Pedestrians walk past a board at a currency exchange office in Moscow, Russia, on Jan. 16, 2023.

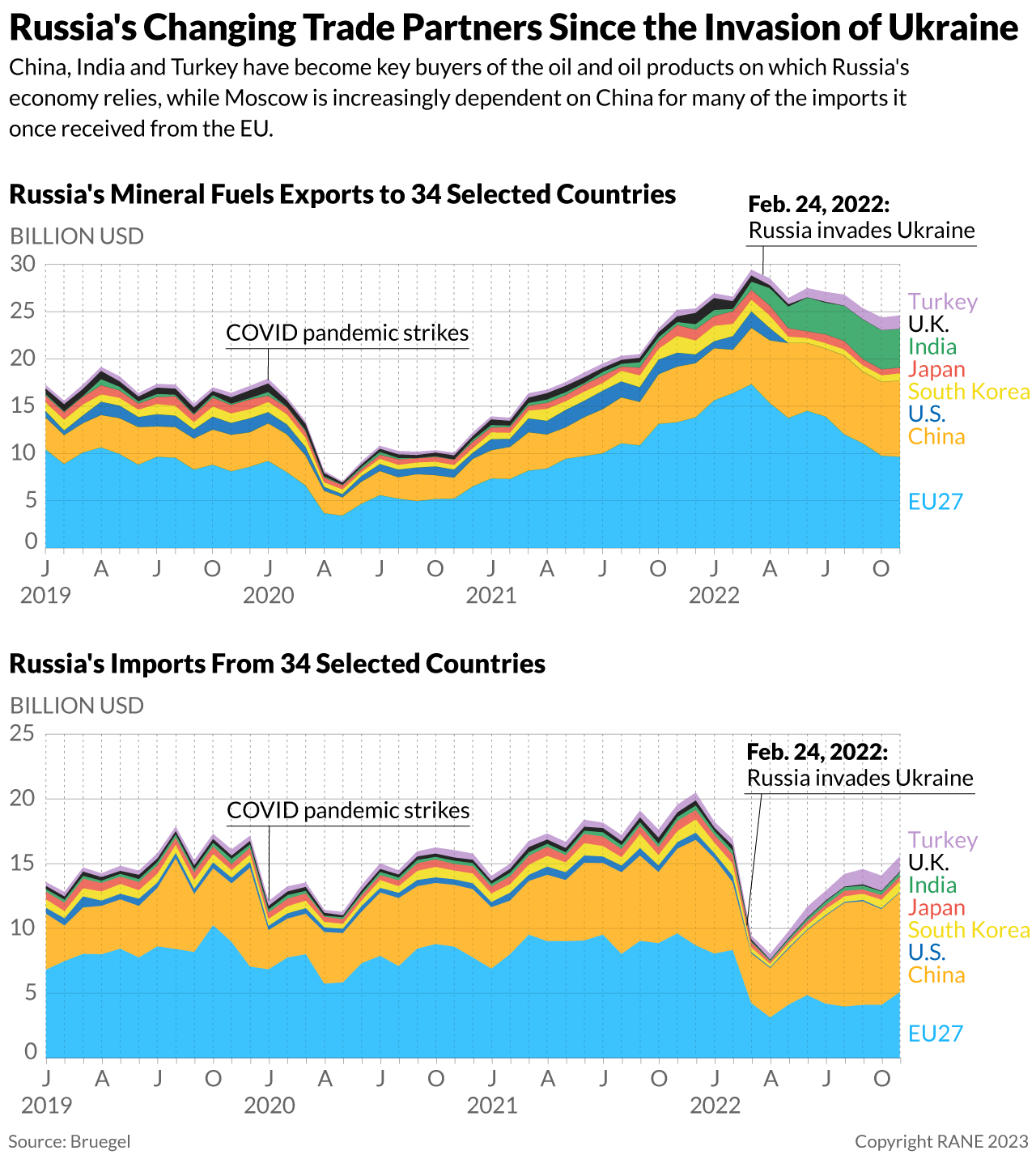

Russia's economic struggles are unlikely to alone force political change or de-escalation in Ukraine in the coming year. But medium-term challenges and the country's bleak structural outlook will undermine President Vladimir Putin's authority and complicate Russia's war efforts in Ukraine. A year after launching its war in Ukraine, Russia's economic outlook is bleak, but the risk of an acute crisis remains low. However, Russia's economic situation will likely worsen on Feb. 5, which is when the G-7's price cap on Russia's refined fuel sales will enter force, complementing the price cap on Russian crude that's been in place since Dec. 5. Moscow will likely continue to conceal and manipulate its economic data to avoid panic, which it has done since the start of the Ukraine invasion. But Russia's economy is slated to further contract in 2023 amid falling global prices for oil and gas, which have in recent years constituted approximately 20% of the country's GDP, 60% of its exports and 40% of its government's budget. The impact of Western sanctions and the G-7 price caps is also forcing Russia to sell its hydrocarbon exports at significantly discounted prices, further eating into the country's energy revenues. Russia's primary export-grade crudes, for example, are currently selling at about $40-$45 a barrel, amounting to a 50% discount compared with Brent crude (which is currently about $88 a barrel).

- On Dec. 27, Russian First Deputy Prime Minister Andrey Belousov said the government expected Russian GDP to decline by 1% in 2023. Russia's Economic Development Ministry forecasts a decline of 0.8%, while Russia's central bank forecasts a fall of 2.1%. Such forecasts still tend to be more optimistic than those from outside analysts. The International Monetary fund expects Russia's economy to contract by 3% in 2023, while a Bloomberg poll of economists from December estimates a 2.5% contraction. The chief economist of Alfa Bank, Russia's largest private commercial bank, forecasts a 6.5% contraction next year amid Russia's falling consumer demand, lower investment and loss of export potential.

- Russia's economic contraction in 2022 would have been much larger if not for high global commodity prices (many of which Russia exports) in the months following the invasion. Oil prices this year are unlikely to compensate for Russia's falling oil and gas production in 2023 amid Moscow's inability to supply buyers amid a lack of tankers and sanctions. However, China's reopening amid the easing of COVID-19 restrictions and better-than-expected Western economic data will significantly support Moscow. The International Energy Agency estimates Russian oil production in 2023 to fall around 1.6 million barrels per day (bpd) from its pre-war levels, to 9.7 million bpd. Russia's own 2023 budget projects a 23% fall in all oil and gas revenues compared with 2022.

- On Jan. 11, Russian President Vladimir Putin ordered Deputy Prime Minister and former Energy Minister Alexander Novak to figure out how to prevent the high discounts at which Russian oil is currently being sold on global markets from creating problems for the Russian budget. Russia will soon be forced to offer discounts for its refined products (like diesel) as well. Such price slashes could be even steeper since tanker capacity for Russian refined products is more strained than it is for crude oil, which could force Russia to reduce domestic refining and sell more of its oil as crude. Russia's dependence on a small number of large buyers for its oil, namely China and India, will continue to give those states immense bargaining power over Moscow.

While Russia's economy will continue contracting and its budget deficit will grow, lower inflation and historically low unemployment levels will mitigate economic and political risks for Moscow in the short term. As in 2022, Russia's 2023 economic contraction will probably not significantly undermine political support for Putin, or lead to military production shortfalls that meaningfully affect Russia's ability to continue waging its war in Ukraine. This is largely due to Russia's low unemployment rate, which currently stands at 3.7% (this does not include military personnel, who are considered employed), with only 2.7 million Russians unemployed. With Russia experiencing a labor shortage, workers in the country now face less competition and feel empowered to seek high wages, often found in armaments industries. While this will fuel inflation, Russia will likely keep domestic consumer prices at acceptable levels in 2023; in fact, there are reports the Russian government is concerned about inflation being too low and thereby contributing to the country's demand stagnation. Russia's 2023 federal budget deficit is likely to far exceed the 2% of GDP forecast by the government (which was based on Russian oil selling at around $70 per barrel — well above the $40-$45 a barrel Russia is currently receiving). But Russia's growing deficit is unlikely to precipitate significant near-term economic repercussions for Moscow. This is because prior to the Ukraine invasion, Russia maintained one of the lowest debt-to-GDP ratios in the world among major economies at under 17%, and still has a substantial National Wealth Fund with which to plug the deficit.

- Price growth in Russia has been significantly below 3% since September, below the Russian Economic Development ministry's 5.5% target and the Central Bank's 5-7% goal. Russian officials are worried that too slow of price growth will fuel mid- to long-term problems, including reduced output, increased unemployment and falling incomes.

- The head of Russia's central bank, Elvira Nabiullina, has indicated that Russia's widening budget deficit could mean high inflation and, subsequently, prompt higher interest rates that further choke off the prospect of economic growth. But this does not pose an acute threat to Moscow's finances for two reasons. For one, the Russian government can borrow internally, having successfully issued three federal loan bonds on Nov. 23 that raised a total of 1.44 trillion rubles, or about $21 billion (the main buyers of these bonds were large domestic banks that borrowed the record sum of rubles from Russia's central bank through repo transactions, and this has so far not caused a significant increase in inflation). And secondly, Moscow can also continue to sell off assets from its sovereign wealth fund such as Chinese currency — the liquid portion of which, at current rates, would not be exhausted until 2025.

In the medium term, Russia's attempt to create a semi-autarkic economy will translate to declining living standards and greater difficulties in growing the country's defense production. But these impacts are unlikely to alone cause the political change or weapon shortages needed to end the war in Ukraine. Russia's most pressing medium-term economic challenge stems from its failure to replace key imports from the West, many of which are currently targeted by Western sanctions. The value of Russian imports has fallen by roughly 25% since the start of the war, and almost all sectors of Russia's economy relied on imported goods in some capacity prior to the invasion. Russia's import dependence extends to consumer products and industrial components, which have helped raise the standard of living in the country over the past 20 years. But more importantly, Russia remains highly reliant on imports of high-tech components and critical materials for military production. Russia cannot, for example, build sufficient semiconductors and other electronics for its military production, let alone its overall domestic needs. Furthermore, since 2014, Russia established import substitution budgets intended to at least give it a head start on replacing key products and goods following the post-invasion collapse of imports. But the program has been widely seen as a near-total failure, as Russia neglected to establish domestic production for key machinery and technology, and is also still years away from doing so for key industries — leaving the country almost completely dependent on China for imports. But luckily for Russia, Western sanctions are leaky, enabling Russia's intelligence services to continue their long history of acquiring sanctioned goods and technology covertly. Russia can also secure many consumer goods and some key equipment through gray import schemes via China, Kazakhstan and Turkey. These two factors will mitigate the impact of Russia's failure to establish domestic production for the foreseeable future.

- In 2014, the Russian government introduced an import substitution program that provides subsidies to businesses creating analogs for critical technologies and components previously purchased from the West. But in May 2022, influential Russian senator Andrey Klishas acknowledged that the program had 'completely failed' and that now the government's only real plan was to 'transplant our industry, and with it our economy, to a new, now Chinese, needle.'

- Russia's history of stealing electronic and other technology from the West dates back to the Soviet era and earlier. The country's recent success in these efforts is evident in public reports detailing Western components illegally present in Russian military hardware. An August 2022 report by the U.K.'s Royal United Services Institute identified 450 unique microelectronic components of Western manufacture, most of which were subject to export controls, in 27 Russian weapons systems recovered in Ukraine.

In the long term, structural economic issues — including Russia's demographic decline, dependency on energy exports, and inability to attract investments — will severely restrain the country's growth potential, which could eventually threaten the war's popularity in Russia and the government's capacity to continue it. Moscow will not indefinitely be able to finance its deficit internally with monetary intervention, nor will it be able to replace its imports with domestically made substitutes in an economically viable manner in the coming decade. Many years down the line, medium-term challenges may leave the government unequipped to prevent a more substantial economic crisis in Russia, as the rents needed to make the investments to end its oil and energy export dependency are falling because Russia's average cost of production per barrel rises due to the lack of Western tech. Russia is also not making those investments anyway amid its contracting economy and use of budgetary resources on the war. Should Russia's export revenues from commodities continue to fall, this could eventually instigate a balance-of-payments crisis in Russia in which foreign investors would not intervene to bail out Russia. In the wake of such a crisis, even investors from friendly countries to Moscow would largely withdraw their capital, though China would likely preemptively intervene and finance Russia to prevent such an outcome. In any case, adding to Russia's gloomy outlook are additional structural factors, including a worsening demographic outlook amid ongoing mobilization that will exacerbate labor shortages. Growing state intervention in the Russian economy (which was already very high before the invasion) will also further limit Russia's productivity and growth potential as once-productive, private areas of the economy increasingly fall under government control. In all, low domestic savings and investment rates driven by stagnant GDP will put an even greater burden on the Russian government to prop up the economy — an increasingly politically risky and difficult task amid the need to simultaneously procure resources and manpower for the war in Ukraine.

Russia's stagnant economy won't make Russia's foreign policy more adventurous and will not have a major political impact in the near term. It will, however, discourage foreign investment and somewhat empower political reformists, though they are still unlikely to secure power should Putin leave office. Russia's struggling economy is unlikely to lead to major changes in the country's foreign policy, which has already become more aggressive since the invasion of Ukraine. Russia's foreign policy is unlikely to become significantly more hawkish, given the country's high losses of men and materials in Ukraine. The only serious potential target for such aggression, Kazakhstan, will also maintain its ties with Moscow and is closing its eyes on gray import schemes through its territory, aiding Russia. Still, struggles to attract significant new foreign investment — even from countries friendly to Russia — will cast doubt on the effectiveness of Moscow's foreign policy course. This will slightly empower reformers in Russia calling for reductions in tensions with the West and de-escalation of the war in Ukraine in order to begin restoring Russia's previous role in the global economy. But for now, there is little reason to believe that such economic arguments would prevail over more hawkish views calling for the continuation and escalation of the war in Ukraine in the still unlikely event that Putin suddenly leaves office.