The United States is likely to experience a weak economy for a prolonged period, which, when combined with high debt levels, will have long-lasting effects on federal spending and perhaps even Washington's ability to exercise global influence as the country turns inward. The United States' pandemic-induced recession may have bottomed out in the April-June quarter, with GDP shrinking at a record pace. But with growth sluggish even before the pandemic, prospects for the U.S. economy remain stark. Base effects alone probably ensure positive growth in the third quarter of 2020, though signs the U.S. recovery is already slowing means another contraction in the fourth quarter cannot be ruled out. And with infections on the rise across America, there's an increasing chance that U.S. GDP growth could remain below pre-pandemic levels for years to come.

What Happened

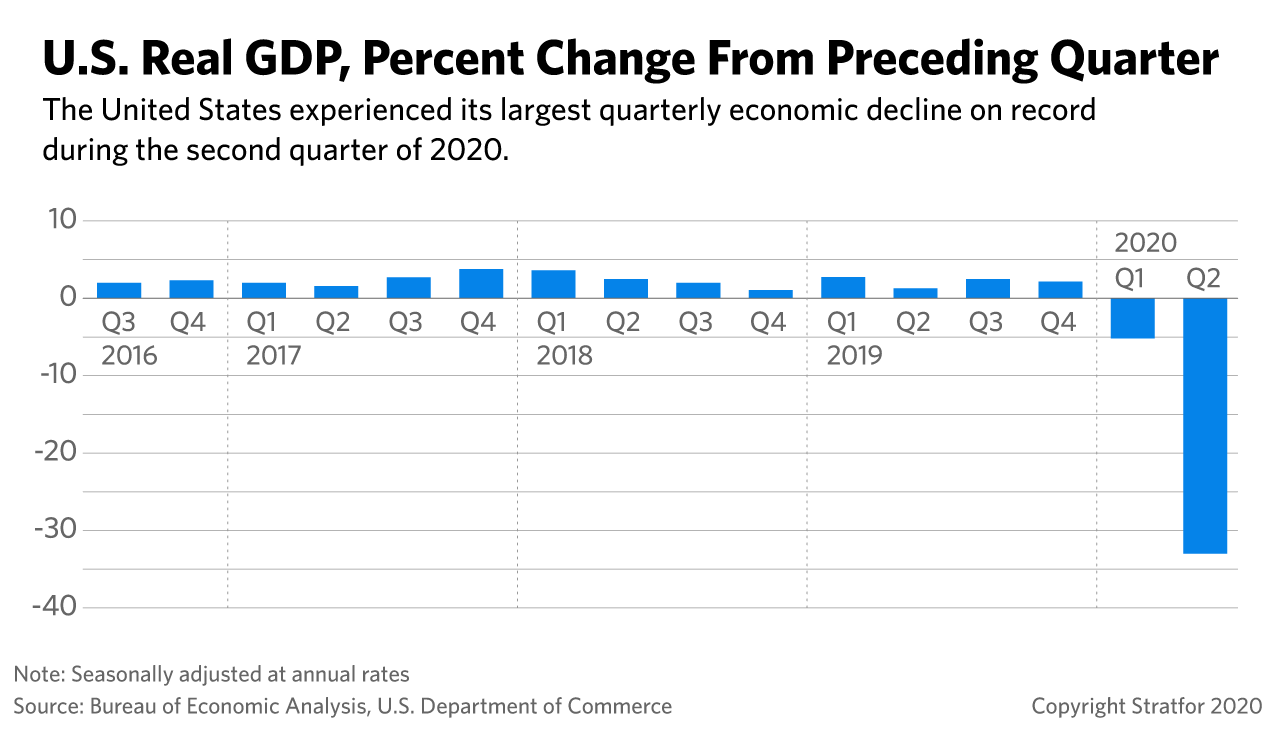

As widely expected, the initial estimate for U.S. GDP growth, the broadest measure of economic activity, fell sharply in the second quarter of 2020, by an annualized rate of 32.9 percent. While slightly less than the consensus forecast of about 34 percent, the decline marks the largest-ever on record since the United States began compiling quarterly data on an annual basis in the 1940s. First-quarter GDP growth was also revised down to -5.0 percent.

The U.S. economy will likely grow in the third quarter of 2020, as lockdowns peaked in April. Nonetheless, with virus outbreaks surging in at least 21 states, high-frequency indicators of economic activity that include credit card sales and hotel occupancy rates show a stalling recovery. This will amplify the damage already done to incomes, consumption, investment and unemployment. Even moderate containment measures, such as continued social distancing and working from home for some occupations and industries, will still undermine economic activity. On July 29, U.S. Federal Reserve Chairman Jerome Powell underlined these concerns by explicitly stating that “the path of the economy will depend significantly on the course of the virus,” and that a resurgence threatens to derail the U.S. recovery.

- American households will remain wary of spending on anything other than essential consumption. Personal consumption, which accounts for about two-thirds of U.S. GDP, fell at an annualized rate of 34.6 percent in the second quarter. The personal savings rate as a percentage of disposable income also nearly tripled, rising from 9.5 percent in the first quarter to 25.7 percent in the second.

- Personal incomes jumped 32.6 percent in the second quarter, though this was driven mainly by government transfers whose future is unclear. The pending expiration of enhanced unemployment benefits, even if Congress passes a stopgap extension, nonetheless increases uncertainty underlying continued income and will continue to fuel consumer retrenchment as households fear further outbreaks and renewed unemployment.

- Moreover, according to Reuters, 17.3 million Americans owe $21.5 billion in past-due rent. The federal eviction ban also expires on July 31, with Congress seemingly stalemated on an extension.

- Unemployment will be the largest continuing drag on the economy. Official unemployment figures have understated the damage to labor markets due to problems in distinguishing workers either on furlough, as unemployed, or out of the labor force. In addition, the end of the Paycheck Protection Program on August 8 could cause delayed job cuts as businesses lose support in the face of declining sales. The labor force participation rate is 61.5 percent, a small uptick but not enough to recover from the February-April dip. Meanwhile, initial jobless claims in the latest reporting period (which includes a lag) were up for the first time since they exploded in March. Continuing claims fell slightly, but the four-week moving average of initial claims seems stuck at 1.4 million, with more than 30 million Americans believed to be receiving some kind of income support.

- The situation is no better for U.S. businesses, as corporate profits continue to plunge amid ongoing uncertainty about demand and supply bottlenecks. Fixed business investment declined by an annualized rate of 27 percent in the second quarter, with real estate investment falling by 38.7 percent. Non-residential fixed investment has declined for five consecutive quarters and is not expected to recover significantly this year as both large and small companies face bankruptcies. At the end of June, more than 3,600 U.S. companies had filed for Chapter 11 bankruptcy in the first half of 2020, a 26 percent jump from the same period in 2019 and a 43 percent surge over June 2019, according to legal services data from Epiq Global.

- Meanwhile, government spending was up by 2.7 percent in the second quarter as a result of massive federal spending. Coming pullbacks in government spending are certain, however, as there remains no consensus on how much federal stimulus is needed. Declining state and local revenues will also constrain spending at those levels since 48 states have some kind of requirements to maintain balanced budgets, according to the U.S. Government Accountability Office. For context, it took 10 years for state and local government spending to recover from the 2007 recession.

- While net U.S. exports (the final expenditure category of GDP) were up negligibly in the second quarter, the outlook for trade remains uncertain amid plummeting global trade demand and escalating U.S.-China tensions.

What's Next

As for policy responses, Powell strongly implied the Fed had reached limits of its toolbox, even if it is prepared to do whatever is necessary to keep the U.S. economy afloat amid the country's worsening COVID-19 crisis. Fiscal policy must instead do the heavy lifting going forward. The so-called “dot plot” from the Federal Open Market Committee meeting in June shows the Fed's unanimous view that interest rates will remain near zero through 2021 with only two members foreseeing an increase in 2022 and Powell discouraging the idea of negative rates.

Fiscal policy, however, may be about to go over a cliff with Congress and the White House seemingly deadlocked on the size of renewed spending and transfers. So if fiscal policy needs to carry the weight but can't, or if there's insufficient political will to reach a deal, the United States will be in for a prolonged period of economic stagnation, with the government severely constrained in its ability to respond to business cycle fluctuations.

Federal spending priorities will need to be reoriented, especially as Washington copes with a record level of debt, which will also have implications for the United States' global role by limiting its ability to project power, whether hard or soft. China and Europe are well ahead of the U.S. in controlling their COVID-19 outbreaks, and whether it wants to or not, the United States will need to design budgets in line with its resources, which of necessity might also include declining military spending and foreign aid.