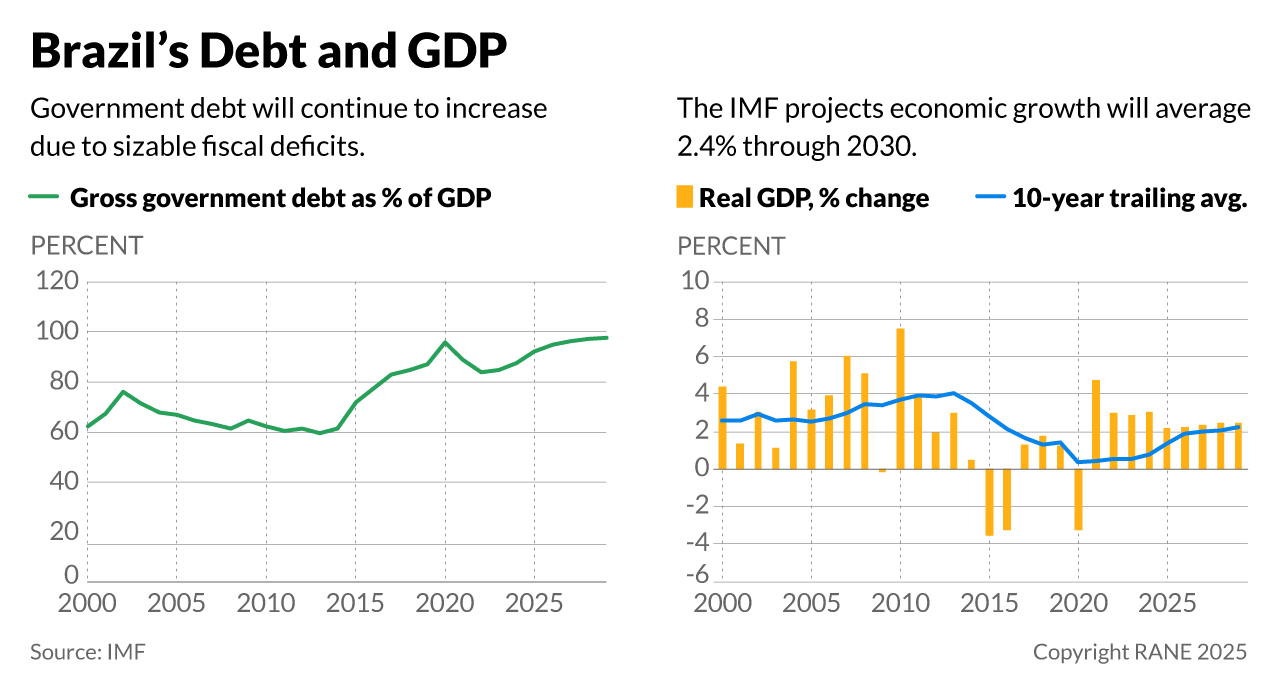

Brazil's current strong economic growth is unsustainable over the medium term due to continued low savings and investment and increasing uncertainty about the fiscal outlook, which will force the government to take more forceful adjustment measures in the next two to three years. According to the International Monetary Fund, Brazil's real gross domestic product grew by 3% in both 2022 and 2023, and real GDP is expected to have grown another 3% in 2024, marking an acceleration after over a decade of significant economic underperformance. This growth is supported by strong domestic consumption, increased agricultural and hydrocarbon output, and a pro-cyclical fiscal policy, which describes the government's tendency to increase spending (or reduce taxes) during periods of economic expansion. However, the IMF projects that Brazil's gross government debt will increase substantially from 85% of GDP in 2023 to 95% of GDP by 2027, and fiscal deficits are also high, amounting to 5-7% of GDP over the next few years. While Brazil's international financial position, commitment to a floating exchange rate regime and net foreign currency creditor position mitigate the risk of a debt crisis in the short to medium term, concerns about the outlook for long-term debt sustainability and economic growth are on the rise.

- The Brazilian public sector is a net foreign currency creditor, and less than 5% of Brazilian public debt is foreign currency-linked or -denominated. Brazil's international financing requirements are very manageable, and the central bank sits on $330 billion of foreign currency reserves, while the current account deficit is more than fully financed by net foreign direct investment flows. Neither external solvency nor liquidity is an issue.

- Additionally, Brazil's long-term economic growth is stronger than that of Latin America's other two largest economies, Argentina and Mexico. For instance, in the past thirty years, Argentina and Mexico registered real GDP growth of 2%, compared with Brazil's 2.4%. Over the past decade, however, Brazil's real GDP grew 0.5% annually, compared with Mexico's 1.5%, while Argentina's real GDP did not grow at all.

- These last few years of economic growth compare favorably to the era that followed Brazil's 2014 ''Car Wash'' corruption scandal that stymied investment and economic growth for years, as real GDP growth averaged a mere 0.5% per year over 2014-23. Even so, Brazil's current growth falls short of that registered during the 2000s, and according to the World Bank, Brazil's real GDP per capita has actually declined over the past decade.

While Brazil's international financial position is manageable, a modest medium-term growth outlook and adverse fiscal dynamics will eventually force the government to pursue a much more restrictive fiscal policy. In 2023, Brazil's National Congress reformed the country's fiscal framework to give the government greater leeway in terms of spending. Brasilia is struggling to take more decisive actions aimed at a fiscal adjustment in the short term to help stabilize the debt-to-GDP ratio. The government has also failed to address longer-term fiscal concerns related to constitutionally mandated high levels of education, health and pension spending, which will eventually prove unsustainable. As a result, a fiscal adjustment is necessary. If implemented forcefully, such an adjustment would help free up resources to be invested in the economy to raise medium-term growth. However, this is unlikely to happen on a meaningful scale in the near term, as the Lula government is already struggling to implement a short- and medium-term fiscal adjustment, and political constraints will only rise ahead of Brazil's October 2026 presidential election.

- In August 2023, Brazil replaced its 2016 constitutionally mandated spending cap with looser rules on government expenditure. The amendment reestablished floors for mandatory education, health and investment spending. While the reform committed the government to improving the primary balance (which describes the government's revenue minus its non-debt-related expenditures) from -0.5% of GDP in 2023 to 1% by 2026, the National Congress can change these targets with a simple majority vote. Meanwhile, mandatory spending increases mean the government is constantly striving to mobilize greater revenues.

- According to the Brazilian Institute of Geography and Statistics, Brazil's population of 216 million is projected to peak at 220 million in 2041 in the context of a rapidly falling fertility rate (down from 2.3 children per woman in 2000 to 1.6 in 2023, and projected to reach 1.4 by 2040). Additionally, the old-age dependency ratio, which describes the number of people aged 65 or older relative to the number of people of working age, increased from 10% in 2010 to 15% in 2023 and is projected to reach 36% by 2050. Brazil's working-age population is estimated to have peaked in 2021 as a share of the total population.

- Absent reform, public pension spending is projected to increase from 12% of GDP in 2016 to 16% in 2025 to 26% in 2050. This is not sustainable over the long term. Pension reform in 1998, 2003 and 2012 was insufficient to impact the upward path of future spending significantly. Adjusted for age, Brazil already has the highest pension expenditure in the world, according to the IMF.

In the coming years, political and legal constraints will limit the government's ability to implement necessary growth-accelerating structural reform, increasing the risk that debt becomes unsustainable. Brazilian presidents typically face an unwieldy National Congress in several ways. First, the president's party generally controls only a small share of seats in the Chamber of Deputies and the Senate, forcing the formation of coalitions that are ideologically and politically incoherent. Second, the number of congressional political parties and hence congressional fragmentation is high, which further weakens the cohesion of presidential coalitions and coherent, forward-looking policymaking. Third, party discipline in Brazil is very low, largely due to an electoral regime that weakens parties' control of candidates and favors personalistic policies. Fourth, recent changes to the way budget policy is implemented have further weakened the president's ability to win congressional support for a cohesive, long-term economic reform agenda, as it reduces the executive's ability to withhold approved funds to gain support for legislative proposals. Finally, many important economic reforms require amendments to the constitution, necessitating supermajorities that are difficult to achieve. If Brazil fails to implement major spending reform, particularly on pension and social spending, the country will eventually fail to comply with its new fiscal framework, and government debt will reach unsustainable levels. Over time, this trend will increase the pressure on Brazil's currency, inflation and nominal interest rates, and it will likely fuel tensions between the government (keen on keeping interest rates low) and the central bank (trying to achieve its inflation targets),which will further fuel financial uncertainty. Rising debt will also prevent the government from mobilizing the fiscal resources necessary to increase investment and support medium- to long-term economic growth.

- Consisting of 81 members, the Senate has 11 different political parties and groups. This high degree of fragmentation leads to the formation of fragmented and incoherent ''presidential coalitions,'' and the current coalition consists of a mere 42 senators. Consisting of 513 members, the Chamber of Deputies has 16 different parties and political groups. The government coalition falls short of an absolute majority with 225 deputies, requiring wide-ranging compromise with independents or the opposition to pass legislation.

- Members of the Chamber of Deputies are elected based on open-list proportional representation, which gives voters extensive influence over whom they elect and weakens party control over candidates, leading to personalistic and clientelist politics. This representation system has led to the creation of the so-called Centrao grouping among broadly centrist lawmakers in the National Congress who lack ideological conviction or cohesion and engage in clientelist politics. Meanwhile, senators are elected based on a plurality regime. However, due to weak national political parties and the senatorial candidates' reliance on state governments and governors (and their political machines) to be elected, they are similarly independent of the parties they represent.

- The Brazilian Constitution established extensive social and economic rights for citizens that require constitutional majorities to be amended. Constitutional reform is possible, particularly as far as it concerns minor issues, but it is generally politically challenging due to the need for a three-fifths supermajority in both highly divided chambers.

Brazil's medium-term outlook remains challenging, not least because sooner or later the country will need to overhaul its public finances. Over the medium term, the government will need to implement a more forceful fiscal adjustment to prevent a continuous increase in government debt, not least given large and increasing social and pension obligations. Politically, radical changes to pension and healthcare spending are very unpopular, as they affect ''acquired rights,'' which, if reform does take place, often are grandfathered. Against this backdrop, reform progress will likely be slow and gradual, particularly given the low likelihood of an external financial crisis. Economically and financially, the short-term effects of reform will also be limited because such changes typically seek to prevent a further rise in pension spending, rather than a decline in a context where spending is set to increase due to demographic dynamics. Due to increased government-financed consumption and transfers, this also means Brazil will continue to be characterized by a low, and perhaps even falling, savings rate, which will constrain domestic investment, particularly in public infrastructure, and future economic growth. Other structural reforms, such as greater trade integration, may support higher growth in the medium term, but progress here will also be slow, as the international trade environment is set to worsen in the coming years amid U.S. President Donald Trump's push to impose sweeping tariffs, the recent Mercosur-EU deal notwithstanding. With major structural reform unlikely before the 2026 presidential election, Brazil's economic performance is thus likely peaking right now, and will probably start to deteriorate soon, cyclically and structurally. This will increase political and distributional conflict in the run-up and, particularly, in the aftermath of the 2026 presidential race, when the room for further increases in spending will have been exhausted, forcing the government to take corrective action in reducing real spending and perhaps in raising taxes.

- In terms of trade integration, defined as exports and imports of goods and services, Brazil ranks 184 out of 195 countries. Agricultural, fuel and mining products account for 75% of Brazil's total exports. China is the top purchaser of Brazilian goods, comprising 26% of the South American country's exports, followed by the European Union with 15% and the United States with 11%. The bulk (23%) of Brazil's imports also come from China, followed by the United States with 19% and the European Union with 16%.