A 3D illustration of COVID-19. The global economy is now expected to experience significantly lower growth in 2020 as more consumers and businesses adjust to a quarantined world.

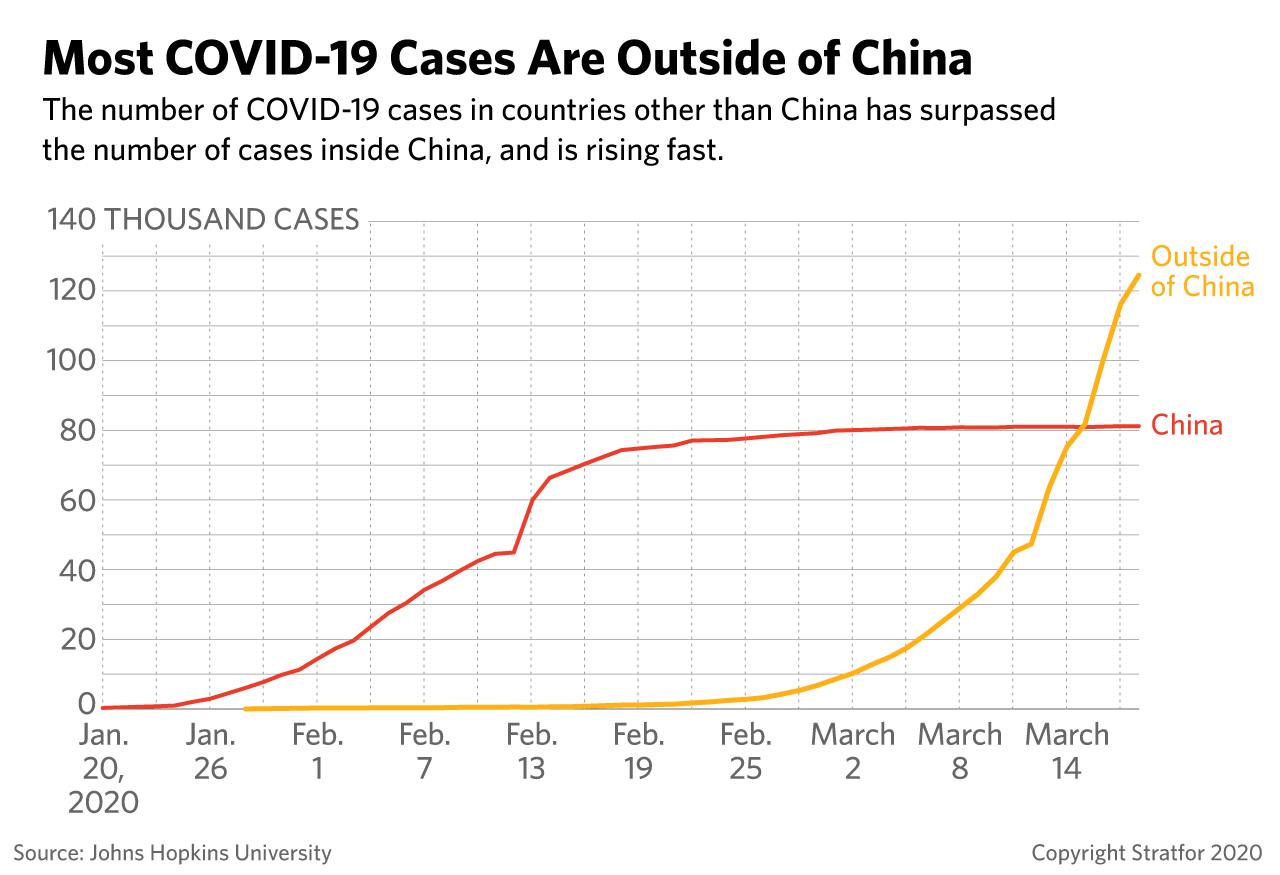

As the COVID-19 outbreak continues to spread to more countries in more corners of the world, initial forecasts that the total economic damage would be mostly contained to China are no longer plausible. Consensus estimates now suggest a 5-10 percent drop in global gross domestic product (GDP) in the quarter in which country-wide epidemics begin, persisting at an as-yet-undetermined magnitude into the next quarter as consumers and businesses adjust to the impact. The still many unknowns that surround the pandemic, however, has made it difficult to forecast the full economic fallout. China’s recovery may thus provide a better benchmark for what will happen elsewhere, given its status as the initial epicenter. But few other countries will be willing or able to take actions as draconian as Beijing's to quickly and efficiently contain the virus — and the subsequent economic hits.

The Outlook Darkens

Early COVID-19 economic forecasts made in January and February, back when the virus was primarily contained in China, were based on the 2003 SARS epidemic and the 2009 H1N1 outbreak. They projected a one-quarter hit on China’s gross domestic product (GDP) growth, and a loss of only about 0.1 percent off world GDP forecasts. But as COVID-19 continues to spread to more countries outside China, large-scale simulations have been conducted to more accurately assess the pandemic’s worldwide economic impact.

Models based on the 1968-1969 flu epidemic in Hong Kong — which had a case-fatality ratio of 0.5 percent and killed one million people worldwide — have estimated total losses from the COVID-19 pandemic at about $2.3-2.7 trillion in a $90 trillion world economy. Based on a 1918 Spanish Influenza-like pandemic, a more extreme projection generated by the Australian National University put economic losses at more than $9 trillion, or 10 percent of nominal global output.

At the core of the fallout is the pandemic's impact on consumer demand for goods and services, which is the primary driver for economic growth in much of the world. In the United States, for example, domestic consumption makes up 70 percent of GDP. But amid the COVID-19 pandemic, even healthy people may choose to limit spending because of employment fears or social distancing behavior. And as a result, consumer spending (other than online shopping) will fall further as more countries reckon with widespread outbreaks.

The pandemic will also affect corporate profits, causing businesses around the world to cut back further on already anemic investment. This will affect equity and corporate ability to repay record amounts of debt as well. Primary credit markets are essentially frozen as well, meaning some companies will not be able to rollover liabilities without increasing their refinancing costs. Countries with less favorable debt dynamics such as Italy, meanwhile, will be forced to pay more for increased fiscal spending and will, in turn, face greater risks of default.

The new oil price war between Saudi Arabia and Russia could be helpful to net oil importers, such as China, Europe and Japan. But the total effect is still indeterminate, as price declines will eventually be offset by fewer barrels a day being imported. Additionally, oil price declines plus a lack of wage increases in many countries given falling demand for labor raise the risk for negative inflation (or deflation).

Regional Impacts

As with global patterns, the regional and country-specific economic impacts of COVID-19 — and the fiscal policies being put in place to help curb those impacts — remain fluid.

China

While aggregate economic data won’t be reported until mid-April, a year-over-year contraction in China’s GDP in the first quarter of 2020 is almost certain at this point. China, which accounted for one-third of 2019 global growth, began experiencing diminished growth at the beginning of the year when COVID-19 first began spreading in the country. Between January and February, the country's industrial output fell by 13.5 percent, retail sales fell by 20 percent, investments in buildings and machinery dropped by 24.5 percent, and the unemployment rate jumped to a record high of 6.2 percent But now, the country is also grappling with plummeting foreign demand, as the virus continues to spread internationally.

There is evidence that China's epidemic is slowing and that country is now getting back to work, with estimates that 80-85 percent of business activity has resumed. These estimates, however, are not fully supported by secondary data, such as traffic congestion. And longstanding concerns regarding the accuracy of Chinese reporting will color any government-issued assessment.

Beijing also recently announced tax cuts and new investments totaling about 6 percent of GDP to help boost its economy, but the government’s 6 percent growth target for 2020 may still be out of reach without further stimulus. Beijing's stimulus policies may temporarily increase domestic demand temporarily, but they contribute to long-term structural problems, including the continued build-up of unsustainable domestic debt, which could become a drag on future growth.

The United States

There is now a broad consensus that the United States is now on the brink of a recession (in at least the short-term),(or is already in one) with first-quarter growth near zero followed by an expected decline in second-quarter growth amid supply crunches in manufacturing, near-panic in financial markets, and the continued collapse of travel and leisure activities.

- The New York Federal reserve's latest Empire Manufacturing survey showed the report's index of business conditions was down a record 34.4 points in March, which usually implies a recession is underway.

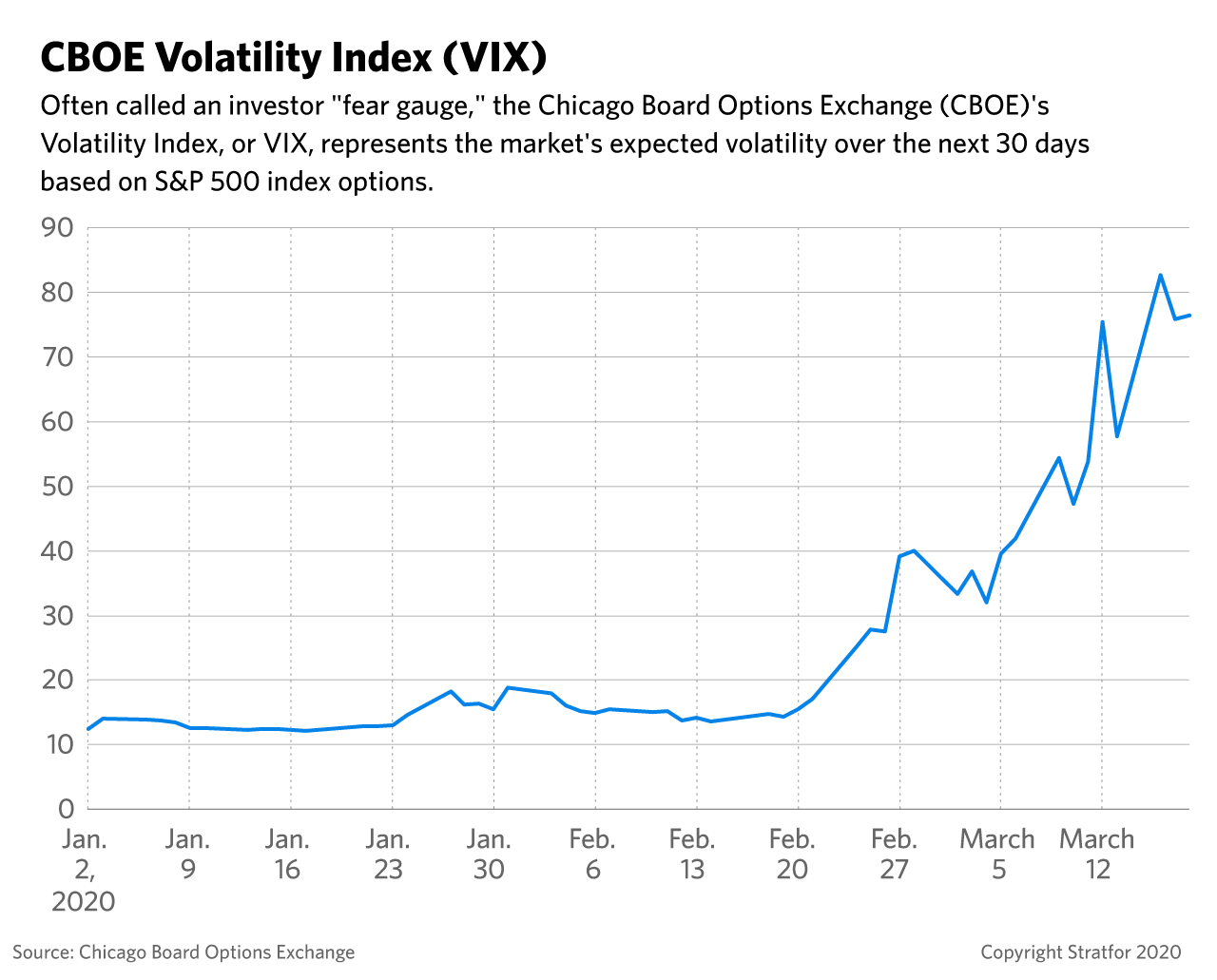

- The Chicago Board Options Exchange Volatility Index, known as a fear gauge, has also so far risen more than sixfold this year.

- On March 19, the U.S. Labor Department reported initial jobless claims were up by 70,000 to 281,000 compared with the previous week, and private forecasters expect that number to jump by at least two million in the next report on March 26.

For now, however, most forecasts are being downgraded only to 1.2-1.5 percent of aggregate growth for all of 2020. But it is still unknown how long consumers will pull back (after a surge of precautionary "buying binges" among American consumers in early March), especially as quarantine measures force businesses across the country to either close or operate at reduced levels. Business earnings declines are, in turn, driving layoffs and weighing heavily on consumer sentiment.

The nature of U.S. politics takes time to yield decisions on fiscal policy, leading to inevitable lags in implementation. In a best-case scenario, U.S. economic activity would pick up at the end of the second quarter just as fiscal and monetary stimulus measures start to kick-in. But this economic turbo-charge could also possibly lead to inflation down the line.

Europe

With France, Italy, and Spain in nearly total lockdown for the foreseeable future, the hit to Europe's economic growth will be massive, even if unquantifiable.

- The European Commission already estimates that GDP will fall by 2.5 percentage points from an increase of about 1.5 percent in 2019.

- The German ZEW Economic Sentiment for March dropped a staggering 58 points — the largest fall in the indicator's nearly 30-year history.

- The president of the European Central Bank (ECB) reportedly told European leaders that a one-month shutdown of EU economies to contain the virus would reduce euro area growth by two percentage points from the ECB’s initial forecast of 0.8 percent growth for 2020, and that a three-month lockdown would drop output by 5 percentage points.

- For the United Kingdom, Brexit-related uncertainty was already estimated to reduce the country's potential output by half this year. But the still-unrealized impact of leaving the European Union's common market will now be further augmented by coronavirus-related drops in consumption and investment.

The Middle East and North Africa

Lower oil prices, combined with depressed tourism and domestic consumption rates due to COVID-19, will take a toll on every economy in the Middle East and North Africa. The recent breakup of the OPEC+ alliance could also make the impact outlast the outbreak itself.

- COVID-19 will accelerate the pace of economic collapse in countries like Lebanon and Iraq with existing financial and debt crises. Lebanon, in particular, will be forced to consider an International Monetary Fund loan to deal with its massive debt issues.

- The pandemic will risk sending the region's major economies, such as Egypt and Turkey, into recessions by dampening consumption, tourism and industrial sector demand. Turkey alone could see its GDP by more than 15 percent by June, adding more pressure to the lira, the country's national currency, and concerns about corporate debt.

- The uncertain recovery period from the regional COVID-19 outbreak will also collide with a period of low oil prices. This will slow the pace of economic reform and diversification in energy-dependent economies in the Arab Gulf states. Saudi Arabia, Bahrain and Oman, in particular, will likely be forced to draw down financial reserves, take out more debt and delay capital investments.

What Can Governments Do?

To mitigate the economic blow of the COVID-19 pandemic, central banks around the world — including the U.S. Federal Reserve and the European Central Bank — are reorienting their strategies away from cheaper credit through interest rate effects. These efforts are intended to provide liquidity as coronavirus-induced flights to cash result in market droughts. Doing so could help ease pressure on corporate balance sheets amid declining profitability from sales and revenue.

But changes to national fiscal policies are more important in the short-term to offset falling demand and losses of income. Some countries are offering lending and credit guarantees for businesses along with temporary tax relief for households. Looming possible layoffs will lead to requirements for aggressive fiscal measures, such as payments to consumers, even if those temporarily increase government deficits by massive amounts. But the duration and impact of such fiscal policies on global consumer behavior are difficult to gauge, especially if precautionary savings increase. It's also unclear how long supply chain disruptions will continue.

What to Watch For

In assessing the overall economic impact of the COVID-19 pandemic, there are several key factors that complicate current economic forecasting for COVID-19:

- Real-time hard data often lags in such global events, creating a retrospective snapshot of previous conditions.

- Stock markets are a guide to investor expectations of corporate earnings, but daily fluctuations in the market reflect fears, which make short-term movements an unreliable indicator of the overall economic outlook. Long-term trends are thus often a more accurate gauge, with the S&P 500 moving down by an average of about 25 percent since mid-February.

- Sentiment indicators for businesses and consumers are more current and forward-looking, but are still published only monthly.

In addition to economic forecasts, there are several other key dynamics and developments to track over the next few months in order to better gauge how COVID-19 will shape global outcomes. These include, but are not limited to:

- The spread of the virus across the United States and the degree to which it precipitates more draconian containment strategies, as well as the time it takes to bring the U.S. outbreaks under control.

- Whether the virus continues into the summer, as many baseline economic forecasts presume the pandemic is seasonal and follows the epidemiological pattern observed in China, in which it accelerates and peaks over a two-month period before receding.

- More widespread outbreaks in countries in South Asia, Latin America and Africa, where health care systems are already significantly constrained.

- The speed and scope of global government policy responses to support household and business incomes, and of central banks to limit financial disruptions.

- The speed of recovery in China, as a leading indicator of how quickly economies can get back to normal, though China’s export-oriented economy will struggle as demand in the rest of the world continues to decline.

In the longer term, there are and will continue to be long-lasting, albeit indeterminate, retrenchments in consumption and investment. Moreover, global financial conditions have tightened dramatically as assets are repriced downward, and as flights to safe havens and liquidity result in selloffs in equity and credit markets. Those could lead to wider layoffs beyond the immediate ones as companies are unable to meet liabilities, increasing even wider layoffs that could accelerate into a deeper, longer-lasting economic contraction.