Despite financial markets' recent turbulence, Brazil is unlikely to pursue a harsh fiscal adjustment in the coming months, meaning persistent investor concern over the country's debt trajectory will continue to undermine macroeconomic conditions and the business environment. Investors' growing concerns about Brazil's rising debt trajectory and President Luiz Inacio Lula da Silva's unwillingness to deliver robust spending cuts have resulted in a sharp depreciation of the country's financial assets in recent weeks. The U.S. dollar rose 7.2% against the Brazilian real between Nov. 26 and Dec. 30, while Brazil's main stock index, Ibovespa, dropped 7.4% over the same period. The volatility reflects, among other things, investors' concerns over the country's rising indebtedness and the government's lax fiscal discipline, as Lula has repeatedly defended social spending and public investments as means for economic growth and downplayed markets' criticism. In an effort to mitigate the financial turmoil, the Central Bank throughout December conducted its largest intervention in the currency market in 25 years. To tamp down on rising inflation, the bank also increased its key interest rate by one percentage point to 12.25% on Dec. 11, and indicated plans for at least two more hikes of the same size by March. But these measures have not eased market concerns, as evidenced by the Brazilian currency hitting a record low of 6.27 reals against the dollar on Dec. 18.

- Economists now expect the Central Bank's main interest rate to reach 14.75% by the end of 2025 (up from the 12.25% they forecasted in mid-November); they also expect Brazil's inflation rate to hit 4.96% by the end of next year (versus the 4.34% forecast in mid-November).

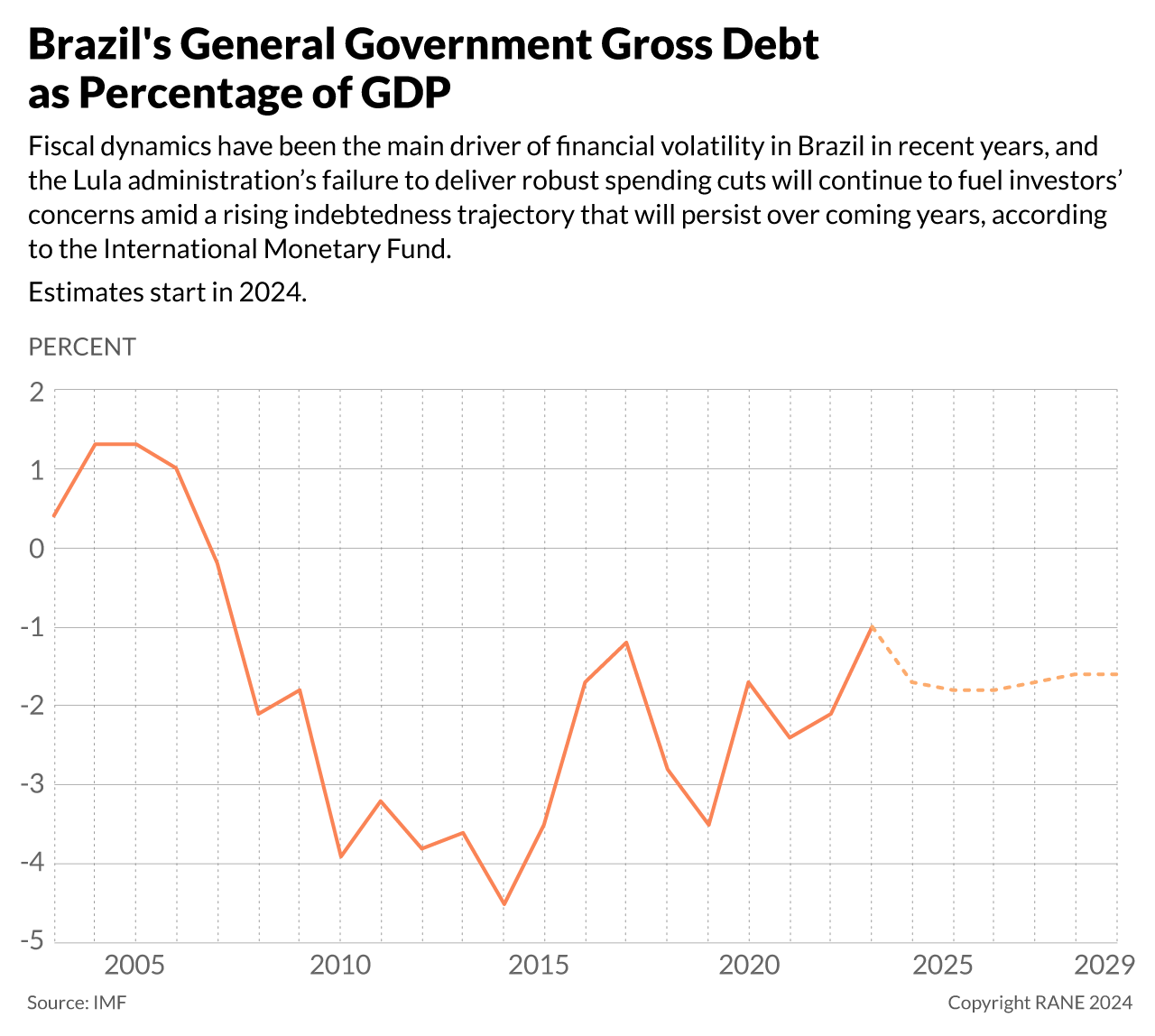

- The International Monetary Fund estimates that Brazil's general government gross debt will rise from 84.7% of GDP in 2023 to 97.6% in 2029.

- In a Dec. 15 television interview, Lula said that Brazil does not have a fiscal problem and that the country's current high interest rate levels were the only concerning aspect of the Brazilian economy.

- In 2023, the Lula administration introduced a fiscal framework aimed at improving the country's debt trajectory, but constitutional mandatory social spending has squeezed the discretionary budget and has made it harder for the government to comply with its self-imposed fiscal targets of zeroing the country's deficit in 2025. This has raised market concerns over the long-term sustainability of the framework.

Investors have expressed concern about Brazil's debt trajectory and commitment to fiscal discipline for years, but the situation started to escalate in November after the government presented a diluted spending cut package alongside a broad income tax break for the middle class. The sharp deterioration of the Brazilian currency comes amid a global appreciation of the U.S. dollar, as the U.S. Federal Reserve has indicated fewer interest rate cuts in 2025, which increases the attractiveness of U.S. assets and fuels the demand for dollars, thereby weakening other currencies around the world, especially ones in emerging markets (like Brazil). However, domestic drivers — including Brazil's rising debt trajectory and successive fiscal deficits over the past decade — have put more pressure on the Brazilian real by making investors worried the country's constitutional spending cap will become unsustainable in the coming years. The Lula administration, meanwhile, has done little to ease these market concerns, as its economic agenda until November had focused solely on increasing revenue collection to reduce the fiscal deficit while refraining from spending cuts. Against this backdrop, the real gradually depreciated throughout 2024, with a 25.8% drop year-to-date. But the situation significantly deteriorated on Nov. 27 after Finance Minister Fernando Haddad presented only limited spending cut measures, along with a tax break increase that took markets by surprise; although the latter was one of Lula's main campaign promises, investors did not expect him to follow through on the tax break at a time of heightened market concern over the country's need to reduce spending. In the days following Haddad's announcement, the Brazilian real plummeted to new lows, becoming the worst-performing currency in 2024 amongst 31 global currencies.

- On Nov. 27, Haddad announced a spending cut package that limits minimum wage gains, imposes stricter rules on public servants' wage caps, and restricts some social benefits to workers, elderly or disabled people; together, the measures are projected to save the government $71.8 billion reals ($11.6 billion) in two years. But the finance minister also announced plans to raise the income tax exemption threshold from those earning $2,824 reals ($456) per month to those making $5,000 reals ($807) per month beginning in 2026; the expanded tax break is expected to cost the government $35 billion reals ($5.6 billion) each year, which has fueled skepticism among investors about the Lula administration's actual commitment to fiscal discipline.

- Brazil's Congress on Dec. 20 approved most of the measures in the government's spending cut package; legislators have not set a date to start discussions on the proposal to expand the income tax exemption.

Although the government will likely announce more spending cut proposals in 2025, they are unlikely to eliminate investor skepticism; this portends further macroeconomic instability, though Brazil is unlikely to default on its debt. Lula has hinted at the possibility of additional spending cut measures in the months ahead. But given the president's ideologically driven political strategy of favoring social spending and public investment as means for economic growth over fiscal discipline, along with his confrontational rhetoric toward financial markets, it is unlikely that new proposals will be significant enough to ease investor concerns. More contradictory policy decisions — like the move to simultaneously announce spending cuts and tax breaks on Nov. 27 — are also likely, as Finance Minister Haddad's mostly orthodox economic policies will continue to clash with the leftist measures backed by Lula's Workers' Party. Such internal disputes, along with lawmakers' potential refusal to back the Lula administration's economic agenda, could further roil stock markets in the coming months by worsening policy uncertainty, thereby leaving businesses and investors in Brazil exposed to heightened financial volatility. The ongoing fiscal crisis may result in the Brazilian real remaining depreciated in the long term as well. While this would favor the country's grain and mineral exporters by making their goods more price-competitive, a weaker real would also fuel inflation and weigh on domestic industry by making it more expensive to import inputs. Meanwhile, higher interest rates will likely slow economic activity, hurting sectors reliant on domestic consumption like retail, construction, entertainment and tourism. This bleaker economic outlook may result in a negative credit outlook in the medium term. A default, however, remains highly unlikely because Brazil's debt is mostly denominated in local currency, and the country's $363 billion in foreign exchange reserves far exceeds its dollar-denominated liabilities.