Russian President Vladimir Putin on May 18 at the Congress of the Russian Union of Industrialists and Entrepreneurs in Moscow.

Governments must spend immense resources to sustain large-scale war, and Russia is no exception. Since its 2022 invasion of Ukraine, Russia has poured vast reserves of funding, equipment and manpower alike into its war effort, and its economy bears the wounds to prove it, made worse by mounting Western sanctions. However, a largely qualitative analysis of Russia's economy suggests that Moscow could continue its war with Ukraine at current levels of intensity for at least another two to three years under current economic constraints. This extended timeline may reduce the Russian government's incentive to negotiate a political settlement as long as Western support for Ukraine does not force Moscow to dig significantly deeper into its dwindling resources.

However, continued war would come with significant short- and long-term economic costs for Russia, despite the temporary boost in economic growth following Moscow's sharp increase in defense expenditure. Domestic demand already outstrips the Russian economy's production capacity, as reflected in high — and likely underreported — inflation. While rising inflation will not prevent Russia from maintaining high defense expenditure over the next few years, it will risk raising domestic political discontent in the medium term and sinking long-term economic growth.

In short, Russia's short-term economic constraints are manageable, which will limit incentives to make significant concessions in peace negotiations. However, the economic costs of maintaining the war will increase over time and weaken Russia's economic position further, which could eventually constrain the government's domestic political ability to pursue the war. As a result, Russia's calculus in peace negotiations may shift over the next several years, particularly if Western support for Ukraine increases.

Financing the War Effort

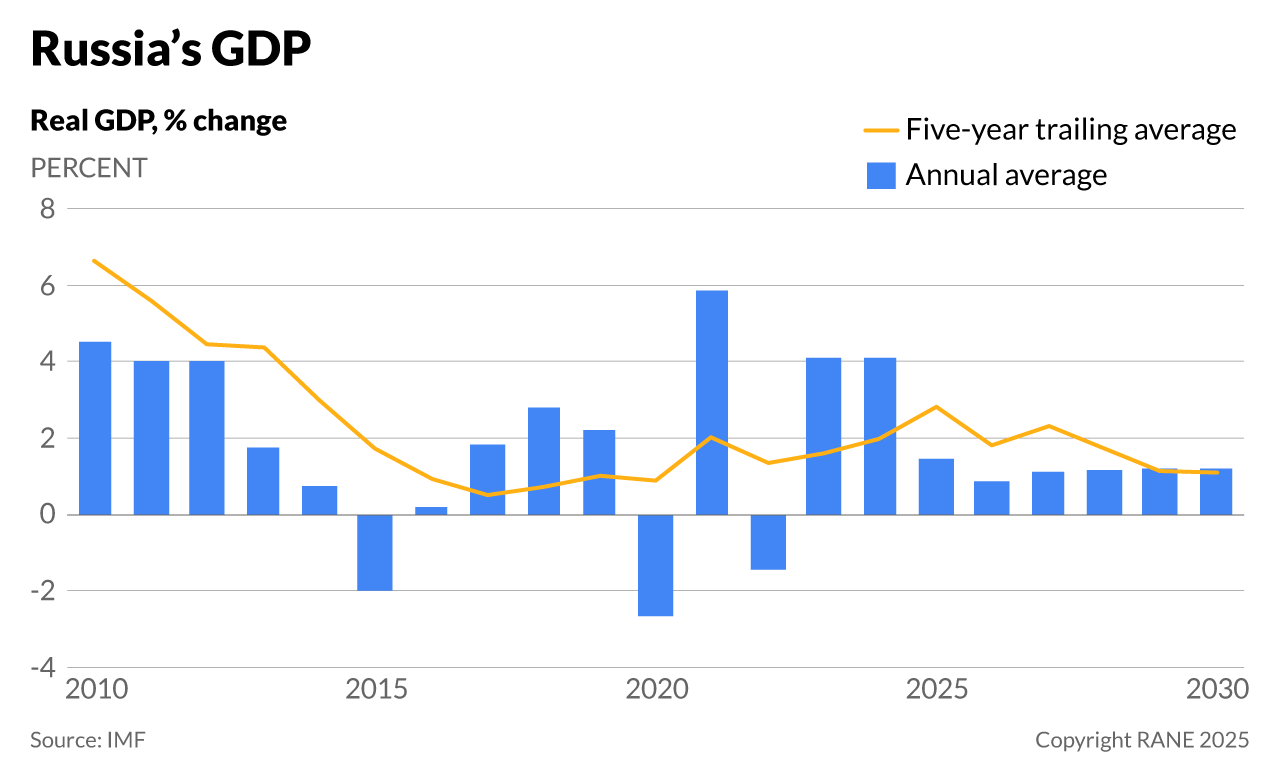

The status of the Russian economy is difficult to assess due to limited data availability or its poor quality. However, based on official figures, Russia's economic growth appears to have accelerated to 4% in 2023-24 after the economy shrank in 2022. While this growth appears to be a positive sign for Russia at first glance, it was largely attributable to Moscow's significant increase in defense spending, which will prove unsustainable over the longer term. Similarly, while government debt appears to have remained very low in 2023-24 (the International Monetary Fund estimates it at 20% of GDP), high inflation still points to tightening economic constraints as domestic demand, including defense spending, outpaces domestic production. Unable to borrow internationally, Russia will increasingly struggle to circumvent this constraint, regardless of its level of government debt. The next paragraphs discuss the financial aspects of Russia's war economy and suggest that primarily non-financial constraints will increasingly weigh on the economic outlook.

In terms of government finances, increased expenditure on personnel, materiel and operations can be sustained through higher taxes, lower non-defense spending, greater debt financing or the drawdown of the government's financial resources. While reliable data are not available, there is no doubt that Russia's defense expenditure has increased far more rapidly than non-defense expenditure since 2022. Governments can also finance increased expenditure through direct central bank financing of the budget, which often leads to higher inflation (the so-called inflation tax). If the official statistics are to be believed, Russia has thus far resisted financing its war effort by taking on significant additional debt, instead relying on the drawdown of financial resources. It is noteworthy, however, that higher inflation, which averaged 8.4% in 2024, compared with around half that level in 2018-21, has also been instrumental in maintaining a low debt-to-GDP ratio, which is officially reported at 20% of GDP.

To the extent that a country's war effort relies on foreign resources, its economy must be able to acquire imports. Similarly to the domestic budgetary financing of the war effort, a government can draw down its existing foreign assets, export goods and services to generate revenue or raise foreign debt to finance imports. Since Russia cannot access its frozen foreign assets or raise debt internationally, Moscow cannot rely on net foreign resources to support its economy and must instead use export revenue to finance imports.

This is where sanctions enter the equation. In practice, Russia has been able to more or less successfully evade many trade-related sanctions by importing goods through third countries, outright smuggling, or sidestepping insurance-related sanctions by building out and operating a fleet of "shadow tankers". Nevertheless, Western sanctions have imposed material costs on the Russian economy, whether by increasing the costs of importing sanctioned goods or forcing Russia to accept lower prices for its oil exports due to price caps.

Freezing the Central Bank of Russia's foreign-exchange reserves reduces Russia's ability to finance imports. Meanwhile, financial sanctions prevent the Russian government from raising foreign debt, while foreign trade sanctions aim to limit Russia's ability to generate foreign-currency revenue. Relatedly, export controls are meant to deny Russia access to critical imports or at least force it to acquire them elsewhere at higher prices, assuming they are available elsewhere. More broadly, trade restriction also imposes what economists call deadweight losses on the economy, leading to overall economic losses, as the economy is forced to switch to more expensive goods internationally or more expensive sources domestically. Finally, its more limited ability to acquire critical technology due to export controls will also weigh on its long-term economic outlook regarding productivity growth.

Economic and Political-Economic Constraints on the War Effort

The war effort and sanctions will continue negatively to impact the Russian economy in the short and long term. While impossible to quantify, standard economic analysis suggests the effect will remain tangible and increase as the war continues. Economically, governments are almost always capable of mobilizing enormous resources to support a war effort. Politically, however, they may be or feel more constrained, as the greater the resource mobilization, the greater the relative reduction in household consumption. The Russian government may feel less constrained given the institutional centralization of power, the relatively effective stifling of domestic opposition to the war and virtually nonexistent institutional avenues for political actors, including voters, to influence government policy. Nevertheless, any wartime leader will seek to limit the economic costs if it can be helped so as not to undermine support for the war.

In the short term, increased defense spending can boost economic growth, provided the economy is operating at below capacity. This seems to have been the case in Russia in 2022, at least judging from the unemployment rate. The unemployment rate has halved from 2021 to 2025, falling from 4.8% to 2.5%. While conscription may explain part of the decline, anecdotal evidence suggests that increased domestic demand, supported by sharp increases in defense expenditure, have helped pull labor into the economy. The very low unemployment also indicates that the Russian economy is now operating at above capacity, which will limit economic growth by pulling idle resources into economic production, both labor and unused capital. At the same time, a very significant increase in defense spending reduces output available for household consumption or decreases domestic savings required to finance domestic investment. And reduced household consumption may weaken domestic support for the war. While certain types of workers may have benefited from increasing wages, particularly in the defense industry, people who rely on government support will likely have suffered a decline in real income as a consequence of increased inflation in the face of at best slow increases in government social and pension spending relative to (likely underreported) inflation. Moreover, reduced investment will weaken the medium- and long-term economic outlook.

In addition to the impact of higher defense expenditure on consumption and investment, land wars also remove nonnegligible amounts of labor from the economy, particularly in the face of significant battlefield losses. British intelligence estimates put Russian battlefield losses — killed and wounded — at nearly 1 million. This compares to a working-age population of about 100 million. Not counting emigration, this may have reduced Russia's male working population by 2%, going some way toward explaining the fall in unemployment. British intelligence also assesses that foreigners make up only a very small share of Russian army personnel, including losses. There are an estimated 10,000-12,000 Korean soldiers fighting in the Ukraine war, and Koreans represent by far the largest contingent of foreign fighters. If the potential decline of the active labor force is not offset by increasing the labor participation ratio (such as bringing on more women and pensioners) or by increasing hours worked per worker, the more limited availability of labor will weigh on the economic outlook. Meanwhile, more limited savings will weigh on domestic investment and on medium- to long-term economic growth.

The Long-Term Economic Consequences of the War

If financial data are taken at face value, the Russian government faces manageable near-term economic and financial constraints in terms of continuing to prosecute the war and replace manpower and equipment losses. The costs of the war in terms of forgone household consumption and diminished long-term growth would still, however, be real. Defense spending is estimated at 6%-7% of GDP today, but may well be higher. This may be unsustainable in the medium to long term. High inflation meanwhile suggests that domestic demand is running too high. Inflation in the three years before 2022 was less than 4%, while in 2024 it exceeded 8% (though many economists question the reliability of official inflation data). Supporting high defense expenditure weighs on domestic consumption. Over time, this may be less palatable for the Russian government in domestic political terms.

None of this means that Russia will not mobilize further resources for the war effort, such as reducing household consumption or increasing the labor participation ratio. As mentioned, the high degree of political centralization, the crackdown on domestic political dissent and very limited avenues for expressing public discontent insulate the Russian government somewhat. But it does indicate that increased defense spending and personnel losses do have a material cost to Russia's short-, medium- and long-term economic prospects. And this is before factoring in the welfare and productivity losses due to reduced international trade and more limited or more costly access to advanced foreign technology.

In the decade leading up to 2022, Russian real GDP growth averaged less than 1.5%. If sanctions and trade restrictions remain in place and Russia maintains defense expenditure of more than 6% of GDP, the economy is at risk of entering stagnation over the medium term. More optimistically, the International Monetary Fund is projecting real GDP growth of 1.1% in 2026-30. But a shrinking workforce, aging technology and stagnating to declining domestic investment mean the Russian economy will fare far worse over the next decade than over the past decade. This, in turn, will likely create domestic and strategic constraints for the Russian government, not least because its ability to increase defense expenditure significantly will be constrained politically and, at least in the longer term, economically.

In addition to the immediate fiscal costs of the war and the longer-term negative economic consequences in terms of trade and investment, the Russian government will incur potentially significant liabilities and future spending commitments in terms of veteran pensions, veteran health care and financial support for conquered territory, not to mention the long-term costs due to diminished economic cooperation with the West. On the flip side, if Russia retains economic control over parts of Ukraine, it will also have a larger tax and resource base to offset some of the longer term economic and financial costs, though they are highly unlikely to offset them completely. Finally, higher NATO defense expenditure — a direct consequence of Russia's war in Ukraine — will also represent a long-term cost to Russia in terms of the higher costs it wants to maintain its security by partially matching increasing Western defense spending. Finally, while a peace settlement that imposes substantial reparations on Russia is unlikely, it would increase the costs of the Ukraine war to Russia.

Economically, a government can almost always extract additional resources to support a war effort, at least in the short term, by reducing private consumption or domestic investment. A sharp reduction of private consumption may prove politically difficult, even if the Russian government is relatively well-positioned to fend off moderate criticism and opposition. A sharp reduction in investment will curtail the long-term sustainability of high defense expenditure. The latter would also weaken Russia, whose relative economic position is already relatively disadvantageous in terms of the size of its economic base. In terms of GDP, Russian defense expenditure is already more than three times the expenditure in European NATO countries, while the combined economic size of European NATO, let alone all NATO members, is far greater than that of Russia. On a nominal GDP basis, Russia's economy is about 1/15 of that of the United States, or about the size of Canada. On a purchasing power parity basis, Russia is 20% of European NATO members' GDP. Russia's already economically disadvantaged position plus continued high defense expenditures will lead to a further relative weakening of Russia's economic power.

What does all this mean for the short- and long-term economic and geopolitical outlook? The short-term economic constraints faced by Russia are manageable. But Russia's ability to significantly ramp up expenditure should — for example, the Western powers double down on military support for Ukraine — is limited in the sense that it would lead to higher inflation, reduced household consumption and, over time, increased domestic political consent. In the long term, the costs for Russia are high and will continue to increase in terms of manpower losses, reduced investment in the civilian economy, access to advanced foreign technology and access to foreign markets. While difficult to quantify, Russia's long-term economic outlook is very constrained. This means that Russia's incentives to make concessions at the negotiating table will be limited in the short to medium term, at least as long as there is no threat of the West doubling down on its support for Ukraine. As long as Ukraine is not defeated on the battlefield or collapses militarily, however, increasing costs of a continuation of the war for Russia will increase the incentives to bring it to an end. Whether this will lead the Russian government to adopt a more flexible approach is difficult to say. History shows that countries continue wars even though the economic and strategic costs exceed the expected benefits.