A complete interruption of Russian gas supply through Ukraine would likely only have a limited and temporary impact on Europe's energy markets thanks to ample gas storage, alternative entry points and increased access to new global LNG supplies in the coming years. Russian state-owned gas giant Gazprom interrupted natural gas supplies to Austria on Nov. 16. The interruption followed a Nov. 13 warning from Austrian energy group OMV that Russia could disrupt supplies after an international arbitration ruling awarded Austria 230 million euros ($243 million) against Gazprom for damages related to Moscow's September 2022 decision to cease natural gas exports to Germany (including volumes destined for Austria). OMV's warning said the company expected a "deterioration of the contractual relationship" with Gazprom and a "potential halt of gas supply" as a result of the ruling, particularly as it planned to immediately recoup damages won in the arbitration by withholding payments for imports from the Russian company. The warning triggered a surge in European gas prices on Nov. 14, with European benchmark Dutch TTF futures rising as much as 5% to a one-year high of 46 euros per megawatt-hour. However, the market reaction to the actual Nov. 16 cut-off was largely muted when trading resumed on Nov. 18, as Gazprom redistributed the unsold volumes of Austria's 17 million cubic meters per day to other European buyers, keeping the overall supply to the Continent stable.

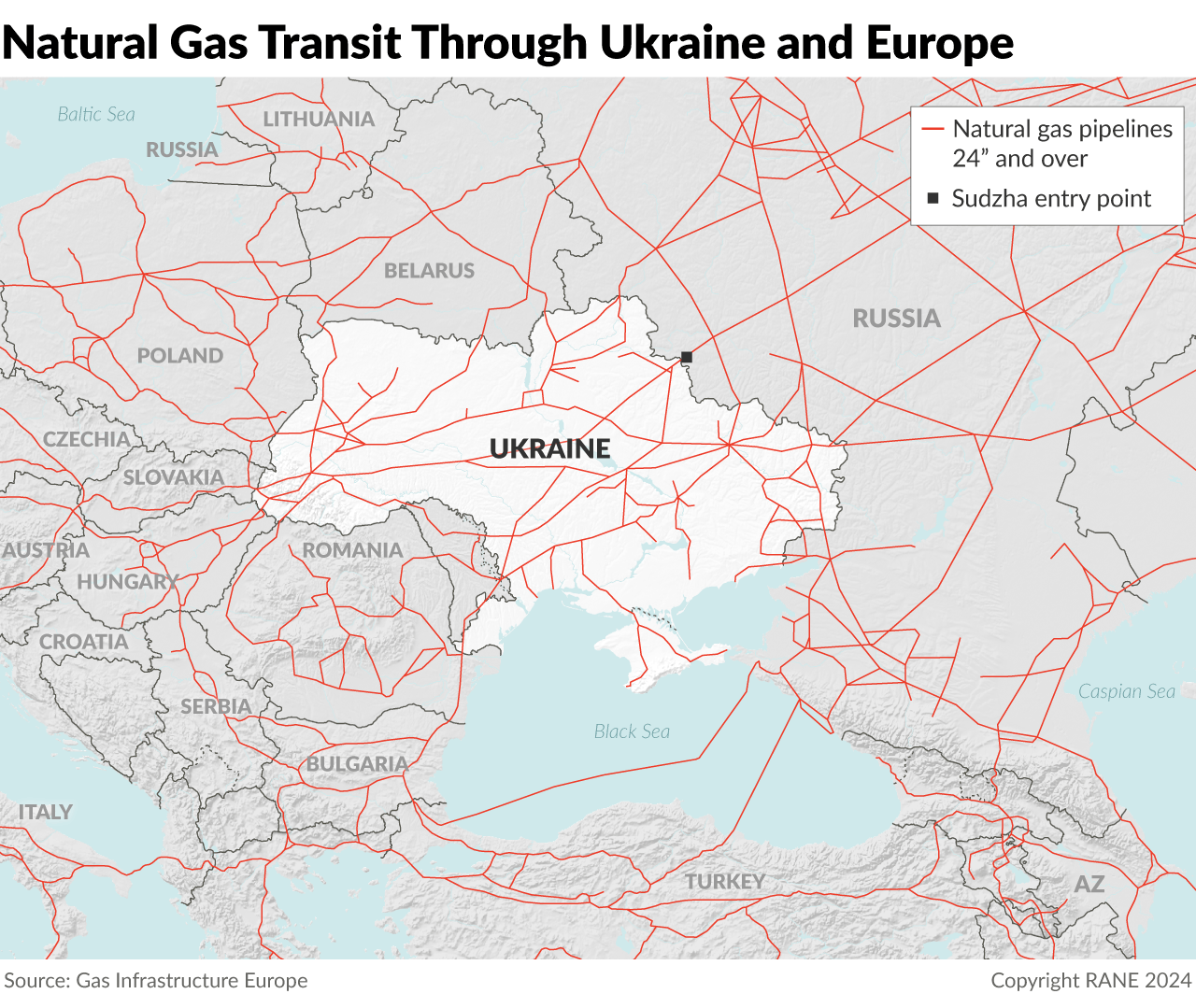

- Despite Russia's 2022 invasion of Ukraine, Russian pipeline gas has continued to flow through the war-torn country, although at reduced volumes, mostly ending up in Austria, Slovakia and Hungary. Together, the three countries import about 65% of their gas through Ukraine.

- While the European Union has drastically reduced its imports of Russian gas since the start of the war, Russia still accounts for around 15% of the bloc's total natural gas imports. About half of Russia's gas exports to Europe are liquified natural gas, or LNG, with the other half roughly equally split between the TurkStream pipeline and pipelines that cut through Ukraine. Supplies through Ukraine currently account for only about 5% of the European Union's total natural gas imports, down from 11% in 2021. Overall, Russia delivers around 15 billion cubic meters of gas to buyers in the European Union through Ukraine.

Russian gas supplies to Europe via Ukraine are expected to end on Jan. 1, 2025, after the existing transit agreement expires, as an extension or alternative arrangement remains unlikely for now, even with the inclusion of a third-party intermediary like Azerbaijan through swap arrangements. Ukraine's five-year transit agreement with Gazprom to transport natural gas to buyers in the European Union through its pipeline system connecting Russia to Slovakia will expire on Dec. 31. Kyiv does not intend to renew the agreement or strike any new deal involving a direct contractual relationship with Gazprom. Yet, all parties have reasons to be interested in some sort of transit agreement. Gazprom does not want to lose its remaining customers in Europe, while these customers — Hungary, Slovakia and to some extent Austria — would rather preserve privileged, direct access to pipeline gas, if possible. Ukraine, for its part, needs the transit fees to maintain its expensive gas transit system and would welcome any extra revenue to help offset its wide annual budget deficits. Against this backdrop, Kyiv is negotiating an alternative arrangement involving gas exchange deals with a neutral intermediary (most likely Azerbaijan) to keep the gas flowing. However, risks and constraints will significantly complicate negotiators' ability to reach a new agreement, including the potential for further destruction of Ukraine's pipeline infrastructure due to the ongoing conflict with Russia. Additionally, a new agreement would run counter to the European Union's goal of reducing and eventually phasing out dependence on Russian energy resources.

- Gazprom and Ukraine's Naftogaz brokered their current contract in December 2019 with the help of the European Union, Germany and France. The last-minute deal was signed to avoid repeating the 2009 crisis that led to a complete cut-off in gas supplies to southeastern Europe, which was fully dependent on Russian gas at the time. However, the lack of urgency for a deal this time around — as the worst of Europe's energy crisis has already passed — means Brussels, Berlin and Paris will not play this key mediating role, removing a fundamental driver of another agreement.

- Ukraine's gas transit system, one of the largest in Europe in terms of both transit and storage capacity, costs between 400 million euros and 800 million euros annually to maintain, meaning a large portion of the roughly 714 million euros Ukraine receives in annual transit fees is spent simply on system maintenance. Considering Ukraine uses the system to transport its own growing gas production, Kyiv needs these transit fees to prevent the system from falling into disrepair. Moreover, Ukraine's gas network would likely become a military target in Russia's ongoing bombing campaign against Ukraine's energy infrastructure if Russian gas were no longer passing through it, further increasing upkeep and repair costs for Ukraine.

- Interruption of gas transit through Ukraine would cost Russia an estimated $6.5 billion annually unless Gazprom can redirect these flows to LNG terminals or other pipelines, which it would only be able to do partly.

- Under a gas swap arrangement, Ukraine would establish a commercial contract with Azerbaijan's state-owned oil and gas company SOCAR to facilitate the transit of Russian gas through so-called swap agreements enabling Russian gas technically labeled as "Azeri" to continue flowing through Ukraine and reach European markets, while Russia would provide Azerbaijan with gas labeled as "Russian." Azerbaijan would be an ideal candidate to play this part thanks to its neutral and relatively balanced relations with both Kyiv and Moscow, as well as SOCAR's existing relations with European buyers and experience with gas swap deals. Even if negotiators do not reach such a deal before the Russia-Ukraine transit agreement expires at the end of the year, talks could continue through the first few months of 2025.

An earlier interruption of Russian gas supply through Ukraine would result in short-term price volatility in Europe, but the medium-term impact would likely be minimal thanks to sufficient alternative supply. The early interruption of Russian gas supply to Austria has barely impacted prices since overall volumes supplied to Europe remained stable. But even a sudden cut-off before the end of 2024 would likely only cause short-term price volatility, as OMV and other buyers in central Europe have long been preparing for the potential end to pipeline flows via Ukraine, mitigating the risk of eventual supply disruptions. For instance, OMV has built up gas reserves (now reportedly at 90% of capacity in Austria) and secured alternative supplies as part of its diversification strategy away from Russia, including additional piped volumes from Norway and long-term LNG supply deals, that would enable it to meet contractual obligations to customers even in the case of an earlier-than-expected interruption of supply via Ukraine. These preparations will serve the Continent well even if supply remains stable through the end of 2024, as Russian gas deliveries would still end in 2025 without a new transit arrangement between Russia and Ukraine. In this scenario, the impact on the energy security of Austria, Hungary or Slovakia would still be minimal thanks to ample alternative supply on the Continent through LNG terminals and floating regasification units in nearby countries like Croatia, Greece, Germany, Italy, Lithuania and Poland that are connected to the three landlocked countries via pipeline infrastructure. Moreover, the tightness in the global LNG market that has so far sustained prices in Europe is set to ease over the next few years as substantial new supplies from Qatar and the United States come online in 2025-26. This new supply should help reduce price pressures in Europe even in the case of a complete interruption of Russian supplies through Ukraine, barring any major events that create supply and/or demand shocks, like incidents affecting Europe's gas infrastructure or a particularly cold winter in Europe or Asia over the next couple of years.

- The end of the transit contract would also mark a significant step in Europe's quest to achieve independence from Russian energy supplies, accelerating a planned complete decoupling by 2027 under the RePowerEU non-binding targets. This would further rob Moscow of its ability to weaponize its energy exports to increase pressure on the West over support of Kyiv's war efforts. As the Kremlin looks for new ways to preserve this leverage, Russia may grow more interested in directly targeting Europe's energy infrastructure (or threaten to do so) through conventional or unconventional operations, including physical attacks or cyberattacks.

- To make up for the missing volumes of Russian gas through Ukraine, Europe would need to import an additional 15 billion cubic meters per year of LNG. This figure would increase in case of a particularly harsh winter that depletes inventories by the end of the heating season in Europe. Coupled with potential further delays in the completion of various LNG projects expected to come online next year (with some big projects like Mexico's Golden Pass and Energia Costa Azul LNG recently pushed to 2026), this could lead to a tighter-than-expected global LNG market next year, pushing up prices in Europe and Asia.