By replacing Russian gas with U.S. LNG, the European Union risks swapping a strategic dependence on Moscow for one on Washington — a relationship that, though fundamentally different, would not be immune to the use of energy as a tool of political and economic leverage, and that could leave the bloc operating with tighter market buffers and greater price volatility through the end of the decade, even as diversification reduces single-supplier risk. On Jan. 26, EU energy ministers approved legislation to phase out imports of Russian pipeline gas and liquefied natural gas (LNG) by the end of 2027. The phased ban will begin taking effect six weeks after it enters into force and tighten progressively through 2027, requiring companies to unwind existing agreements within defined timelines or face financial penalties. Spot imports of Russian gas and LNG will be prohibited six weeks after publication. Russian LNG imports under short-term contracts concluded before June 2025 will be banned from April 2026, while imports under long-term LNG contracts will be banned from January 2027. Pipeline gas imports under short-term contracts concluded before June 2025 will also be banned from June 2026, while imports under long-term contracts will be phased out from September 2027, with extensions possible until November 2027 if EU member states are not on track to meet gas storage targets. Russian oil imports are not covered under the approved package, though the European Commission has indicated it plans to submit additional legislation later this year to also prohibit Russian oil imports by the end of 2027.

- The measure passed despite opposition from Hungary and Slovakia, which are among the European Union's largest Russian gas importers. This was possible because it was structured as a trade policy instrument, which, unlike sanctions, does not require unanimous member state support or renewal every six months. Hungary and Slovakia said they will challenge the measure at the European Court of Justice on the grounds that energy policy falls under national competence, that energy imports can only be banned through EU-level sanctions, and that the disproportionate impact on the two countries violates the principle of energy solidarity within the bloc.

- Previously, there was no general EU ban on importing Russian gas, allowing companies to continue deliveries under existing contracts and, in principle, to enter into new ones. The only bloc-level restrictions in force were introduced in 2024 and were limited in scope, notably banning the transshipment of Russian LNG through EU ports for re-export to third countries. Beyond this, restrictions at the EU level had remained largely indirect, excluding Russian gas from joint purchasing and demand-aggregation schemes while leaving national authorities the discretion to restrict import capacity for Russian pipeline gas and LNG.

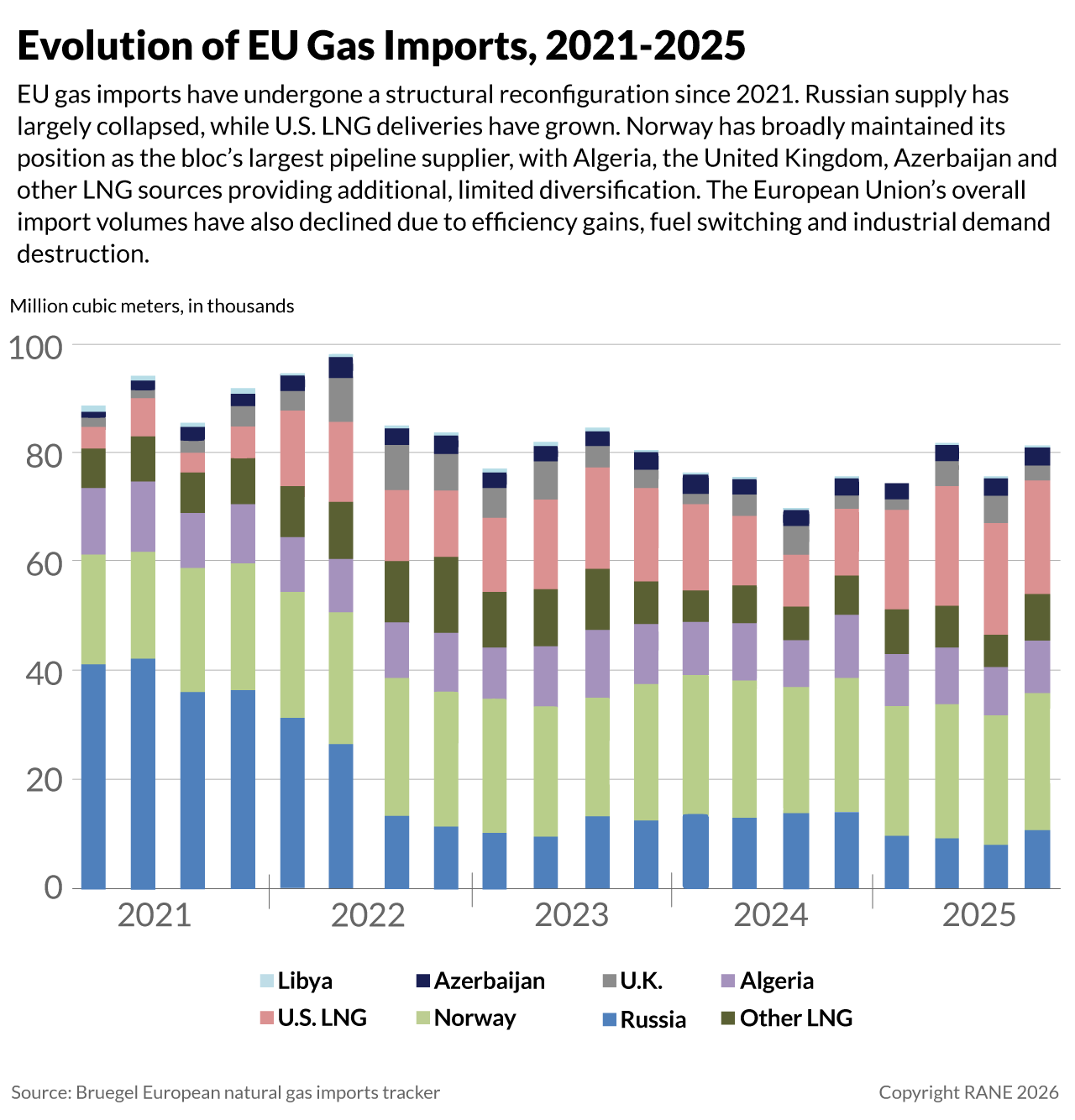

The European Union has significantly reduced its reliance on Russian energy since the 2022 invasion of Ukraine, largely by expanding U.S. LNG imports. Russian natural gas now accounts for only about 12% of the European Union's total imports, down from 45% before the war. However, Russia remains the bloc's second-largest LNG supplier. Since early 2022, the European Union has reduced this exposure through a combination of demand reduction, mandatory storage requirements, diversification of supply routes and, most significantly, a rapid expansion of LNG import capacity that has made liquefied gas a key component of the European Union's baseline supply. In 2025, the bloc imported record LNG volumes, which the European Commission estimates accounted for around 46% of total gas imports, with pipeline supplies falling to roughly 54%, reflecting in part the termination of Russian transit via Ukraine. Russian gas made up about 10% of total pipeline imports last year, while Norway remained the European Union's largest supplier, providing roughly 30%. As Russian volumes declined, replacement supplies have come primarily from rising U.S. LNG imports, with the United States emerging as the European Union's dominant LNG supplier, delivering approximately 80-82 billion cubic meters in 2025, or around 58% of LNG imports and roughly 27% of total EU gas intake, nearly quadruple 2021 levels.

In the short term, the phasing out of Russian gas is unlikely to cause major supply disruptions or price hikes thanks to expanding global LNG supply, rising regional production and alternative supply routes, though Central Europe will remain more exposed to supply risks. Most EU member states affected by the ban will manage to secure alternative supplies without significant price increases. On the LNG side, the removal of Russian cargoes from northwest European markets will be compensated by higher inflows from other suppliers, led by the United States, while Russian LNG will largely be redirected toward Asian markets. This reshuffling will reduce global market efficiency and push spot prices slightly higher in both Europe and Asia, but it will not significantly tighten supply. Moreover, by the time the full ban takes effect at the end of 2027, a large wave of new LNG export capacity — driven mainly by projects in the United States and Qatar and set to expand global supply by more than 50% by 2030 — will be coming online, easing price pressures. Across the European Union as a whole, the pipeline gas ban will lead to greater reliance on LNG and tighter use of existing infrastructure, resulting in only modest upward price pressure and no supply deficit under normal conditions. Central and southeastern Europe will remain the most exposed regions to short-term price volatility due to their distance from LNG terminals and reliance on pipeline flows, though countries should be able to adjust through alternative routes and regional supply substitution. The loss of remaining Russian flows via TurkStream will reduce supplies entering Bulgaria and transiting onward into Central Europe, but rising Black Sea output from Turkey and Romania will offset much of this shortfall. If expected production growth in either country falls short or is delayed, Turkey and Greece could increase LNG imports and reroute additional volumes through Bulgaria into Central Europe. Slovakia will rely more heavily on west-to-east transit via Poland, the Czech Republic and Austria. Austria will also continue to source most of its gas through Germany, while Hungary will increasingly depend on Romanian pipeline supplies and LNG imports via Croatia. However, these routes will operate close to capacity, leaving limited redundancy. As a result, while existing infrastructure, LNG access and rising regional production will prevent structural supply deficits, risks will remain around system resilience, as disruptions at key cross-border points could translate quickly into supply shortfalls.

Over the longer term, Europe's pivot away from Russian gas risks concentrating supply exposure on U.S. LNG, creating a potential source of vulnerability amid an increasingly volatile geopolitical environment and a more transactional transatlantic relationship, even though the commercial and legal structure of the U.S. LNG market makes deliberate supply weaponization unlikely outside extreme crisis scenarios. Current projections indicate that by 2030, U.S. LNG could account for 75-80% of EU imports and up to 40% of the bloc's total gas intake as Russian gas exits the system. This prospect is intensifying a debate in Brussels over the risk of replacing energy dependence on Moscow with one on the United States amid renewed transatlantic tensions. This exposure differs fundamentally from the European Union's pre-2022 reliance on Russian energy, which was mostly based on long-term contracts with state-controlled Gazprom. U.S. LNG is sold by multiple, competing private companies operating in a liberalized market, which complicates Washington's ability to directly suspend flows or coordinate politically motivated supply restrictions. That said, U.S. LNG exports are still subject to federal export authorizations, trade policy and emergency powers, which could give the U.S. president significant leverage over export volumes and conditions in extreme circumstances, even if day-to-day cargo flows are not subject to discretionary political approval under normal conditions. This risk is heightened by President Donald Trump's transactional foreign policy and his readiness to test institutional and legal constraints to coerce other countries, adversaries and allies alike. The likelihood of abrupt supply cut-offs remains significantly lower than in the Russian case, and there is no evidence the United States would weaponize LNG exports the way Moscow did after 2022. However, the European Union's growing reliance on U.S. LNG raises the risk that energy dependence could again become a vector of political pressure. Although the legal and commercial structure of the U.S. LNG sector makes discretionary supply interruptions under normal conditions both difficult and economically costly, this concentration risk would become more salient in a severe geopolitical crisis, a major rupture in transatlantic relations or a war affecting global energy flows.

- On Jan. 28, European Energy Commissioner Dan Jorgensen said the European Union would step up efforts to diversify its energy supplies away from U.S. LNG following recent threats by Trump to take control of Greenland. He described the developments as a wake-up call, warning that the European Union risks "replacing one dependency with another," and said diversification efforts would focus on securing new supply agreements with Canada, Qatar and North African countries, alongside boosting domestic energy production to reduce reliance on gas imports.

- Under the Natural Gas Act, the Department of Energy authorizes the export of LNG to non-FTA countries at the project level, typically sought prior to final investment decision and construction in order to underpin financing and contracting. Once this authorization is granted, exporters do not require federal approval for individual cargoes, destinations, or underlying commercial contracts. The commercialization and scheduling of LNG shipments occur without routine government involvement, and all operating U.S. export projects currently hold non-FTA export authorizations. In practice, if an authorized exporter contracts a cargo to a European buyer, it can proceed without a case-by-case political sign-off. That said, exports remain subject to the broader statutory framework governing national emergencies and energy security, meaning that in an extreme crisis or wartime scenario, a U.S. administration could seek to restrict or condition export activity under emergency authorities. However, any suspension or revocation under the Natural Gas Act would apply to all non-FTA exports rather than selectively to specific destinations. Targeted restrictions would likely require legislative changes or reliance on broader emergency powers. A U.S. administration could, in theory, attempt to impose targeted restrictions under the International Emergency Economic Powers Act, but doing so against allied buyers would be politically contentious, subject to congressional review of the underlying national emergency and likely vulnerable to legal challenge. Outside an extreme crisis or wartime scenario, such measures would be difficult to sustain in practice.

- The Trump administration explicitly framed "energy dominance" as a priority in its 2025 National Security Strategy, calling for expanded energy exports as a means of projecting U.S. power abroad. In the document, this is articulated primarily in terms of deepening alliances and curtailing adversaries' influence over global energy markets, but it also underscores the extent to which Washington views export capacity as an instrument of geopolitical leverage. The White House is actively seeking to expand net energy exports to European allies and has used trade pressure to secure large-scale EU purchases, as evidenced by the European Commission pledging to procure up to $750 billion in U.S. energy products by 2028 as part of the EU-U.S. trade framework agreement reached in July 2025.

Brussels aims to mitigate this exposure by reducing the need for gas through renewables, nuclear power and efficiency gains, but structural constraints mean gas will remain a core component of Europe's energy and industrial systems for the foreseeable future. Under its REPowerEU plan, the European Union has already reduced gas consumption by roughly 20% since 2021 and aims to cut it by up to 25% by 2030. Meanwhile, the International Energy Agency projects European gas demand to fall by 8-10% by 2030 from 2024 levels, driven mainly by a sharp decline in gas-fired power generation as renewable electricity output expands by more than 40%. Gas-to-power demand alone is expected to drop by around 25%, while industrial consumption is projected to decline only modestly. This reduction will be concentrated in Western Europe, while gas use in parts of Eastern Europe is set to rise slightly as coal and lignite plants are phased out. Nuclear power will also help displace gas in electricity generation, but it will not make a meaningful dent in overall EU natural gas demand by 2030. This is because most new reactors are unlikely to enter service before the mid-2030s, and lifetime extensions remain limited relative to planned retirements. New-generation technologies, such as small modular reactors, are also unlikely to be commercially available at scale before the mid-to-late 2030s. As a result, total installed nuclear capacity in the European Union will likely remain broadly flat, or only marginally higher, by the end of the decade. Moreover, greater reliance on renewables and nuclear will not eliminate the need for gas-fired generation. Nuclear provides steady baseload output, but gas remains essential for system flexibility, especially as the share of variable renewables rises, balancing variable wind and solar generation in the absence of large-scale storage and grid reinforcement. In industry, gas will be even harder to replace. It remains a critical energy source for high-temperature heat in energy-intensive sectors and a key feedstock for fertilizers and basic chemicals. Hydrogen is often presented as an alternative for decarbonizing industrial gas use, but for most industrial users, the economics do not yet justify large-scale fuel switching — or concrete plans to do so in the future — without sustained and predictable public support. Government backing for green hydrogen projects and infrastructure has been facing delays, funding constraints and regulatory uncertainty. And even where state-backed investment proceeds, notably in Germany, it focuses mainly on dual-use infrastructure designed to accommodate natural gas for an extended period before any potential conversion to hydrogen, if such a transition ever occurs.

With natural gas remaining central to its energy mix, the European Union will seek to further diversify its supplies in the coming years, but options to meaningfully reduce reliance on U.S. LNG will be limited until the 2030s. The European Union will accelerate efforts to rebalance LNG and pipeline imports as it completes its phase-out of Russian fossil fuels. On LNG, the bloc is expanding ties with Qatar and the United Arab Emirates. While much of these Gulf Arab countries' supply remains oriented toward Asian markets under long-term contracts, capacity expansions, portfolio flexibility and secondary market resales will support incremental European volumes. Australia could also gradually contribute limited incremental LNG volumes to Europe, but its role will remain constrained by distance, higher transport costs and the prioritization of Asian markets, making it more of a balancing option than a central piece of European diversification. Canada is a longer-term option, but infrastructure gaps, political hurdles, long project timelines and regulatory uncertainty constrain commercial viability in the short- to medium-term. West and East African LNG adds flexibility, but volumes remain modest. On the pipeline side, Norway will remain Europe's largest supplier, but, as a mature producer operating near capacity, the country will prioritize maintaining output more than expanding it. Romania's Neptun Deep field will turn the country into a net exporter from 2027, though volumes will primarily serve southeastern Europe. North Africa and the eastern Mediterranean offer longer-term potential but are constrained by political risk, financing challenges and infrastructure gaps that limit the scope for sustained export growth, despite abundant resources and proximity to European markets. The European Union could also expand gas imports from the Caspian region, but this would require sustained investment, infrastructure buildup and geopolitical alignment over many years. Taken together, these limitations will likely prevent significant diversification away from U.S. LNG this decade, meaning the United States is set to remain Europe's single-largest external gas supplier through the late 2020s.

- Qatar is undergoing one of the largest LNG expansions in the world, planning to boost liquefaction capacity from about 77 million tonnes per annum (mtpa) today to roughly 126 mtpa in 2027 and 142 mtpa by 2030, for an almost 85% increase in output capacity. Much of this new capacity will be available for flexible trading and short-term cargoes by decade's end, including shipments to Europe. However, contract coverage remains high, with much of Qatar's LNG under long-term deals through the 2030s, which can limit flexible volumes available for European spot demand. Moreover, Doha has warned that EU environmental rules could constrain access to the European market, as Qatar continues to favor long-term, oil-linked contracts with limited destination flexibility. This directly clashes with Europe's preferred contracting model for hub-indexed pricing and shorter commitments; so far, major European importers have only concluded a handful of long-term supply agreements, typically spanning 15 to 27 years. Still, high contract coverage does not imply complete destination rigidity. Many LNG contracts allow for resale, swaps or portfolio reallocation, meaning that even volumes formally committed under long-term agreements can be redirected across regions in response to price signals. Should the United States ever restrict LNG exports to Europe, market arbitrage would likely re-route cargoes through secondary trading and portfolio exchanges.

- In the eastern Mediterranean, large gas fields off the coast of Cyprus could supply gas to Europe, but this option is limited by high development costs, persistent delays in investment decisions and ongoing geopolitical instability in the region. Progress also depends heavily on Egyptian infrastructure, which Cairo is increasingly prioritizing to offset declining domestic production. Regulatory frictions and unresolved commercial frameworks have already pushed any meaningful export timelines into the late 2020s or early 2030s, leaving the scale and reliability of these supplies uncertain.

- Algeria and Libya offer geographic proximity, established pipeline links to Europe and a long-standing commercial presence of European majors, but scope for export growth remains structurally constrained. Algeria's mature fields, rising domestic demand and delayed upstream investment limit additional volumes, while Libya's large reserves remain locked by political fragmentation, security risks and degraded infrastructure, keeping exports well below capacity and making any increase dependent on sustained stability and capital inflows.

- Existing routes from Azerbaijan to Europe via the Southern Gas Corridor are already largely contracted. Any meaningful expansion — including potential volumes from Turkmenistan — would also require costly field development, new Trans-Caspian infrastructure, pipeline upgrades and sustained political alignment among producer, transit and consumer countries over many years.

However, the European Union's diversification strategy is unlikely to reverse the shift toward structurally higher and more volatile energy prices relative to pre-2022 levels, which could eventually lead to a limited return of Russian energy imports, should geopolitical conditions allow. The coming wave of new global LNG supply will help push prices down from recent highs and limit the risk of extreme spikes, but European gas prices are unlikely to return to pre-2022 levels. Deeper integration into global LNG markets will also increasingly tie European hubs to Asian demand cycles, shipping constraints, weather variability and more geographically dispersed geopolitical disruptions, while seasonal volatility will persist even as average prices ease. For European buyers, utilities and infrastructure operators, this environment complicates investment decisions. Volatile prices, uncertain demand trajectories and policy risk constrain appetite for long-term gas infrastructure and contracts, thereby reducing spare capacity and system redundancy and increasing exposure to potential disruptions. Supply security will thus improve, but with tight margins. Storage, LNG terminals and cross-border interconnections will operate at near capacity, increasing vulnerability to infrastructure failures and transit disruptions, particularly in central and southeastern Europe. In this context, moderate shocks could still quickly lead to limited price and local supply disruptions, even if there are no widespread, system-wide shortages. Meanwhile, higher and less predictable energy costs will continue to weigh on Europe's industrial base, with energy-intensive sectors facing a durable cost disadvantage relative to North American competitors. The energy price advantage Europe historically enjoyed over parts of Asia has also already evaporated, widening the competitiveness gap and reinforcing capacity rationalization, delayed investment and selective relocation. Much of the demand destruction since 2022 is therefore likely permanent, and any stabilization later in the decade will occur at lower volumes and with greater price sensitivity. Persistently high energy costs and relatively tight supply-demand balances — combined with the risk that global LNG markets tighten faster than expected as electricity demand rises with data centres and digital infrastructure — create the possibility of Russian gas re-entering Europe's energy mix in the future. This would hinge on a shift in geopolitical conditions (namely, a stable peace in Ukraine and normalized EU-Russia diplomatic relations), and could be fueled by growing concerns about over-dependence on U.S. gas supplies. Any such return, however, would occur under stricter safeguards and lower volumes. Brussels and Moscow's energy relationship would also be fundamentally different, as European diversification efforts would significantly reduce the geopolitical leverage Russia once held through its energy exports.

- Legally binding phaseout targets under RepowerEU will be difficult to reverse, but not impossible. Over time, the existing pipeline infrastructure could make historically cheaper Russian gas supplies attractive once again if high energy costs continue to strain competitiveness. Alongside a resumption in LNG imports, the reopening of the Nord Stream pipeline between Europe and Russia cannot be ruled out, while a resumption of flows via the Yamal pipeline looks less likely amid political opposition from Poland. While unlikely, flows could even resume through Ukraine as part of a peace agreement that might include provisions for restoring gas transit, providing Kyiv with much-needed transit fees for recovery and reconstruction — assuming Ukraine's pipeline infrastructure remains intact by the end of the war.