South African President Cyril Ramaphosa (center) delivers his 2023 state-of-the-nation address at the Cape Town City Hall on Feb. 9, 2023.

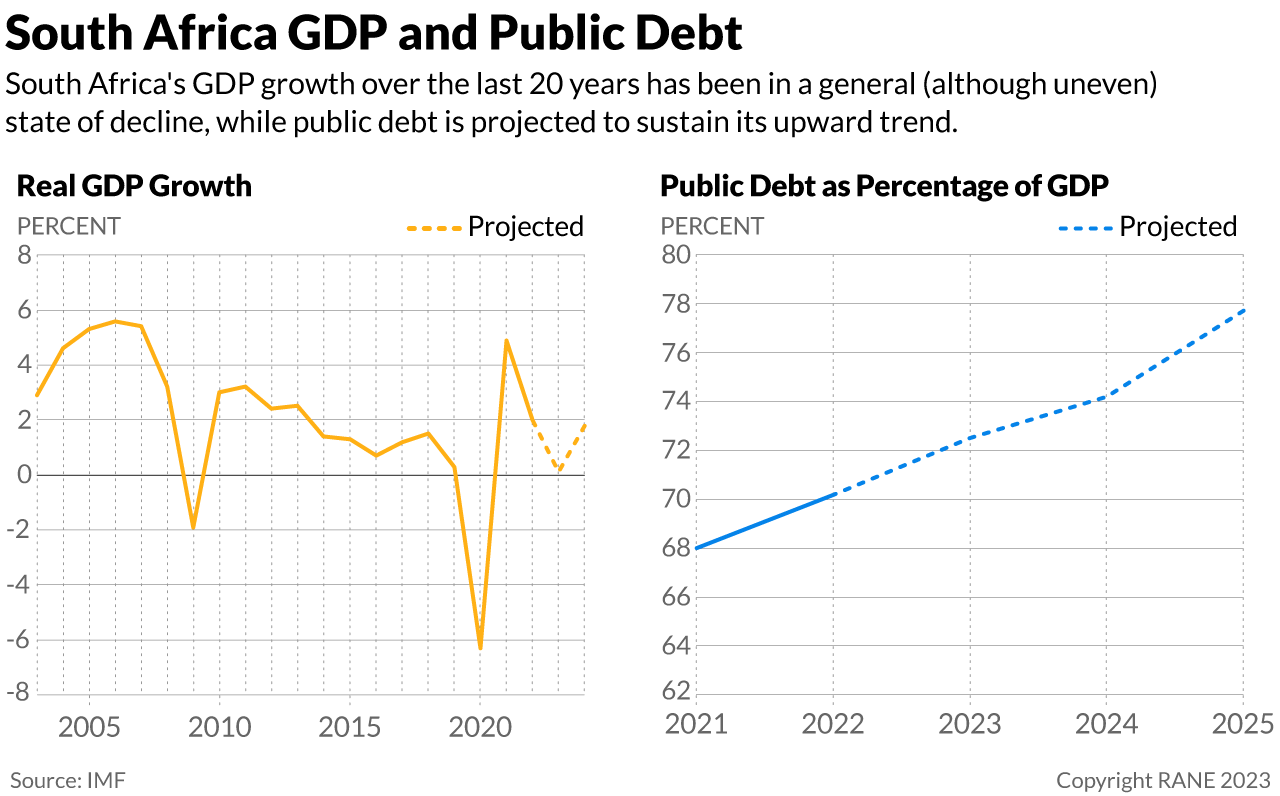

South Africa's economic decline and the ruling party's waning support will continue to deter the implementation of structural economic reforms, portending persistently low growth through the 2024 election and beyond. South Africa, the most developed country in sub-Saharan Africa, is in a long-term state of economic decline. The country's real GDP growth is projected to fall to 0.1% in 2023 from 2% in 2022, averaging 1.4% between 2010 and 2022. For the most advanced economy in sub-Saharan Africa, such a ten-year trend is troubling; the International Monetary Fund (IMF) projects that the average emerging market economy's real GDP growth rate in 2023 will fall to 2.8% from 3.4% in 2022. On top of low growth, South Africa has a mounting public debt problem, made worse by IMF predictions that the fiscal balance will take on a wider deficit of about 6.5% of GDP in the 2023-24 fiscal year (up from 5.5% in 2022-2023) and deteriorate further through the 2025-26 fiscal year. Similar to its GDP growth rates, South Africa's public debt-to-GDP ratio exceeds the average for emerging market economies by about five percentage points, and exceeds that of other sub-Saharan African countries by about 15 percentage points.

- External debt is less of a concern than public debt, given that South Africa's current account balance will move to a deficit of 2.3% of GDP in 2023 and 2.5% in 2024, which translates into a more-or-less stable debt ratio. External debt accounted for about 40% of the country's GDP in 2022, well below credit rating agencies and multilateral lenders' threshold of acceptable debt levels, which is generally around 55% of GDP.

- Headline inflation is expected to fall back within the South African Reserve Bank's target range of 3-6% in the second half of the year. Decreasing food and fuel prices and rising interest rates are the key drivers behind falling headline inflation (which hit a five-year record of roughly 8% in July 2022), which the IMF expects to reach 4% in 2024 and remain steady through the medium term.

- The current account balance deficit is driven by softer commodity prices for South Africa's minerals exports, lower external demand and the high cost of energy-related capital imports. In the medium term, the IMF projects that the current account balance will somewhat improve to 2% of GDP.

South Africa's economic stagnation is the result of several long-standing structural issues, but the country's electricity crisis has accelerated its economic decline in recent years. Structural impediments to growth, such as inefficiencies in labor market regulations and human capital constraints, have laid the foundation for South Africa's economic decline. The government continues to prop up and bail out failing state-owned companies like the electricity utility Eskom and transportation company Transnet, in part because their employees have historically voted for the governing African National Congress (ANC) party. For the same electoral reasons, the government has also maintained generous social safety net policies and a COVID-era cash transfer, further increasing its budget deficit. But South Africa's rapid economic deterioration in recent years is due largely to the ongoing electricity crisis, which has so far reduced South Africa's growth outlook by two percentage points in 2023 according to the South African Treasury. Years of corruption, mismanagement, a lack of investment and declining infrastructure have forced Eskom — which supplies about 95% of South Africa's electricity — to increasingly implement planned outages, known as ''load shedding,'' to stave off a complete grid collapse. The outages currently last between two to eight hours, but could become even longer and more frequent in the coming months as electricity demand spikes due to cold temperatures and Eksom's failing infrastructure. In a public briefing on May 18, Eskom's acting CEO warned his company may be forced to move to Stage 8 power cuts this winter, which could leave South Africans without power for 16 hours in a 32-hour cycle — likely costing the economy billions of rand worth of business.

- In February, Finance Minister Enoch Godongwana said he expects the government's public wage bill to reach 701.2 billion rand (roughly $37 billion), or over 30% of the annual budget, surpassing the level he once thought would be reached in 2025.

- The costs of South Africa's unreliable electricity supply are massive and all-encompassing. The central bank estimates that the electricity crisis may be costing the economy as much as $50 million per day, while disruptions to schools, hospitals, traffic and government services create myriad health, safety and development risks.

The South African government will pursue electricity sector reforms that could eventually mitigate harm to business activity, though their effect will not be immediate. In recent months, the government has carried out several measures to address the ongoing electricity crisis, including partial privatization of the sector, rehabilitating old and damaged power plants, and providing tax incentives for individual production of green energy. These measures were possible because the electricity crisis is so disruptive that virtually all political parties support varying degrees of reform. However, even if the measures are successfully implemented, it will likely take at least a year before they start mitigating the electricity crisis. The government will continue to pursue electricity sector reforms given the immense economic cost of load shedding, meaning that the extreme cost to business activity will likely be alleviated once the reforms take effect. Still, the government's inability to implement structural reforms in other areas will very likely facilitate continued economic stagnation.

Moreover, the ruling ANC party's low popularity ahead of the 2024 general elections will likely constrain the government's ability to implement necessary economic structural reforms. With general elections scheduled for 2024, the ANC is heading into its most contentious electoral period in history, with public support dipping below 50% for the first time in the party's history in the most recent round of municipal elections in 2021. The ANC's waning popularity is connected to the country's economic decline and worsening socioeconomic climate. Despite the government's high social spending, South Africa still suffers from sky-high levels of unemployment, poverty and inequality. Low popular support for the ANC makes the party even more dependent on labor unions in the mining, transportation, health and education sectors, among others. These unions comprise a key voting block for the party and have semi-frequently brought the country to a standstill with strikes and protests during negotiations over wages and working conditions, thus constraining the ANC's ability to pass economic reform measures that are unpopular with unions.

- Roughly one-third (33%) of working-age South Africans are unemployed, and more than half of the population (55%) is estimated to be living in poverty. South Africa also has some of the highest levels of income equality in the world, with the World Bank estimating that only 10% of the population owns over 80% of the country's wealth.

- According to current opinion polls, the ANC will receive around 45% of the vote in the 2024 general election, down from 57% in the 2019 general election and 62% in the 2014 general election.

- The ANC is highly factionalized, with President Cyril Ramaphosa's faction favoring pro-business structural reforms and the opposing Radical Economic Transformation (RET) faction demanding populist, economic redistribution policies. Ramaphosa's faction currently holds five of the top seven seats in party leadership and has been able to push through some reforms to the power sector, but lacks the political or popular support necessary to implement sweeping economic reforms.

Even if the ANC is forced into coalition governance following the 2024 general election, a drastic change in economic policy is unlikely, which means that South Africa's economic stagnation will likely persist for at least the next six years. While the ANC remains the party with the most national support ahead of the 2024 general elections, it could still be forced into coalition government if it does not meet the 50% support threshold in parliament. The ANC does not have any natural allies in opposition parties, and any potential partnership is made more difficult by factionalism within the party. Against this backdrop, the Economic Freedom Fighters (EFF), a populist party that advocates for Black economic empowerment and redistributive land policies, could be the most viable option for coalition governance (particularly for the populist RET faction of the ANC). But an EFF-ANC partnership would also very likely push the government even further away from fiscally restraining structural reforms. This means South African economic policy will likely remain stagnant through the next presidential term (which ends in 2029), portending at least six more years of capital flight, low growth, failing infrastructure, heightened unemployment and increased socioeconomic inequality.

- Continued economic stagnation and failure to implement economic reform mean that South Africa's public debt problem will likely worsen in the coming years — further limiting fiscal space to address social spending needs, take on more debt of failing state-owned companies and cope with unexpected shocks, like extreme weather and climate events.