As Pakistan strives to fulfill the requirements of the International Monetary Fund's loan program, financing assurances from external lenders and the implementation of an agricultural income tax will be key. On Jan. 7, Pakistan's Prime Minister Shahbaz Sharif announced that the United Arab Emirates had agreed to extend the deadline of a $2 billion debt payment originally due in January. This follows Saudi Arabia's decision to renew its $3 billion deposit with Pakistan's central bank on Dec. 5, 2024. These financial assurances solidify initial promises from Pakistan's external creditors that the IMF required before approving Pakistan's $7 billion Extended Fund Facility in September 2024, and they will be a critical part of the IMF's decision to release future tranches. The IMF will conduct its first review of the program in the first quarter of 2025 and, if approved, the program will continue to release funds in installments over 37 months. However, Pakistan has experienced some delays in acquiring assurances from creditors, including China, and other IMF requirements remain unmet. Islamabad must meet these requirements soon or risk delaying future IMF disbursements, which would exacerbate the country's financial crisis.

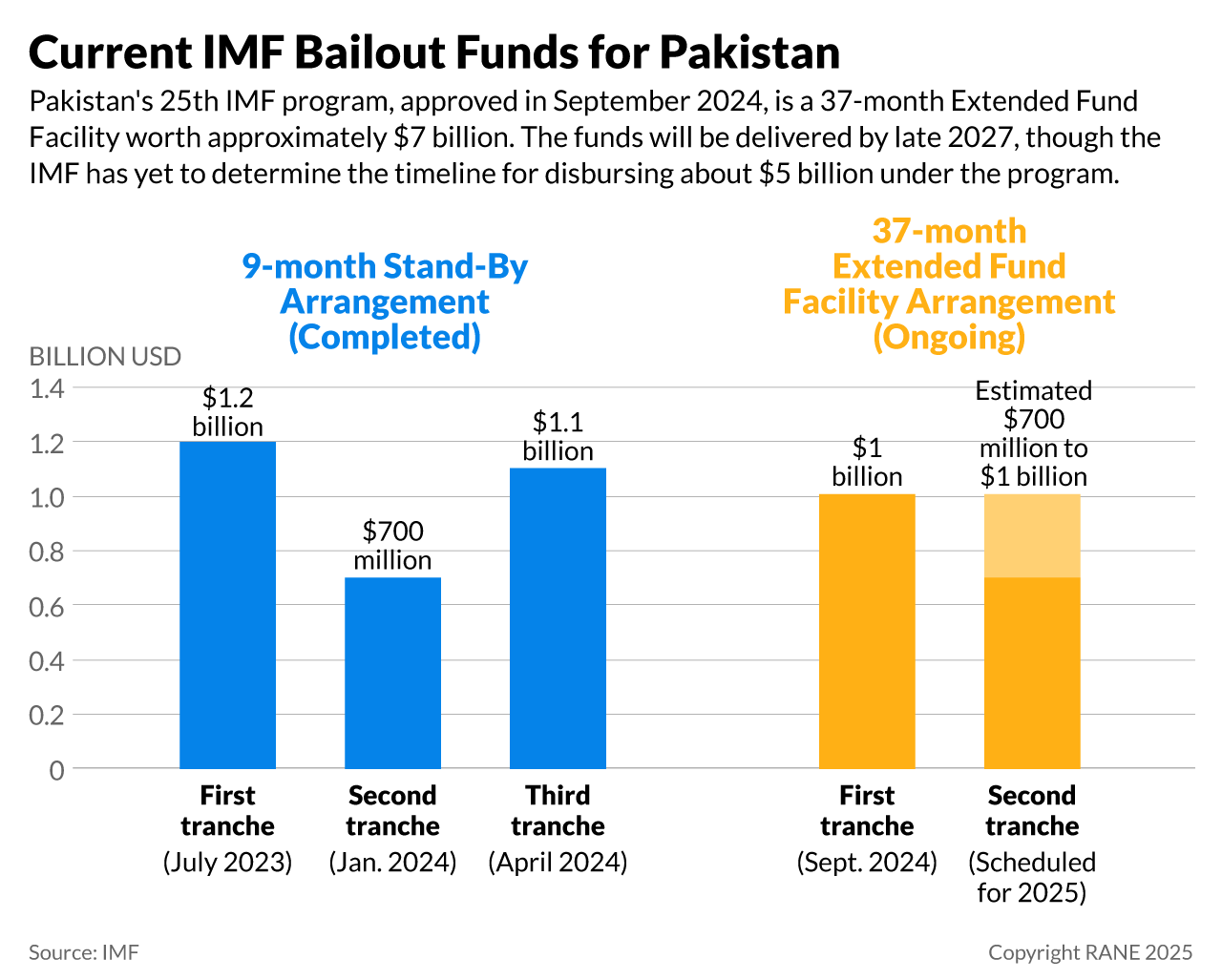

- The IMF's executive board approved the $7 billion Extended Fund Facility on Sept. 25 and delivered the first tranche of nearly $1.1 billion the same month after Pakistan reached a staff-level agreement with the IMF in July. The new loan marks Pakistan's 25th IMF program since its independence in 1947, the highest number obtained by any country.

- In the July staff-level agreement, Islamabad secured commitments for external financing through bilateral and multilateral lenders, including pledges to roll over loans from economic partners such as China, Saudi Arabia and the United Arab Emirates. The government obtained $16.8 billion in short-term financing rollovers, along with $2.1 billion in new commitments from these partners. However, the IMF has projected a $5 billion external financing gap for Pakistan in 2024-27, with $2.5 billion due in the current fiscal year ending June 30, 2025.

These financial assurances from the United Arab Emirates and Saudi Arabia follow an irregular IMF-Pakistan meeting on Nov. 12-15 in which IMF officials expressed concern about Pakistan's lack of progress under the program. At the meeting, IMF representatives emphasized Pakistan's financing shortfalls and delays in creditor commitments, as well as its failure to broaden its tax base and privatize state-owned enterprises. To address these issues, the IMF urged Pakistan to address its fiscal deficit, implement an agricultural income tax and continue privatizing Pakistan International Airlines. The meeting was unusual, as the IMF typically does not convene such discussions outside scheduled reviews, and it occurred against the backdrop of significant economic challenges in Pakistan, including a fiscal deficit driven by a revenue collection shortfall of nearly 190 billion rupees ($685 million) in the first quarter of the fiscal year, which is around 0.18% of the country's GDP.

- Under the IMF's structural benchmarks, the fund outlined recommendations to privatize loss-making state-owned enterprises, including Pakistan International Airlines. So far, Pakistan has met some benchmarks, such as removing restrictions on privatization by allowing the government to sell a significant portion of Pakistan International Airlines' shares and transfer management control to private investors, as well as privatizing 26% of the airline's shares by selling them to strategic investors. However, efforts have since stalled, and the IMF is concerned about Pakistan's bidder prequalification process and overall privatization strategy.

Pakistan will likely be able to address the IMF's concerns about delayed creditor commitments by bringing China on board, but Islamabad must still implement significant economic reforms to address structural issues. Given that China gave Pakistan financial assurances before the IMF program's approval in July, Beijing will likely eventually fulfill its commitment by rolling over its loan to Pakistan. However, any delays could hamper the IMF executive board's approval of the first program review. To expedite China's rollover, Pakistan could offer mutually beneficial economic incentives such as preferential access to key sectors like mining, energy and infrastructure development, as well as streamlined approval processes for Chinese investments under the China-Pakistan Economic Corridor. Once China agrees to roll over Pakistan's loan, Pakistan's balance of payments will improve and ensure sufficient funding over the IMF program period, providing Pakistan time to adjust economically and restore macroeconomic equilibrium. However, these measures will provide only temporary relief and will not resolve Pakistan's underlying structural issues, including the country's large domestic government debt. To tackle these problems, Pakistan must implement significant economic reforms.

- While Pakistan has not explicitly granted China preferential access to key sectors in exchange for loan rollovers or financial assurances, its broader economic relationship with China, particularly under the China-Pakistan Economic Corridor, indicates a consistent pattern of providing China with significant economic and strategic advantages. These advantages may indirectly facilitate the provision of financial assistance, including loan rollovers.

- According to the World Bank's International Debt Report published in December 2024, China is Pakistan's largest creditor, holding 22% of the country's total external debt, which amounts to $28.8 billion. Saudi Arabia is Pakistan's second-largest bilateral lender, with $9.16 billion, or 7% of the country's total debt. Although the report did not specify the United Arab Emirates' share, other bilateral creditors account for 8% of Pakistan's external debt. As of 2023, bilateral lenders were responsible for 45% of Pakistan's external debt, while multilateral lenders held 46%, with the remaining 9% owed to private lenders, primarily bondholders.

- The United Arab Emirates and Saudi Arabia have become more cautious in their financial dealings with Pakistan, as both countries have moved away from unconditional financial support and have tied their investments and loans to stricter conditions. While there are no public details surrounding their most recent assurances, Pakistan may have offered preferential access to investment opportunities in key sectors such as energy, agriculture, real estate and infrastructure development. These concessions would align with Saudi Arabia's Vision 2030 and the United Arab Emirates' focus on diversifying its economy beyond oil.

To fulfill a key IMF requirement and address revenue collection shortfalls, Pakistan plans to broaden its tax base into untapped sectors, particularly agriculture. In July 2024, the IMF proposed increasing the agricultural income tax to help Pakistan address revenue shortfalls, as the World Bank estimates that such a tax could generate revenue equivalent to 1% of GDP. However, Pakistan has struggled to implement this proposal since the constitution allows only provincial governments, not the federal government, to tax agricultural income. Since then, Sharif's government has pushed provincial assemblies to approve the necessary legislation for the agricultural tax, and all provincial governments have reportedly agreed to do so. While potential unrest from farmers and political opposition may delay progress, the tax is likely to be enacted due to pressure from coalition allies in Pakistan's Sindh province and the military, both of which are key stakeholders in ensuring provincial assemblies pass the tax. Once implemented, the tax will reduce provincial reliance on federal transfers, improve fiscal stability, and make the tax system fairer by addressing disparities in tax burdens across different sectors and groups. Additionally, better documentation of agricultural incomes could enhance compliance with other taxes, further broadening the national tax base and helping Pakistan meet other IMF conditions to secure continued financial support.

- Agricultural income contributes 24% to Pakistan's GDP and employs 35% of the labor force but generates only around 0.1% of total tax revenue.

- On Nov. 18, Sharif emphasized the importance of all sectors fulfilling their tax obligations in response to a revenue collection shortfall and assured the IMF that an agricultural income tax would be implemented starting in early 2025.

- In July, Nathan Porter, the IMF's chief of mission for Pakistan, stated that taxing the agriculture sector was a fundamental element of the IMF's new program for Pakistan. He warned that failure to uphold this commitment could jeopardize the program's overall effectiveness.

- Following the publication of Pakistan's 2025 budget, Fitch Ratings projected a fiscal deficit of 6.9% of GDP for the year, slightly higher than the target of 5.9% and still significantly above the 6% deficit forecast for 2026.