A very strong U.S. dollar will increase the risk of renewed trade tensions between Washington and its main trade partners, and will likely also intensify protectionist rhetoric in the United States ahead of the 2024 presidential election. A confluence of factors — including Europe's dire economic outlook, the U.S. Federal Reserve's relatively aggressive interest rate hikes, and continued monetary accommodation in Japan — have increased the dollar's value relative to other major currencies like the euro, the British pound and the Japanese yen. In trade-weighted terms, the U.S. currency remains just below its March 2020 peak, when the COVID-19 pandemic and safe haven flows sent the dollar soaring.

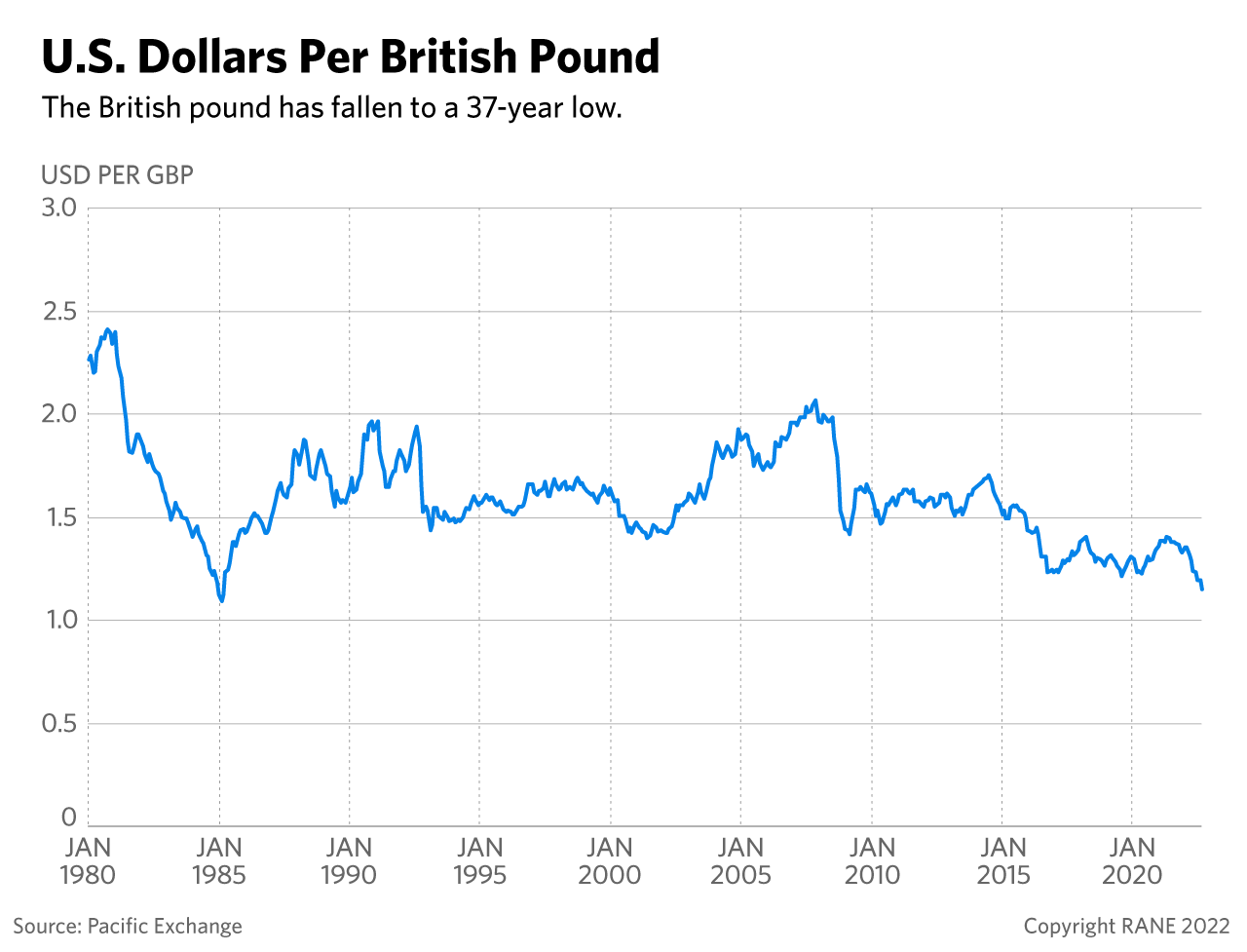

- The dollar has reached a 20-year high against the euro, a 24-year high against the yen and a 37-year high against the pound sterling. The U.S. currency is also up against most emerging markets currencies.

- The trade-weighted dollar (the average value of the dollar against all currencies weighted by U.S. trade) is near multi-decade highs as well.

- The U.S. dollar is also trading at two-year highs against the Chinese renminbi.

In the coming months, multiple political and economic developments in Europe, the United Kingdom, Japan and emerging markets suggest that the U.S. dollar will remain strong and may further strengthen.

- The economic outlook for Europe will remain uncertain in light of the Ukraine war, the energy supply disruptions and an impending recession. A recession in the eurozone could quickly renew investor concerns about sovereign risk and financial stability in countries that use the common currency, especially those that already have high levels of sovereign debt and deep fiscal deficits. If the eurozone enters a particularly deep recession, it might even rekindle concerns about the sustainability of the single currency.

- The United Kingdom will also continue to struggle with high energy and food prices, increasing government debt and, crucially, a widening account deficit. Increased public spending on measures aimed at mitigating the social fallout from the country's cost of living crisis, along with continued concerns about the future of EU-U.K. trade relations under the United Kingdom's newly elected Prime Minister Liz Truss, will add to the downward pressure on the pound sterling.

- In Japan, meanwhile, global inflationary pressures have so far had only a subdued impact on consumer prices compared with other major economies. This — combined with ongoing concerns about deflation — will likely see the Bank of Japan stick with its ultra-loose monetary policy, which will contribute to a further widening of U.S.-Japanese interest rate differentials. Currently, markets are forecasting the U.S. Fed's federal funds rate to peak at 3.8% in March 2023. However, if the United States continues to release solid economic data, those forecasts may be revised upwards, which would put even more downward pressure on the zero-yielding yen vis-a-vis the U.S. dollar.

- The risk of a global economic slowdown and recession, falling commodity prices, and, especially, a stronger U.S. dollar and higher U.S. interest rates will also continue to put pressure on emerging markets. Uncertainty about the present and future course of economic policy in some of those markets, such as Brazil and Turkey, will further weigh on their currencies as well.

In the United States, a continued strong dollar may increase calls for protectionist trade measures, especially regarding China. The administration of U.S. President Joe Biden has not reversed its predecessor's tariffs on Chinese imports, though it has adopted a more cooperative trade policy vis-a-vis Washington's allies. Thanks to the sharp post-COVID surge in domestic demand, American companies and workers are enjoying solid earnings and a historically tight labor market, respectively, which is currently dampening the political appeal of protectionist measures. But while trade policy has largely been a non-issue in the run-up to the U.S. November midterm elections, this will likely change ahead of the 2024 presidential race if the U.S. dollar continues to strengthen and the U.S. economy enters a recession.

- As the United States heads toward or dips into a recession, unemployment levels will increase and corporate earnings will weaken. Within this context, export-oriented U.S. companies will start complaining more vociferously about a strong U.S. dollar eating further into their profit lines. The United States' bilateral trade deficits will start garnering greater domestic political attention as well.

- This could see increased calls for more protectionist policies in the United States as early as next year, when presidential hopefuls begin vying for their party's nomination in the 2024 election. Should the United States' economic situation weaken, candidates will probably focus their campaigns on placing American workers and businessowners ''first'' by reducing the strong dollar and bilateral trade deficits (no matter how large or small).

- This shift may not lead the Biden administration to take protectionist measures, but it will increase the risk of a return to more protectionist U.S. trade policies after the 2024 elections. As demonstrated during the years under former U.S. President Donald Trump, such policies might primarily target China, but they could easily have major repercussions for U.S. trade vis-a-vis its allies in Europe and East Asia as well.