In France, another political crisis suggests that neither the current nor a new government is likely to implement forceful measures to curb fiscal vulnerabilities, which will increase the risk of financial instability, reduce domestic investment and weigh on France's other financial commitments in the coming years. On Sept. 8, Prime Minister Francois Bayrou will face a confidence vote, which he is expected to lose, as his minority government struggles to gain sufficient legislative support for its 2026 budget that includes 44 billion euros ($51 billion) in cuts and other controversial measures, including scrapping two public holidays. Faced with a continued increase in government debt, which exceeds 100% of GDP, successive French governments, depending on the support of an increasingly fragmented and polarized legislature, have failed to implement significant fiscal adjustment. Michel Barnier was ousted as prime minister in December 2024 after trying to push through spending cuts using a constitutional provision that allows legislation to be passed without a vote, while also allowing opposition parties to table no-confidence motions in the government. His successor, Bayrou, then managed to pass a budget in 2025 using the same mechanism after the Socialist Party abstained, but only after surviving two other no-confidence votes and promising concessions to the Socialists. Due to political opposition, the budget targeted fewer savings and focused on (economically less effective) tax increases rather than spending cuts. Several measures were also of a temporary nature, thus limiting their financial impact and leaving France with growing fiscal risks.

- On Sept. 4, Socialist Party leader Olivier Faure confirmed that his party would vote to bring down Bayrou's government during the confidence vote, all but ensuring that it will fall.

- Snap legislative elections in 2024 translated into a three-way parliamentary split. The left-wing New Popular Front (NFP), which is a multi-party coalition, won 182 seats, the centrist Ensemble 168 seats and the far-right National Rally (RN) 143 seats. Since President Emmanuel Macron was elected in 2017, France has had six prime ministers.

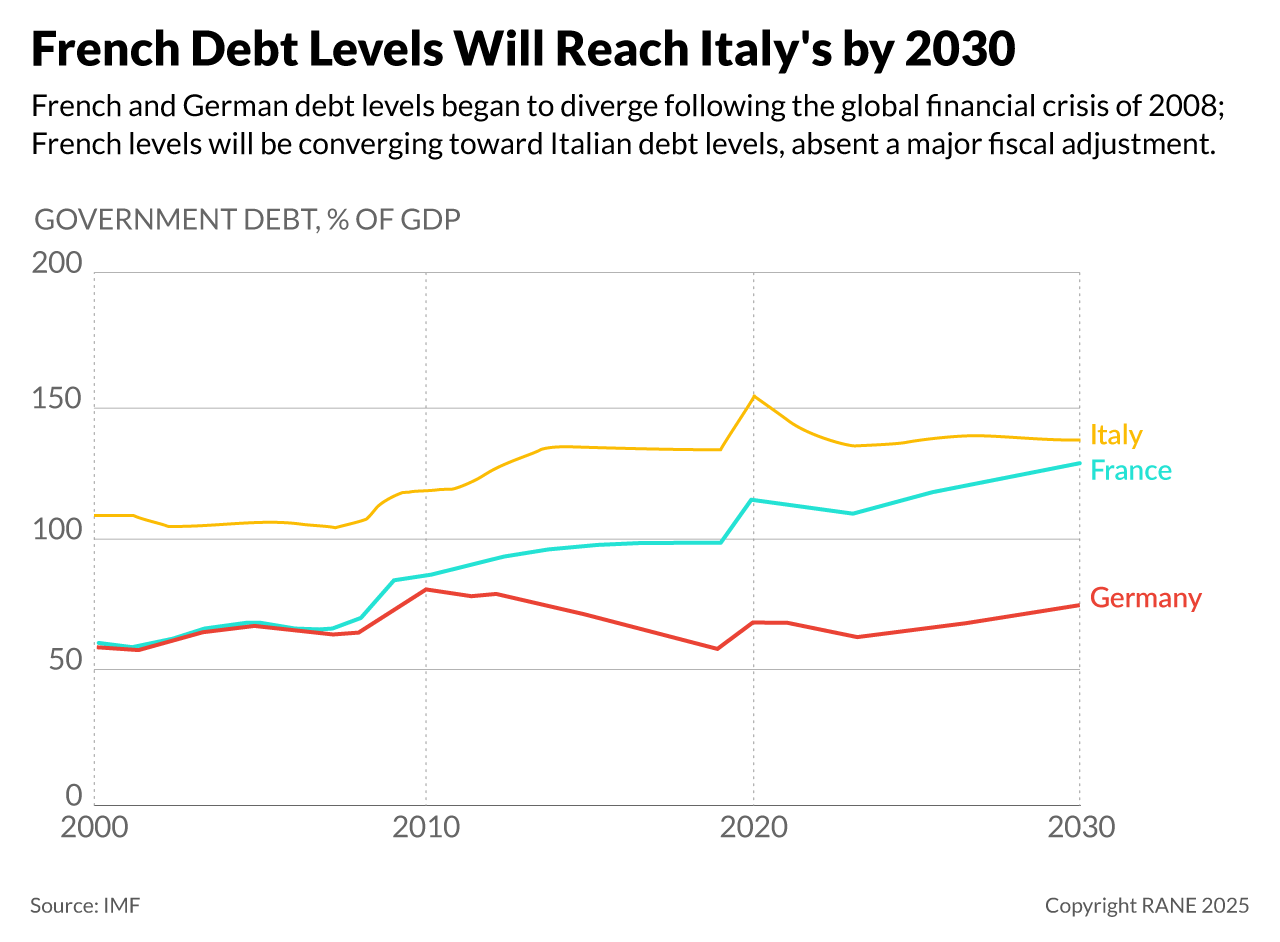

- Government debt stood at 113% of GDP in 2024, compared to a euro area average of 88%, making France the euro area member with the third-highest debt ratio after Greece at 151% and Italy at 135%. By comparison, German government debt amounted to 64% of GDP. The fiscal deficit reached 5.8% of GDP in 2024, compared to a euro area average of 3.1%.

Against the backdrop of increasing government debt and insufficient policies to reduce the fiscal deficit substantially, France is in a difficult fiscal position, but parliamentary gridlock makes fiscal consolidation more difficult. Yields on French government bonds have increased and now trade at their highest levels since the 2011 eurozone crisis, near those of highly indebted Italy, long seen as the eurozone's benchmark for high-risk debt. Yields on long-term government debt are a function of investors' perception of the sustainability of government debt and, hence, concomitant fiscal policy. Current spreads suggest that investors harbor some concerns about the outlook for French debt but continue to give Paris the benefit of the doubt in terms of a broader, sustainable fiscal adjustment down the line. But the political obstacles to a decisive adjustment remain nonetheless significant. In addition to a fragmented parliament where neither of the three blocs commands a majority, a significant reduction of the fiscal deficit will not get approved. France's tax burden is already among the highest in Europe, and expenditure is set to continue to increase, absent expenditure reform. A significant share of expenditure-based adjustment would need to come from cuts to social welfare. But this would be deeply unpopular. Most political parties are unlikely to support significant reform ahead of the 2027 presidential election and potentially another early parliamentary election, given the current political gridlock. The short- to medium-term outlook for significant fiscal consolidation is therefore dim, which explains why markets price French debt the way they do. But yield spreads at current levels also suggest that investors are not overly worried about the government encountering significant financial distress that could trigger a larger debt crisis.

- Ten-year French government bond yields sit around 3.4%. French yield spreads over German bonds are just below 70 basis points, compared to just over 70 basis points for Italian bonds. This suggests that investors deem the probability of a French debt default comparable to an Italian default.

- France's total financing requirements for 2025 are 300 billion euros, or less than 10% of GDP. Most of it will be financed by way of medium- and long-term bonds. This means that an increase in long-term interest rates will not immediately translate into a significant increase in interest payments and higher fiscal deficits, somewhat limiting the possibility of a liquidity-fueled debt crisis.

- French government expenditure exceeds 57% of GDP, compared to a euro area average of 50%. Government revenue accounts for 51% of GDP, compared to 47% in the euro area.

- France's sovereign credit rating is AA- (or its equivalent) by international credit rating agencies, Fitch, Moody's and Standard & Poor's.

- The IMF projects real GDP growth of around 1.2% annually in 2025-2030. However, this may be too optimistic, given the need for fiscal consolidation.

Absent much greater market pressure, decisive fiscal action to significantly reduce fiscal deficits will remain elusive before and likely after the next presidential election, given political fragmentation and polarization that will prevent a stable legislative majority able to pass strong economic reforms and implement fiscal consolidation. Fiscal priorities among the left and the centrist parties supporting the government do not align, forcing weak prime ministers to resort to constitutional prerogatives to push through modest and often temporary fiscal savings. But even these prerogatives are not always sufficient to pass a budget, let alone a budget that generates significant savings, nor gives markets a measure of predictability. Macron could call an early parliamentary election, though it would likely result in another fragmented legislature and fail to break the logjam. Meanwhile, popular opposition to social welfare cuts and tax hikes led by increasingly popular far-right and far-left parties remains strong, as widespread demonstrations against such moves in recent years have demonstrated. This will continue to limit political space and legislative support to pursue an expenditure-based fiscal adjustment in the near term, and particularly so in view of the 2027 presidential election. It would require a significant increase in market pressure in the guise of significantly higher long-term bond yields, sustained over several months, for the political incentives to push through major budgetary reform. But for the foreseeable future, market pressure will remain modest. The rate at which the debt ratio is projected to increase in the next few years is not fast enough for bond yields to reach sufficiently high levels that would make it difficult for the government to issue debt.

- The government benefits from significant constitutional prerogatives when it comes to fiscal policy, but disagreement among the parties supporting the government has made it difficult to pass budgets with significant cost savings. If parliament does not approve the government-proposed budget within 70 days of its submission to parliament, the government can take advantage of an expedited procedure and invoke Article 49.3 of the constitution to force the budget through without a legislative vote. However, this then allows parliament to go for a no-confidence vote and topple the government. Article 40 of the constitution restricts the ability of the legislature to propose amendments that would lead to a reduction in the government's expected income, nor amendments that would increase the government's spending obligations. The government, by contrast, can make adjustments of up to 2% of spending and revenue, once the budget is approved.

- In a field of potential candidates for the next presidential election, far-right RN leader Jordan Bardella leads the polls with 30% support, far ahead of centrist former Prime Minister Edouard Phillipe and left-wing potential candidate Jean-Luc Mélenchon. Both centrist and leftist parties currently supporting the government will be reluctant to pass reform or budgets that include significant welfare spending cuts.

- The IMF forecasts a modest decline of the deficit to 5.5% of GDP in 2025 before staying close to 6% of GDP until the end of the decade, barring significant fiscal adjustment. On the current fiscal trajectory, the debt-to-GDP ratio will reach 128% of GDP by 2030, up from 113% of GDP in 2024.

Increasing financial vulnerability and pressure to implement budgetary reform will weigh on France's military commitments, priorities in the European Union and broader fiscal flexibility. Among other things, budget constraints will limit the amount of military, financial and humanitarian support France will be able to provide to Ukraine. Moreover, fiscal profligacy will make French-supported proposals to increase common EU expenditure less credible, particularly in the eyes of low-debt countries like Germany and the Netherlands. Furthermore, a sustained increase in investor risk aversion would force the French government to focus on sorting out its financial situation, but this is likely to jeopardize government stability and take several years to accomplish, in the meantime, constraining France's financial flexibility. Finally, in the context of increasing defense expenditure, including commitments made within NATO to raise defense and related expenditure to 5% of GDP by 2035, and reduced fiscal space in the event of a renewed exogenous shock, such as another global financial crisis, will constrain the government's fiscal flexibility to respond.

- France has one of the highest social welfare expenditure ratios as a share of GDP in the world. Public expenditure on social welfare exceeds 30% of GDP. Within the EU, only Austria and Finland spend more on social welfare. Pension spending in France is around 14% of GDP, the third-highest level within the bloc after Greece and Italy. The OECD average is 9% of GDP and the EU average 11%.

- Despite strong rhetorical support for Ukraine, France has offered relatively limited support to Kyiv compared to other European countries. France has provided 0.3% of its GDP worth of bilateral aid, compared to Denmark's 2.9% and Germany's 0.6%. In dollar terms, France is only the tenth-largest donor and has provided less support than smaller economies, such as Sweden, the Netherlands, Denmark and Canada.