cuts and tax hikes to increase state revenue and reduce their deficit, limiting their ability to emerge from the recession.

The economic crisis will also create problems for banks holding private debt. In recent years, banks in Southern Europe have been reducing their exposure to non-performing loans at a fast pace. But the risk of households and companies defaulting on their loans will increase hand-in-hand with the rise in unemployment and the contraction of economic activity. The four EU member states with the highest ratio of non-performing loans are all southern: Greece, Cyprus, Portugal and Italy. These are the places to look at for banks potentially failing because of the economic downturn.

Another Nationalist Wave?

The COVID-19 crisis brought temporary political stability to several countries in Europe. Politicians across the Continent have put their ideological differences aside to back emergency measures, increasing the popularity of many governments. But when the worst part of the health crisis is over, pre-existing political disputes will return. And governments that were either fragile (such as Italy’s) or unpopular (such as France’s) will see their old problems come back. Once the emergency passes, the blame game will begin as opposition parties focus their criticism on the things that the governments should have done differently. Nationalist and Euroskeptic parties in the south will attack countries in the north for their lack of solidarity, and will criticize the European Union for its slow reaction to the crisis.

The austerity measures could further complicate the political situation. During the financial crisis of the early 2010s, most of the governments that implemented unpopular spending cuts were punished by voters in the next election. The crisis also contributed to the emergence of anti-establishment parties, some of which had anti-immigration and anti-EU positions. So far, nationalist parties such as Italy’s League and France’s National Rally have struggled to take advantage of the coronavirus pandemic. But these kinds of parties thrive in times of recession, which means that the door will be open for existing or new parties to emerge as a result of the new economic crisis that is just now beginning Europe.