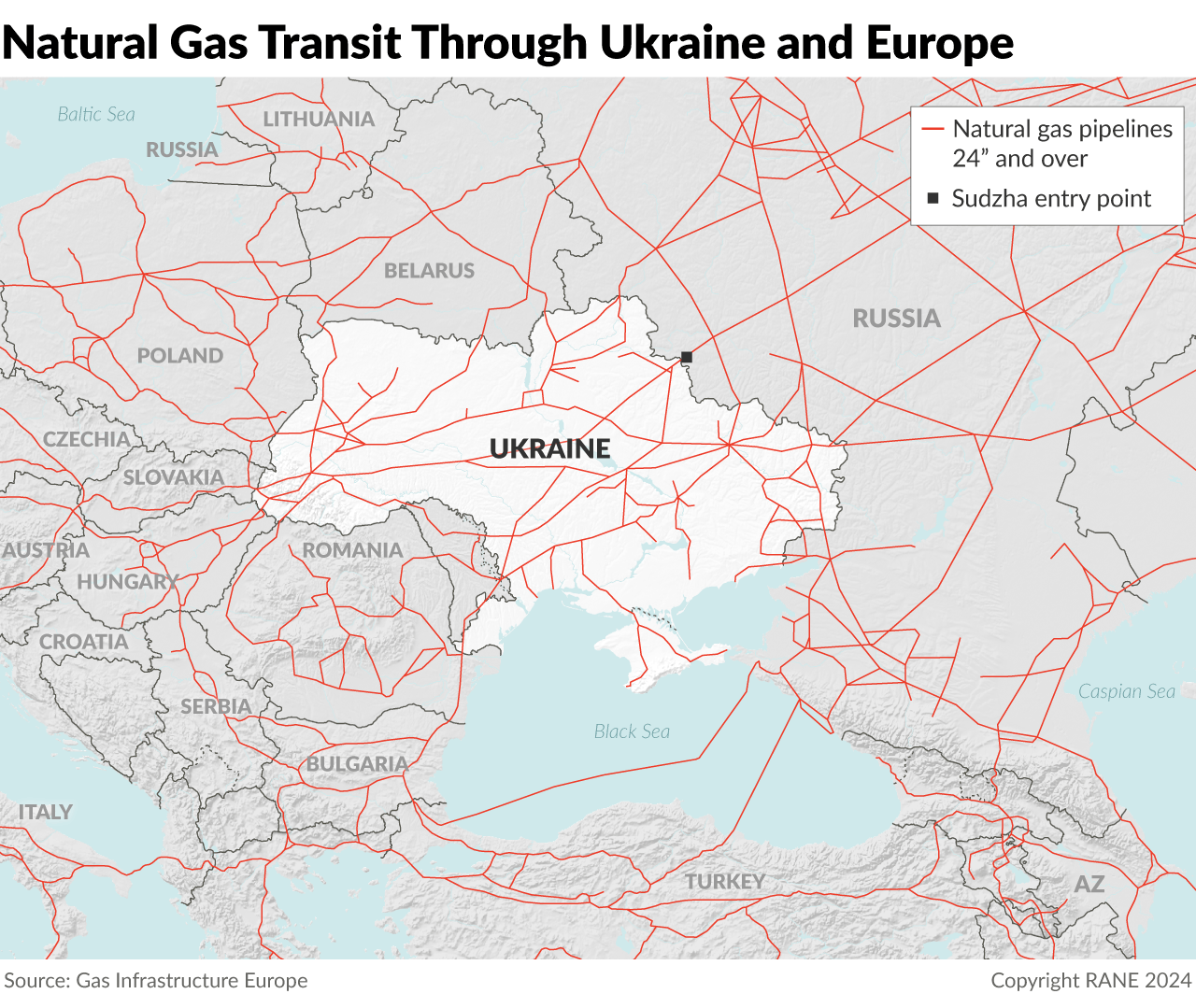

While Russia and Ukraine are interested in a natural gas transit agreement allowing continued gas deliveries to Europe, a deal would require the involvement of Azerbaijan or another third party and faces significant commercial, political and tactical constraints that make it ultimately unlikely by year's end. On Dec. 31, Ukraine's natural gas transit agreement with Russian state-owned gas giant Gazprom will expire. The five-year deal is set to deliver around 15 billion cubic meters (bcm) of gas to buyers in the European Union in 2024, though these flows through Ukraine now account for less than 5% of the Continent's gas supplies. Ukraine does not intend to renew the agreement but is negotiating with Azerbaijan and European buyers for an alternative deal with Gazprom, which would likely involve gas swaps, to keep around 10 bcm per year of gas flowing. Specifically, Ukraine's government is pursuing a commercial contract with Azerbaijan's state oil and gas company SOCAR to facilitate Russian gas deliveries through Ukraine. A transit agreement between Ukraine and SOCAR would involve the shipment of Russian gas through Ukraine's gas transit system, with SOCAR merely providing small amounts of gas to Russia for swaps and serving as a contractual intermediary for the commercial relationship.

- On Oct. 7, Ukrainian Prime Minister Denys Shmyhal reiterated to Slovak Prime Minister Robert Fico that Ukraine would not extend its gas transit agreement with Russia due to Ukraine's "strategic goal to deprive the Kremlin of profits from the sale of hydrocarbons used to finance its invasion." Slovakia's state-owned gas buyer SPP had as recently as Sept. 26 said it is continuing negotiations to extend Russian gas transit through Ukraine.

- On Sept. 19, Reuters misreported that Ukraine had agreed to transit Azerbaijani gas to the European Union at the bloc's request through a swap scheme, prompting European benchmark Dutch TTF spot gas prices to fall temporarily over 10% before bouncing back when Reuters corrected the report hours later. These price swings highlight how sensitive European natural gas prices are to future transit through Ukraine.

- On Oct. 9, Russian Deputy Prime Minister Alexander Novak said Russia is not currently discussing gas swaps with Azerbaijan and that specific gas transportation infrastructure for such swaps had not been created. The comment suggested talks on SOCAR facilitating a Ukraine gas transit deal remain at an early stage and that large gas swaps between Russia and Azerbaijan may not be necessary for a deal.

- In the opening days of Ukraine's ongoing incursion in Russia's Kursk region, which commenced on Aug. 6, Ukrainian forces seized the Sudzha gas metering station, through which Russian gas sales to Europe flow, raising questions about the future of gas transit through Ukraine. But despite damage to the administrative buildings and potentially other infrastructure at the facility, Russian gas has continued to flow onward to Europe as before.

Russia, many key EU member states and Ukraine all have reasons to be interested in a deal. Russia is interested in a transit agreement through Ukraine under almost any circumstance because Gazprom is in financial straits following the loss of its deliveries to European clients, with its current gas deliveries to Europe at only 8% of their peak volume in 2018-19. With the future of gas sales to China still uncertain, Gazprom is eager to sell what gas it can to avoid becoming a liability to the Russian budget and having to shut in gas production. Meanwhile, several influential EU member states — such as Germany, Italy and France — would support a new transit deal to diffuse upward pressure on gas and power prices across the Continent, particularly since a deal would not threaten to derail the bloc's ability to end Russian gas purchases by 2027. Finally, Kyiv also has reasons to be interested in a deal, albeit under certain conditions. This is because Ukraine's gas transit system, one of the largest in Europe in terms of both transit and storage capacity, costs 400 million euros-800 million euros (about $432 million-$865 million) annually to maintain, meaning a large portion of the roughly 714 million euros Ukraine receives in annual transit fees is spent simply on system maintenance. Considering Ukraine uses the system to transport its own growing gas production, Kyiv needs these transit fees to prevent the system from falling into disrepair, particularly as upkeep and repair costs are only set to rise as Russia continues its strike campaign on Ukrainian energy infrastructure. Kyiv would also welcome excess transit revenues to offset its annual budget deficits, which run in the tens of billions of dollars.

- According to Russia's 2025-27 draft budget, state revenue from oil and gas is expected to decline in the coming years, primarily driven by a 30% reduction in mineral extraction taxes levied on Gazprom starting next year, in a bid to help the company remain profitable. Gazprom reported an annual net loss of $7 billion in 2023, its first since 1999.

- Ukraine's budget deficit in 2025 is expected to total about $38 billion, but the government only planned to cover $20 billion and is still searching for additional revenues and external support to cover the remaining deficit.

- Ukraine received about 1.2 billion euros annually in transit fees from the 2019 deal with Russia until deliveries via the Sokhranivka entry point stopped in May 2022 during the early stages of Russia's invasion.

Ukraine and Russia would be more likely to reach a deal if a neutral third party agrees to serve as an intermediary, most likely Azerbaijan's SOCAR, with talks set to continue over the coming months and possibly into 2025. Negotiations will likely center on an agreeable third party serving as an intermediary, with Azerbaijan's SOCAR being the most viable partner to facilitate a deal for several reasons: Azerbaijan is one of the very few countries that maintains productive political and commercial relations with both Moscow and Kyiv, SOCAR has extensive experience working with European gas buyers, and Azerbaijan can transit its own gas into Russia to engage in swap arrangements. Azerbaijan also has extensive experience negotiating swap deals, which may be needed to make the continued transit of Russian gas through Ukraine more politically palatable to both Kyiv and Moscow, as well as for the West, which would like to see Baku take at least a small portion of the revenue that would otherwise go to Moscow. Furthermore, participating in a swap deal is the only way for Baku to increase its own gas sales until the Southern Gas Corridor's expansion concludes, as its three pipelines to Europe are already operating at full capacity. Therefore, Baku's involvement in deliveries through Russia and Ukraine presents an easy opportunity to increase Azerbaijan's geopolitical leverage over Russia and the West. The most likely alternative to Azerbaijan in playing this intermediary role is Turkey, but there is little indication that Ankara or Turkish companies are significantly involved in the talks. Alternatively, Gazprom could conclude contracts directly with European entities, which would then conclude agreements with Ukraine's Naftogaz, though this scenario would come with additional sanctions and other risks to European entities.

- Reports indicate that discussions remain nascent, meaning any agreement will likely come only at the last minute or after the current deal expires. There is thus a significant possibility that Russia could continue gas flows — and transit payments to Ukraine — even after the agreement expires on Jan. 1, 2025, as a "goodwill gesture" to encourage negotiations, and Ukraine would be hesitant to shut off Russian gas flows completely under this circumstance. In theory, this limbo period could persist for weeks, though Moscow eventually would shut off flows if it does not believe it will be appropriately compensated for the gas.

A deal may fail due to numerous constraints, including potential further destruction to Ukraine's infrastructure at the hands of Russia, commercial conditions and competition from Europe's growing alternatives to Russian gas, and political constraints in Kyiv and Moscow. The most immediate threat to future transit is the physical destruction of key portions of Ukraine's gas transit system, which could temporarily render deliveries technically infeasible and potentially more costly. Further damage to the Sudzha facility, the rest of the Urengoy-Pomary-Uzhhorod pipeline, or smaller pipelines, storage facilities and compressor stations in Ukraine could cause Russian gas transit across Ukraine to cease entirely even before the end of this year. This is why Kyiv is reportedly seeking a guarantee of the security of its pipeline infrastructure from Russian strikes as part of the deal, though Moscow will likely reject or ignore this demand. Even if significant infrastructure damage is avoided, another major obstacle to reaching an agreement is the lack of urgency, as the worst of Europe's energy crisis has already passed; European gas prices are below their pre-Ukraine invasion levels and remain relatively stable. Additionally, the bloc's structural dependency on Russia is falling amid increased LNG intake capacity and global production to compensate with each coming year, in line with the bloc's REPowerEU plan to phase out all Russian fuel imports by 2027. The greatest challenge, however, lies in the complex strategic and domestic political concerns of the involved parties, as neither Kyiv nor Moscow wants to be seen as giving the other an advantage on the battlefield. Since the deal would free up budgetary resources that both sides could use to fund the war, the optics of such an agreement are difficult for either to accept. Thus, Kyiv will remain firmly against an extension of the current agreement — or any deal involving a direct contractual relationship with Gazprom, and it may take a significant improvement in the transit payments and conditions in Ukraine's favor to prevent the deal from being seen as funding Russian war efforts, even if Azerbaijan facilitates the agreement. Moscow is similarly constrained, as Gazprom's strong desire for a deal will likely be met with skepticism from some hardliners in the Russian government and security officials, who may believe the benefits of destroying Ukraine's gas transit systems to pressure Kyiv and Europe outweigh the benefits of further gas sales.

- Experts estimate that over 25 million cubic meters (mcm) of Russian gas per day (or roughly 10 bcm per year) may be needed to support the commercial and technical viability of further Russian gas flows through Ukraine, as smaller amounts become less economic and may not achieve adequate pressure to smoothly transport the gas.

- Although it stores some gas for European consumers, Ukrainian imports of gas for domestic use are currently negligible, as energy consumption has dropped drastically due to the war, and Ukraine's domestic gas needs are fully met by its own production, which has increased by 7% in 2024 compared with last year, reaching 53 mcm per day. Most of its domestic production comes from gas fields in eastern Ukraine. A drop in pressure in its gas pipelines — due to the end of Russian gas flows and damage to the system from Russian strikes or a combination of the two — could complicate the distribution of this production to the rest of Ukraine for heating and electricity this winter.

- Kyiv is concerned that a deal could significantly undermine its push to encourage European partners to reduce their reliance on Russian gas, limit Moscow's revenue, and urge European businesses to withdraw from Russia. The EU countries most reliant on Russian gas transiting Ukraine are Austria, Hungary, Slovakia and Czechia, and while they would favor a deal, they likely lack the weight in negotiations to ensure one. Furthermore, they have had much greater access to the global LNG market since 2022, which will only further increase in the years ahead due to the steady expansion of regasification terminals in Italy, Germany, Poland, Lithuania and Croatia and the growing availability of LNG on the global market starting in 2025.