An employee counts money at a branch of Industrial and Commercial Bank of China on July 26, 2011 in Huaibei, Anhui province, China.

Struggles by the People's Bank of China to manage financial inflows are a subtle, yet significant, signal working against further renminbi internationalization, even as China touts its new e-yuan as a monetary innovation that will erode the dollar's dominance. The PBoC raised reserve requirements on foreign exchange deposits to 7% from 5% effective June 15 to make dollar inflows more costly as it tries to suppress RMB appreciation and capital inflows that could add to speculative bubbles. Using administrative measures to counter market trends, however, reinforces the view that Beijing is not ready to open capital or domestic markets, a prime factor working against making the RMB a truly international currency.

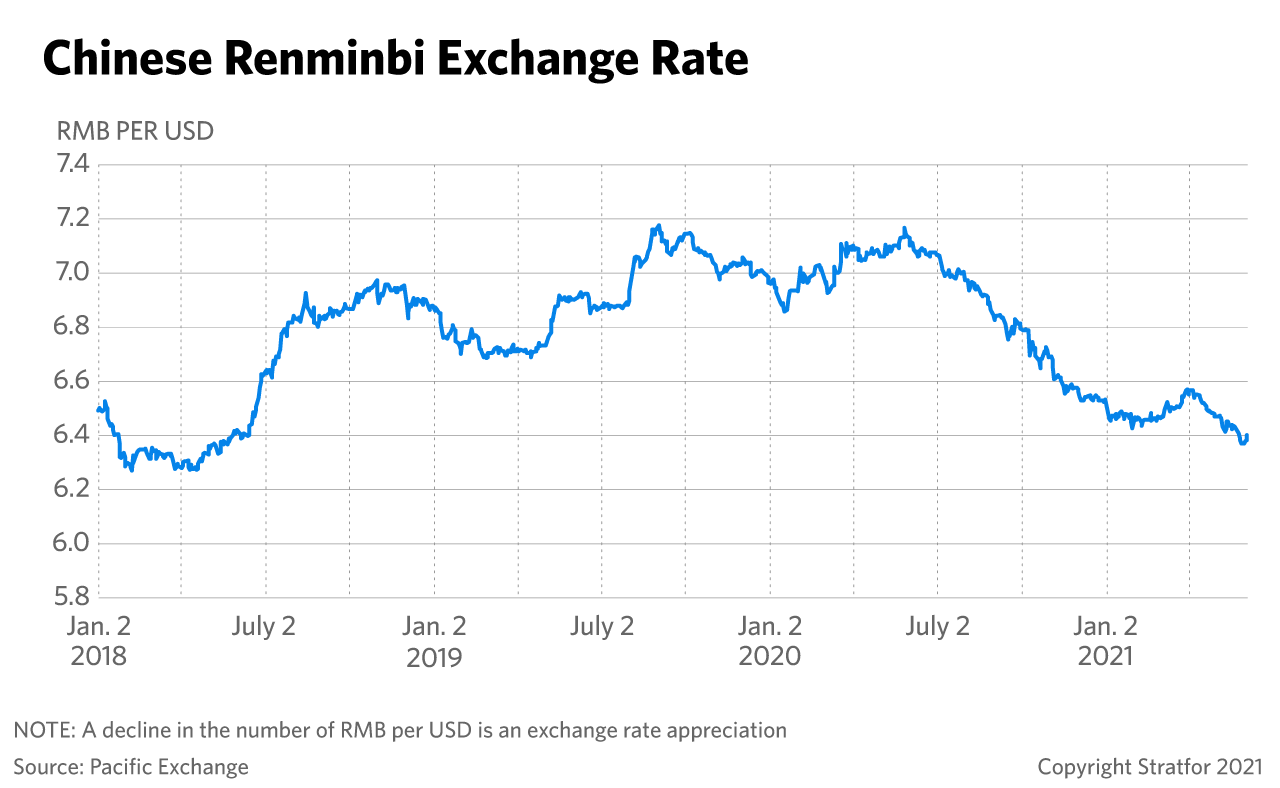

- China's exchange rate remains heavily managed, although the PBoC is trying to abjure the appearance of setting prices and particularly of intervening directly in markets with the active buying of dollars. Intervention that adds to official reserves also draws charges of currency manipulation. At the same time, however, the PBoC sets a daily reference rate for the RMB, permitting trading fluctuations of only plus or minus 2%. It also encourages dollar buying and selling by state-owned banks to slow currency appreciation, a less overt form of backdoor official intervention.

- Gross capital inflows to China are surging and the RMB is at its highest level against the dollar in three years at less than RMB 6.4 to the dollar, even as appreciation lags that of other major currencies against the dollar.

- The State Administration of Foreign Exchange (SAFE) reports nearly $770 billion in inflows in the first four months of 2021, compared with $300 billion in the same period in 2019 and $440 billion in 2020.

China's tolerance for rapid RMB appreciation seems to have reached a limit and it is trying to slow the trend, and discourage further investment in RMB assets; gone is the mixed messaging of previous weeks that a stronger exchange rate could offset imported inflation. In fact, the central bank and SAFE now maintain that depreciation should not be used to stimulate exports and appreciation is not a means to offset higher import prices. The required reserve ratio on foreign exchange is a little-used tool that hasn't been adjusted since the global financial crisis. It increases the funding rate for non-RMB currencies by shrinking the pool of foreign exchange available for domestic investment and reduces the interest rate gap with major currencies.

A higher required reserve ratio does not, however, shift the financial fundamentals that are driving currency appreciation. The PBoC's quandary is that it can slow, but not stop, increased capital inflows that fuel domestic liquidity and asset bubbles while at the same time it is encouraging deleveraging to alleviate financial risk. Other actions that could be taken include:

- Further increases in the required reserve ratio, which at 7% is still below the 12.5% for RMB bank deposits.

- Taxing profits from currency derivatives trades, as well as encouraging companies to use hedging instruments to manage foreign exchange risk.

- A decrease in one-way capital controls, giving Chinese residents a greater ability to invest abroad.

- Control the daily RMB reference rate fixing, setting it below expectations, the same tactic used to devalue the currency in 2015.

The risk, however, is that asset price inflation complicates an already-incomplete and -uneven economic recovery and threatens financial stability. China's capital controls limit financial outflows, so strong capital inflows add to domestic liquidity and inflate asset price bubbles without a safety valve for excess funds to escape the country. This plus high domestic credit creation yields speculative bubbles in real estate and stock prices. The government worries, however, that bursting bubbles will interfere with economic management and create political instability. This particularly concerns Beijing given the approaching 100th anniversary of the Communist Party of China on July 1, a date when it wants to be able to tout the Party's stewardship of the economy.

Meanwhile, the PBoC is committed to withdrawing monetary stimulus at a slow and measured pace, and the government is avoiding sharp changes in policy that could slow the economy even further. It is trying to break expectations of continued RMB appreciation that attract more capital inflows. Prices are certain to rise given that China's economy is growing and has higher returns than can be earned abroad. Asset price inflation, however, could complicate an already-incomplete and -uneven economic recovery and threaten financial stability.

- Overseas holdings of Chinese stocks increased 62% in 2020, according to Bloomberg, and the Shanghai Shenzhen CSI 300 Index is yielding one-year returns of over 35%.

- Foreign holdings of Chinese bonds were up by 47% in 2020, with the 10-year sovereign bond currently yielding more than 3%, compared with the equivalent U.S. Treasury bond yield of less than 1.6%.

- Real estate investment jumped 38.3% in the first two months of the year and was up 15.7% from the same period in 2019, before the pandemic struck, according to Reuters. Total credit for real estate increased an average of 36% a year from 2011-2020, and more than three-quarters of Chinese household wealth is in residential property, compared with 35% in the United States, according to The Wall Street Journal.

Using administrative measures to counter market trends, however, underlines the relative lack of openness of the Chinese economy. Given China's size, this is the main impediment to making the RMB a more widely accepted form of international money as a reliable store of value. Beijing does not fully recognize investment motives for buying and selling RMB assets, which conflicts with the Party view of using currency and assets for transaction purposes only. Interestingly, increased state management of the economy comes at the very time China is introducing a central bank digital currency that it hopes will undermine the dollar. These factors mean the RMB will appreciate further, especially if the PBoC reduces monetary policy accommodation. Beijing's efforts to try to stop the tides underscore that China's exchange rate remains heavily managed, with exchange rate policy set at the State Council level, not by the PBoC or financial markets.