On Jan. 1, 2025, Russian natural gas flows to Europe through Ukraine came to a halt as the five-year transit agreement between Moscow and Kyiv expired without renewal. For over 40 years, this route served as a critical artery for Europe's natural gas supply, a vital revenue source for Ukraine, and a key instrument of Russia's strategic influence on Europe.

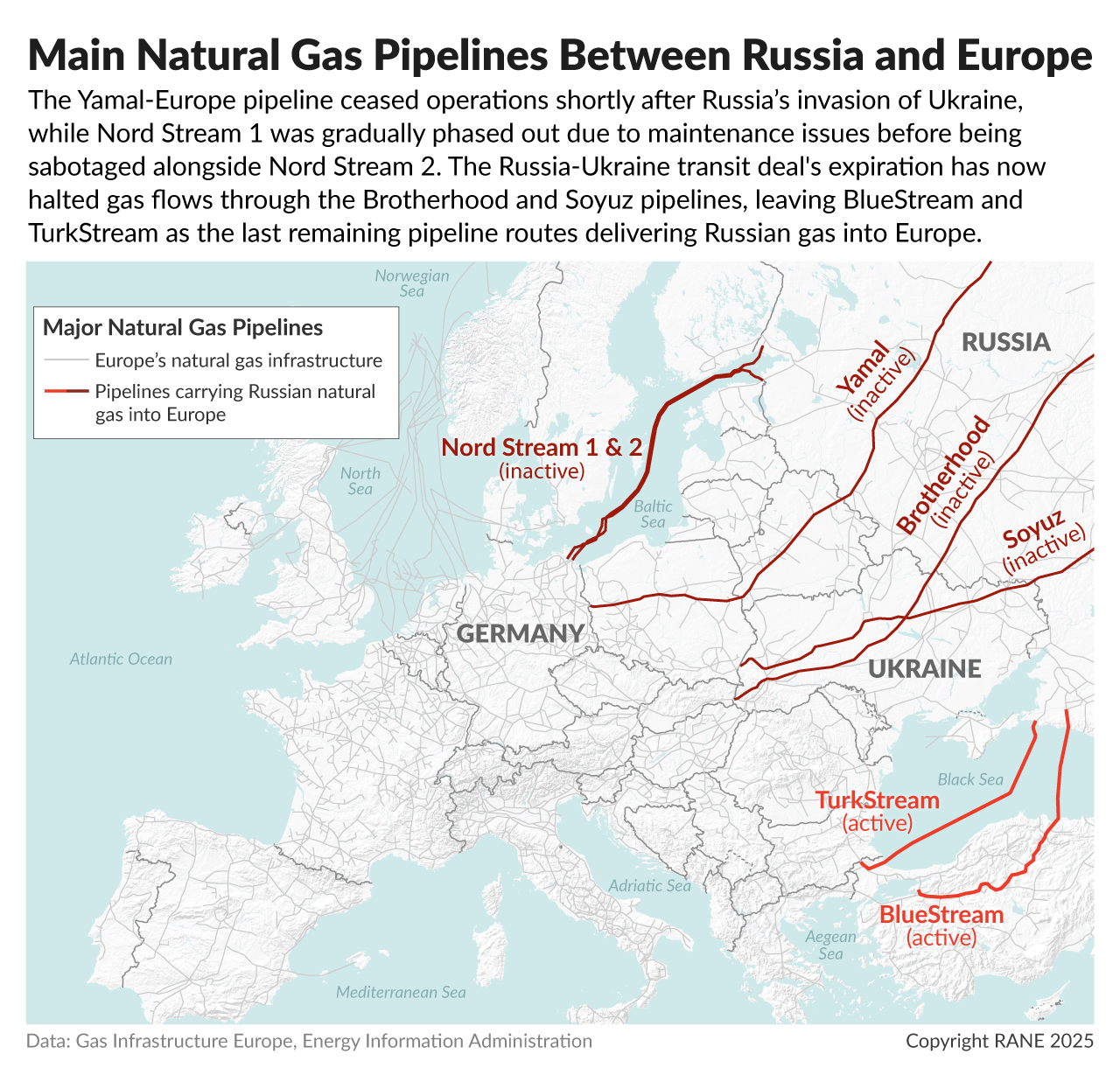

The end of the transit agreement — nearly three years into Russia's full-scale invasion of Ukraine and successive supply cut-offs — has left the TurkStream and BlueStream via Turkey and the Black Sea as the only remaining operational pipelines carrying Russian gas into the European Union. This underscores Europe's ongoing efforts to sever its reliance on Russian resources. It also marks the symbolic culmination of a historic shift in Europe's energy landscape, with far-reaching implications for energy markets and geopolitics in the region and beyond.

However, as Europe grapples with structurally higher energy costs and economic challenges, pragmatic considerations might prompt a partial resumption of Russian gas imports in the coming years — including and especially through Ukraine, perhaps as part of a peace deal — albeit under new terms that minimize strategic vulnerabilities and reflect the lessons learned from the past decade thanks to energy supply diversification efforts that will remove Moscow's ability to weaponize its gas exports to Europe.

How Did We Get Here?

The Russia-Ukraine gas transit route had long been a cornerstone of Europe's energy infrastructure, delivering Russian natural gas to European markets for over four decades through a set of pipelines running from Russia's western Siberian fields through Ukraine and into what is now Slovakia. Its origins trace back to the Soviet era, when the USSR began supplying gas to Europe in the late 1960s, initially to what was then Czechoslovakia, then Austria and later Germany. By the 1980s, gas exports had become a critical source of foreign currency for the Soviet Union and a key energy source for Europe, where demand for natural gas was growing and where energy supply diversification had become a strategic priority following the 1973 global oil crisis.

Following the Soviet Union's collapse in 1991, Russia inherited the bulk of its vast gas infrastructure, leveraging it both as an economic asset and a geopolitical tool. However, newly independent Ukraine's role as a transit hub introduced strategic challenges for Moscow, as it now had to negotiate fees with Kyiv, which held the ability to disrupt supplies or divert them for domestic use. During the rest of the 1990s, Russia thus sought to break its dependency on Ukraine by building new pipelines bypassing the former Soviet republic. This culminated in the 1996 completion of the Yamal-Europe pipeline, connecting Russian fields in the Yamal Peninsula and Western Siberia with Poland and Germany through Belarus, and a 1997 agreement with Turkey for the construction of the BlueStream pipeline (completed in 2003 and later joined by TurkStream in 2020), connecting Russia to Bulgaria via Turkey and the Black Sea. Nonetheless, by the mid-2000s, about 75% of Russian gas exports to Europe still passed through Ukraine.

In 2005, German companies signed a deal with Russian state-owned gas company Gazprom to build the Nord Stream 1 pipeline to transport gas from Russia's Vyborg fields near the Finnish border to northeast Germany via the Baltic Sea. This project sparked fierce criticism from Poland and other EU countries, which viewed Ukraine's transit role as essential to reducing Moscow's leverage over Kyiv, and viewed a new gas route directly into Germany as enhancing Russia's ability to exploit divisions within Europe. But from Germany's point of view, transit through Ukraine was a liability for its energy security, as underscored by the brief but impactful supply disruptions over pricing disputes between Kyiv and Moscow in January 2006 and January 2009.

In the 2010s, the U.S. shale gas boom enabled the United States to become a major exporter of liquefied natural gas (LNG), offering countries like Poland and the Baltic states an alternative to Russian gas. But for Germany — which had just embarked on its transition away from nuclear energy, which would significantly increase its gas demand for years to come — U.S. LNG remained unattractive due to the lack of import infrastructure and higher prices compared with Russian pipeline gas. Instead, Germany's then-Chancellor Angela Merkel doubled down on Russian gas, greenlighting the construction of a second Nord Stream pipeline in 2018, despite Russia's annexation of Crimea in 2014. However, U.S. sanctions in December 2019 on companies involved in the construction of Nord Stream 2, with just over 10% of the pipeline left to build, delayed the project's completion. The Russia-Ukraine gas transit agreement was thus renewed for another five years on Dec. 30, 2019, in a deal brokered by the European Union, Germany and France that sought to maintain transit revenues for Kyiv and ensure gas continued to flow into Europe ahead of the start of Nord Stream 2.

By the time the agreement came up for renewal at the end of 2024, however, Russia's 2022 full-scale invasion of Ukraine had reshaped Europe's geopolitical and energy landscape to a point where an extension was virtually impossible. In an address to the Bundestag on Feb. 27, 2022, German chancellor Olaf Scholz described Russia's invasion as a ''historic turning point'' for Germany, or Zeitenwende, and announced a departure from Berlin's decades-long rapprochement toward Moscow, including on energy by revoking Nord Stream 2's operating permits and announcing plans for the construction of several LNG import terminals. Meanwhile, the European Commission unveiled plans in May 2022 to phase out all fossil fuel imports from Russia by 2027. Although the Ukraine route briefly gained renewed importance following the sabotage of both Nord Stream pipelines in September 2022, this shift in Brussels, Berlin and many other European capitals set the stage for the eventual expiration of the transit agreement. In the lead-up to Dec. 31, 2024, Ukraine firmly opposed renewing the deal, and mediation efforts led by Azerbaijan's state-run energy company SOCAR to secure an alternative arrangement ultimately failed.

Shorter-Term Implications

The Jan. 1 halt of Russian gas flows via Ukraine has so far only caused limited short-term price volatility in Europe, as Gazprom's European customers had ample time to prepare for this scenario by diversifying suppliers and building up reserves. Still, while Europe is unlikely to face shortages this winter, the stoppage will increase price pressures in the coming months. The Ukrainian route accounted for approximately 5% of Europe's total gas intake in 2024 — insufficient to trigger a crisis, but significant enough to accelerate storage depletion in the middle of winter, when demand for heating is at its peak. This means European buyers, and especially those in central and eastern Europe, might have to pay a premium to outbid Asian competitors and secure adequate supplies ahead of next winter in an increasingly tight global LNG market. Though new LNG capacity is under construction worldwide, notably in the Middle East and the United States, meaningful additions are not expected to enter the market until 2026. This means European energy prices for 2025 will likely exceed last year's averages, prolonging higher energy bills for households and businesses.

In particular, landlocked central European countries heavily reliant on Russian pipeline supplies, like Slovakia, Austria and the Czech Republic, will face higher costs securing alternatives such as additional piped volumes from Norway and LNG imports via terminals and floating regasification units in nearby countries like Croatia, Greece, Germany, Italy, Lithuania and Poland. Financial impacts will be especially acute for Slovakia, which had become a key entry point of Russian gas into the European Union and was earning transit fees from sending gas to Austria, Hungary and Italy. The loss of transit revenues and access to discounted gas is expected to cost Slovakia an estimated 500 million euros each year. Other countries like Hungary and Serbia will continue to receive Russian flows through the remaining pipeline connections via Turkey and the Black Sea.

Ukraine will also forfeit significant transit fees, while giving up its long-standing strategic role as a key energy conduit for allies in Europe. Though it opposed renewing the agreement to deprive Russia of a key funding source for its war efforts, Kyiv was relying on the approximately $0.8-$1 billion in annual transit fees (around 0.5% of the country's GDP) to sustain its extensive pipeline network, which costs an estimated $400-$800 million annually just to maintain and is also used to transport domestically produced gas. The financial shortfall risks leaving Ukraine's pipeline infrastructure in disrepair, particularly as Russia is now more likely to increase its attacks on such infrastructure since Russian gas is no longer flowing through it. Additionally, any surplus transit income that could have been used to mitigate Ukraine's substantial annual budget deficits — estimated in the tens of billions of dollars — will now be lost, compounding the country's economic challenges as the war drags on.

Russia, for its part, will lose another piece of geopolitical leverage against Europe, as well as about $6.5 billion a year in revenue from gas sales from one of its three remaining operational pipelines to the Continent. The gas transported through this route has little to no alternative paths to market, as Russia has limited capacity to redirect these volumes to other pipelines or LNG export terminals. Meanwhile, efforts to reorient exports toward Asian markets will also face significant obstacles, being both slow and prohibitively expensive to execute while Russia' remains at war with Ukraine. Although Russia will prioritize boosting LNG export capacity to compensate for lost pipeline volumes, its ability to do so will be constrained by Western sanctions restricting access to vessels, financing and essential technologies for the development of a specialized fleet of LNG carriers. This means Russia is unlikely to fully offset losses of pipeline exports, despite expected growth in LNG exports over the coming years (including to Europe, which has already increased imports since the start of the war) — especially from the Yamal Peninsula. Meanwhile, Gazprom, already struggling financially after losing most of its European customers and reporting in 2023 its first net operating loss since 1999, will see its tax contributions to Russia's budget dwindle.

Longer-Term Implications

Alternative gas suppliers in and around Europe will provide only limited near-term relief to Europe's near-total cutoff of Russian pipeline supply. Norway, Europe's largest energy supplier since 2022, will largely focus on maintaining rather than increasing production levels through the late 2020s. Romania is set to become a net gas exporter with the large Neptun Deep offshore field scheduled to begin production in 2027, but its output will primarily serve local markets in southeastern Europe. The Eastern Mediterranean, with considerable newly discovered fields in recent years, might provide significant new exports, but likely not until the early 2030s. Similarly, North Africa faces political risks and infrastructure constraints that could delay investments to significantly scale up production and export capacity. The Caspian region, while a promising source of alternative pipeline suppliers like Azerbaijan and Turkmenistan, will require substantial investments and time to expand exports. Finally, Gulf states like Qatar and the United Arab Emirates have the greatest potential to increase LNG exports to Europe, but much of their focus will remain on Asia-Pacific markets. While some of the political, financial and infrastructural constraints in these geographies could be addressed within five to ten years, they offer limited solutions for Europe's most immediate energy challenges.

This leaves Australia and, especially, the United States — already the European Union's leading LNG supplier — as the most viable producers to replace lost Russian gas volumes. U.S. LNG export capacity is projected to rise from today's 13.8 billion cubic feet per day (bcf/d) to 17.8 bcf/d in 2025, reaching 24.2 bcf/d by 2028, with several new facilities coming online in the coming years. But while providing a lifeline to Europe as it decouples from Russian gas, this will not resolve the issue of structurally higher energy prices on the Continent, further eroding its global economic competitiveness. In fact, gas prices in Europe will decline as a glut of new LNG hits global markets from 2026, but they will likely not return to pre-crisis levels (before 2021) and will remain significantly higher than in the United States, largely due to the additional costs associated with LNG — including liquefaction, transportation and regasification — that do not apply to U.S. consumers relying on domestic pipeline gas. EU wholesale gas prices are thus expected to remain roughly double U.S. prices (a norm that predates the war in Ukraine), while the energy premium that benefitted Europe vis-a-vis Asian competitors in the past decades will evaporate, amplifying the cost gap for energy-intensive industries. Elevated gas prices will also directly impact electricity markets, where gas-fired power plants still often set the marginal price in Europe despite a gradual transition away from gas for power generation on the Continent. The transition from pipelines to LNG thus exposes Europe to greater market volatility, as a significant portion of this LNG will continue to be purchased on the spot market. This will translate to higher energy bills for industries and households that could hinder Europe's economic recovery and competitiveness.

Despite Europe's progress in its diversification plans, persistently higher energy prices may thus ultimately incentivize an at least partial resumption of energy trade with Russia in the coming years, depending on how the conflict in Ukraine ends. Unanimity requirements within the European Union for energy sanctions means a complete decoupling from Russian gas remains unlikely, despite the 2027 RePowerEU target, given the lack of consensus among member states for a total embargo. Over the next few years, the existing pipeline infrastructure could make historically cheaper Russian gas supplies attractive once again if high energy costs continue to strain competitiveness. Alongside continued LNG imports, the reopening of Nord Stream cannot be ruled out (unless the United States decides to extend and/or expand sanctions on the pipelines), while a resumption of flows via the Yamal pipeline looks less likely amid political opposition from Poland. As for Russian gas flows through Ukraine, a potential peace agreement in the next few years could include provisions for restoring gas transit, providing Kyiv with much-needed transit fees for economic recovery and reconstruction — assuming Ukraine's pipeline infrastructure survives the war intact. A potential deterioration in Transatlantic ties under the incoming administration of U.S. President-elect Donald Trump, which is less concerned with European priorities, could further increase this likelihood.

Lessons Learned?

The halt of Russian gas flows via Ukraine on Jan. 1, 2025, marked a highly symbolic moment in the ongoing transformation process of Europe's energy landscape. While the immediate impact of the cut-off has been limited, the longer-term implications of this broader transformation are profound. Over the past three years, Europe has demonstrated its capacity to secure energy without Moscow, but at the cost of increased market volatility and structurally higher energy prices. Because of this, the end of the Russia-Ukraine transit agreement — like other previous pipeline cut-offs — does not preclude a future resumption of energy trade with Moscow. Depending on the resolution of the Ukraine conflict and Europe's economic pressures, Russian gas could in the medium to long term re-enter the European market, albeit in reduced volumes. Any future energy relationship between Europe and Russia would be fundamentally different from the past, as Europe's diversification efforts would significantly reduce the geopolitical leverage Russia once held through its energy exports, should they resume. European governments will likely maintain measures to limit dependency and avoid repeating past vulnerabilities, and any renewed imports from Russia would occupy a significantly smaller share of Europe's future energy mix, as Russian gas would face growing competition from U.S. and Qatari LNG, as well as declining European demand as the Continent accelerates its transition away from fossil fuels.