An image shows Chinese renminbi banknotes.

Renewed efforts by China to internationalize its currency are aspirational for now, and while such moves could erode U.S. dollar (USD) dominance over time, Beijing currently lacks the political will to make the fundamental economic and political reforms necessary to put the renminbi (or yuan) in the same league. Among the changes needed to seriously challenge the U.S. dollar would be:

- An open international financial account (previously the capital account) of the balance of payments.

- A fully floating and not managed exchange rate.

- Full foreign access to China’s domestic asset markets with legal delineation of property rights.

- Central bank independence from the central government and the Chinese Communist Party (CCP).

People’s Bank of China (PBOC) officials, including Governor Yi Gang, recently floated RMB internationalization to gauge markets’ reaction, suggesting completion of a comprehensive review and possibly more proactive policy support.

- On Oct. 23, Yi said, without elaborating, China will “improve flexibility of the yuan and let exchange rates play a better role as an automatic stabilizer in the macro economy and international balance of payments.”

- The PBOC’s’ senior international official said there could be improvements in bilateral currency swaps agreements, as well as cross-border settlement and payment in yuan.

- The PBOC also released a 2020 RMB Internationalization Report in mid-August, but it’s a status report rather than a comprehensive strategy.

- It’s not known if the just-completed Central Committee 5th Plenum discussed RMB internationalization as part of its debate over a new five-year plan covering 2021-26. The current, 13th Five Year Plan (2016-2020) states a desire “to steadily promote RMB internationalization and see RMB capital go global” as part of broader financial and economic reforms, but the CCP has since dropped any references to financial account convertibility.

China’s efforts to internationalize the RMB peaked in 2016 and have lagged ever since. The endeavor began in 2009 after the global financial crisis and ultimately led to the International Monetary Fund (IMF) including the RMB as one of five currencies in its basket for valuing Special Drawing Rights (SDRs) in 2016. By definition, an internationalized currency is one used widely by private and public sectors outside of and unrelated to the issuing country. The RMB has a weight of nearly 11 percent in calculating the SDR value. But its addition to the five-currency basket in 2016 was mainly a political decision and not important in economic or financial terms, since the SDR cannot be used internationally for trade settlement or investment. Accordingly, the United States acquiesced and did not see the RMB’s inclusion in the SDR basket as a challenge to the dollar’s dominance.

Between September 2015 and July 2020, the Singapore-owned Standard Chartered Bank’s index of RMB globalization, which measures global utilization, declined by 16 percent. This drop was likely driven in part by the following factors:

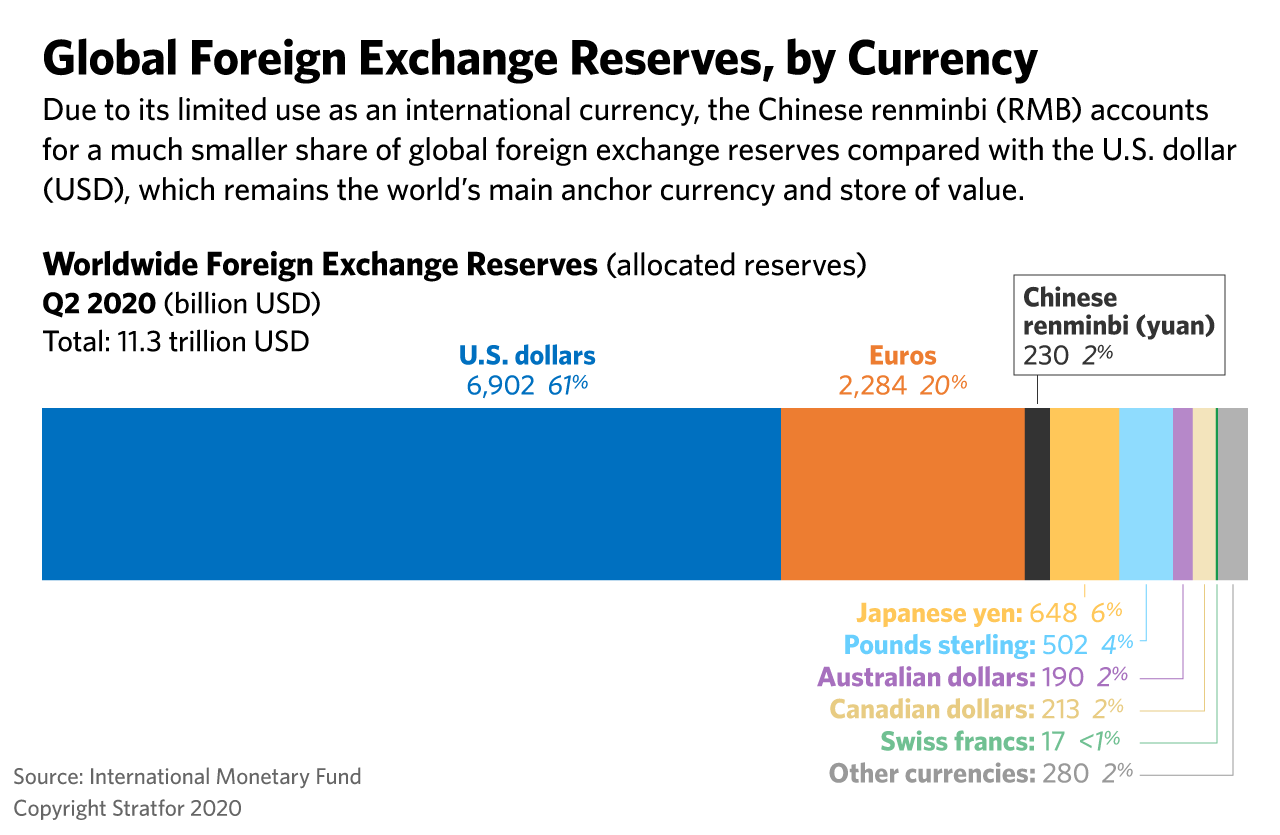

- The RMB’s use as a reserve currency accounts for only 2.05 percent of total official foreign exchange reserves, an increase from 1.23 percent at the end of 2017. That compares with USD shares of 61.26 percent, down from 62.72 percent in the same period.

- Recorded RMB international transactions via the Society for Worldwide Interbank Financial Telecommunications (SWIFT) network have risen from 1.56 percent of the global total in February 2018 to only 1.97 percent in September 2020.

- According to the Bank for International Settlements (BIS), the RMB was on one side of only 4.3 percent of daily foreign exchange transaction turnover cleared through BIS banks in 2019, compared with 88.3 percent for USD.

- Regarding private sector investment, the IMF’s Coordinated Portfolio Survey shows $2.3 trillion in total holdings of international portfolio investment in China, or 3.4 percent of the global total of $66.7 trillion — up from the 1.7 percent in mid-2017, but still a paltry amount for the world’s second-largest economy.

The RMB’s Limited Use

Money has three functions — a unit of account, a means of transaction, and a stable store of value. The RMB, however, is largely a transactions currency useful for dealing only with the issuing country, which in this case, is the world’s largest trading nation. According to WTO data, China accounts for nearly 13 percent of global exports of goods and services, compared to 11.6 percent for the United States. This means a large portion of global business transactions with China is conducted in other currencies.

Given that China is the second-largest global economy, the most critical issue involves establishing greater confidence in the RMB as an investment vehicle and substantially deepening Chinese financial markets to improve international liquidity. The full establishment of a currency on a global level requires bottom-up demand from both the private and official sectors. But the RMB’s use as a store of value — meaning it can be traded and stored for future use, which is one aspect of the definition of international money — is lagging. The RMB is not a fully convertible currency that can serve as a safe haven when international investors need one. There is also no widespread use of the RMB as an investment asset with reserve currency status.

- Global foreign exchange reserves in RMB totaled $230 billion in the third quarter of 2020. This makes the RMB the fifth-ranking reserve currency in the world, only slightly ahead of the Australian and Canadian dollars, as well as the Swiss franc.

- Nearly 40 central banks have swap agreements with the PBOC, but those function more as bilateral clearing accounts for invoicing and payments settlement than emergency liquidity support.

There is also significant doubt over whether China is willing to make tradeoffs necessary to establish a global currency that rivals the U.S. dollar by opening domestic markets and the political system. Indeed, the CCP appears unwilling to take the risks of policy reforms needed to internationalize the RMB for fear that an open economy with a freely floating currency would make China more vulnerable to international economic and financial shocks.

- China lacks well-developed financial markets, and its financial system is subject to heavy regulation and political control. Domestic financial markets are being opened gradually and incrementally, but CCP officials are cautious of increased exchange rate volatility as capital controls are relaxed and the country slowly moves away from a managed exchange rate.

- State-owned enterprises (SOEs) would be forced to compete directly with outsiders if the RMB were fully internationalized. They may be entirely capable of doing so, but SOEs remain at the heart of state economic control, even when they are loss-making “zombie” enterprises.

- Moreover, full reserve currency status requires expansion of the money supply held abroad to maintain liquidity, which would make China’s net international investment position less positive. It would give foreigners greater control over domestic assets, which would be subject to market risk and possible capital flight.

Instead, it seems Beijing wants only the prestige of the RMB as a challenger to the U.S. dollar without creating the necessary underlying conditions, which include providing emergency international liquidity in crises. The U.S. Federal Reserve (Fed) is the global liquidity provider of last resort in emergency financial conditions. During such periods of stress, the PBOC could be called on for support, including in the current pandemic. The Fed’s balance sheet expanded by issuing new liabilities from less than $1 trillion in 2008 to more than $7 trillion at present, including an increase of $3 trillion during the ongoing COVID-19 crisis alone.

What’s Next?

The RMB had its best quarterly performance against USD in 12 years in the third quarter of 2020, rising by 4.1 percent. In mid-October, the RMB was also at its strongest level since July 2018. Underlying the currency’s appreciation is a strengthening of the post-pandemic economic recovery and 10-year sovereign bond yields more than 200 basis points greater than U.S. Treasuries. China seems comfortable with the CNY strengthening at this time, as the country takes market share from foreign competitors hobbled by virus outbreaks despite an appreciating exchange rate.

China’s move to slightly loosen capital controls in October further suggests government acceptance of limited capital outflows and perhaps a more market-determined exchange rate. The move was aimed at reducing restrictions on short sales of CNY, while increasing the amount of domestic funds available to institutional investors to send abroad. Yet, the gradual opening of securities markets will bring in only a few hundred billion dollars of portfolio flows.

To increase the RMB’s use as a store of value, the Chinese government must address policies related to exchange rate management, domestic financial repression and capital market reforms, capital controls and opening of the financial (capital) account, as well as broader governance issues, including private property rights. Chinese leaders have yet to show commitment to developing the RMB as a USD alternative in any of these areas, valuing internal stability over other issues despite a stated goal of finding international alternatives to the USD.

No one in Beijing has yet to advocate for the immediate liberalization of China’s economy and the opening of a capital account. This would need to be sequenced carefully to avoid capital flight and implemented in something other than an opaque manner with consistent enforcement over time and across administrative areas. Limiting foreign access to domestic capital markets, however, sends a signal that those markets are subject to new controls during a crisis and that use of the currency may be impeded. For example, restrictions on selling stock and the introduction of new capital controls in 2015 only raised investor concern about limiting trades and liquidity during a crisis, even as those restrictions have somewhat eased five years later.

Also important to international investors are governance issues, including clearly defined property rights and an objective dispute settlement process. China’s abolition of presidential terms limits in 2018 has since only increased market perceptions of political risk. Beijing committed to implementing improvements in governance and financial markets in its China 2030 project with the World Bank, and the PBOC has also pushed to accelerate reforms and develop capital markets. But the results of these efforts have been lacking and some progress has been reversed.

The bottom line is the RMB is far from being a safe haven currency, and while it potentially could slightly erode the role of the USD, it is not expected to pose a serious challenge for at least several decades, if then. Barring significant policy changes that seem implausible for now, the RMB will remain a second-tier (if not third-tier) currency for the foreseeable future.