Amid China's slower-than-expected post-COVID economy recovery, Chinese policymakers have been focused on reviving consumption as an engine of economic growth. This focus is partly due to the lagging performance of most traditional drivers of Chinese economic growth — e.g. real estate and infrastructure — with the exception of exports, which have experienced strong growth through early 2025 but are now under threat by U.S. tariffs and broader Western protectionism. It is also partly due to Beijing's long-term economic reform plan to transition away from these less capital-efficient traditional growth drivers and toward a higher reliance on consumption, a plan intended to improve the stability of Chinese economic growth while making China less reliant on volatile export markets.

However, at monthly Politburo meetings and annual legislative sessions, Chinese officials have repeatedly resisted calls from foreign and Chinese economists, businesses and former officials for consumer stimulus (i.e. large-scale cash hand-outs, major expansions of social services, or other structural wealth transfers to low-and middle-income households), primarily due to Beijing's economic reform plans and concerns about fiscal sustainability. Instead, Beijing has opted for more measured support, ranging from easier credit access for businesses and households to debt restructuring for local governments — with the hope that they spend more on consumption — and recapitalization of state banks to facilitate lending to businesses and households. But the most closely watched of China's economic support measures has been its consumer subsidies program, which is the closest thing to consumer stimulus and is intended to help Beijing fulfill its top economic goal for 2025 of reviving consumption.

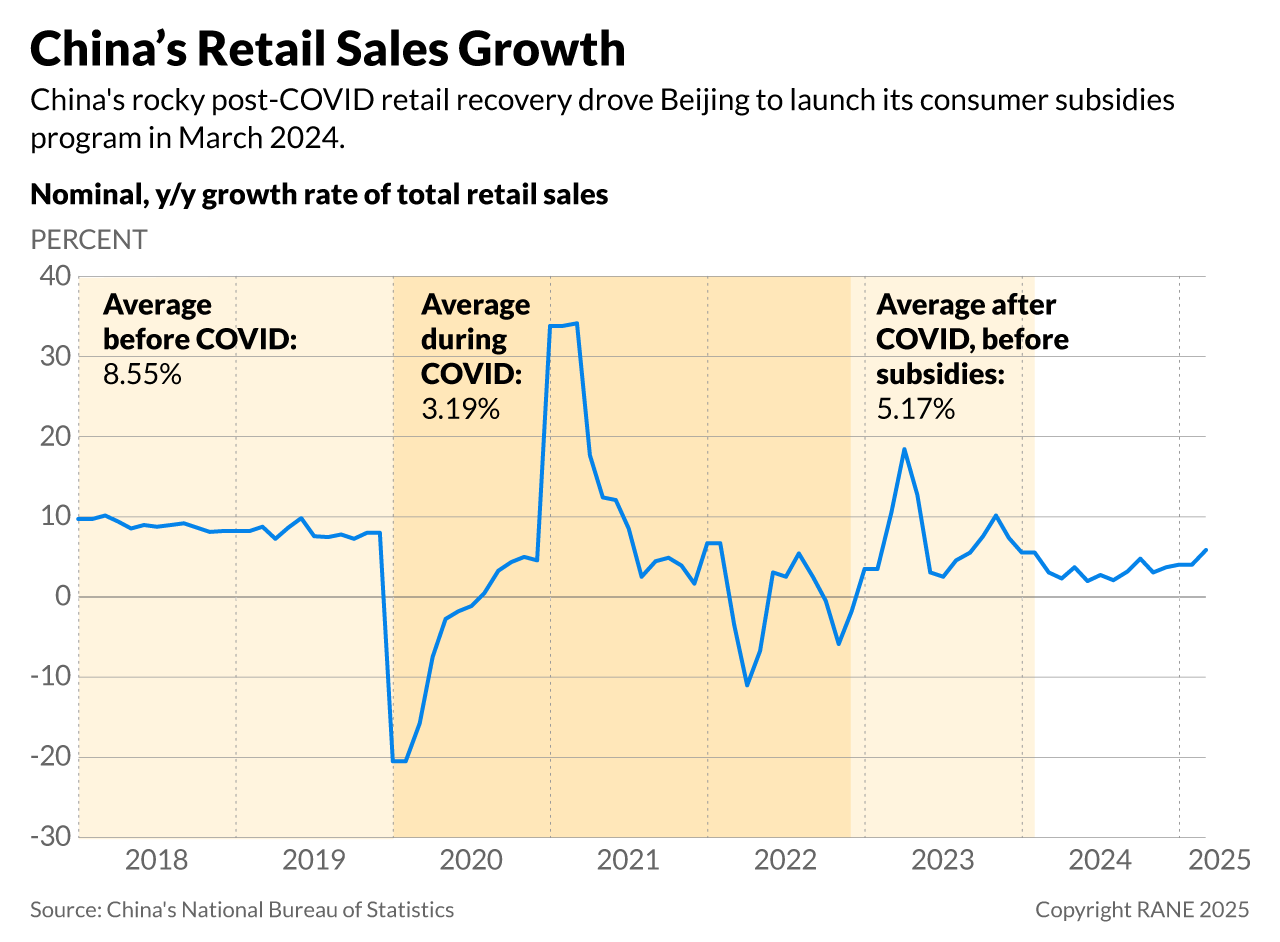

In order to evaluate the effectiveness of these subsidies, RANE examined trends in China's retail data pre- and post-consumer subsidies (with May 2024 as the demarcation date between these two periods) and used these trends as a platform to examine the efficacy and trajectory of Chinese consumer economic support measures. Overall, we find that, despite the mixed results of China's consumer subsidy program, Beijing will likely continue to resist large-scale consumer stimulus unless U.S. tariffs grow substantially. Further, middling consumption will further constrain a revival of Western investment in China and further drive Beijing to crack down on internal information flows and retaliate against Western trade restrictions.

The Data and Their Limits

China's consumer subsidies program came in four tranches, and they focused on sectors most impacted by the real estate downturn — e.g. household appliances and furniture — as well as industrial policy priorities like electric vehicles and export-focused industries most exposed to U.S. tariffs, such as consumer electronics:

- In March 2024, China's State Council, the administrative headquarters of the government, launched a program to subsidize consumer trade-ins of old furniture, household appliances, and vehicles, with the program funded via preexisting central government carbon reduction and commercial development funds. These subsidies became available in May 2024.

- In July 2024, the State Council announced it would upgrade the consumer subsidies program by raising subsidies for automobiles and household appliances, and it committed 150 billion yuan ($21 billion) of direct funding for the subsidies (as opposed to redirecting carbon funds) funded via special treasury bonds.

- In January 2025, the State Council again upgraded the consumer subsidy program to include purchases of smartphones, tablets and smartwatches, and to expand the categories of eligible household appliances. The finance ministry also announced it had allocated 81 billion yuan ($11 billion) for the trade-in programs in Q1.

- In March 2025, at China's annual "Two Sessions" legislative meetings, the annual government work report included a pledge to fund consumer trade-in programs with 300 billion yuan ($41 billion) of special treasury bonds in 2025. For comparison, this equates to 1% of China's projected $4.1 trillion of national government spending in 2025.

China's National Bureau of Statistics (NBS) puts out monthly reports of retail sales data, including total sales (by yuan) and year-on-year growth rates, with these two figures available for individual retail segments (e.g., furniture) as well as topline retail sales. Beijing is notorious for altering its statistics to fit optimistic political narratives and for failing to report other statistics altogether, calling into question the utility of analyzing Chinese government figures. However, trends can be gleaned even from manipulated data by using a difference-in-difference approach, in which the "effect" of Chinese authorities tampering with the data is treated as equal (unchanging) across the timeline evaluated (in this case 2018-2025), allowing for an evaluation of the change in certain statistics before and after the application of an external treatment (in this case, the consumer subsidies imposed in 2024). Alternatively, one can assume that the NBS-reported data is the most optimistic version of Chinese economic performance, in which case an analysis of the data can produce a "best-case scenario" outlook for China, with the working assumption that the economic reality is likely less flattering.

There is also the issue of recent U.S. tariffs on China (rising from the preexisting 25% in January to 35% in February, 45% in March, 170% in April, and then back down to 55% in May) and their impact on Chinese retail sales, as U.S. tariffs on Chinese exports are bound to reduce factory activity, assuming Chinese producers cannot quickly find alternative markets. Reduced factory activity tends to spur lower or withheld wages as well as layoffs, which on the margins can reduce household spending capacity, retail sales and overall consumption, as business-to-business purchases also lag. Despite this potential confounding effect, the timeline for this analysis (2018-2025) largely predates the latest tariffs, which only influence the last two months of data (February-March 2025). In those two months, however, an inflationary effect is more likely than a deflationary impact on retail sales as markets stocked up on Chinese exports ahead of expected higher tariffs in April. Tariffs from U.S. President Donald Trump's first term (imposed over 2018-2020) were also expected to depress retail sales data prior to COVID-19, with the effect wearing off as Chinese firms rerouted exports to the United States through third countries during China's three-year COVID-19 period, a phenomenon now well-documented in trade figures. Without these first-term tariffs, there likely would have been an even greater disparity between pre- and post-COVID retail sales growth, further underlining the utility of analyzing China's recent consumer subsidies.

With these caveats in mind, an analysis of the total retail sales data from 2018-2025 makes it obvious why Beijing developed a consumer subsidies program. The average year-on-year growth rate of China's nominal monthly retail sales for the two years pre-COVID (2018-2019) was 8.6%, far outstripping the 3.19% growth during COVID (2020-2022) and the 5.17% growth in the post-COVID period before the introduction of subsidies, barring a few outlier months (April, May, October and November of 2023) when retail sales growth surged relative to lockdown periods in those same months during 2022. Thus, the consumer subsidies program launched in March 2024 was partially a bid by Beijing to revive topline retail sales (and broader consumption) growth closer to pre-COVID levels.

Beijing also targeted subsidies at certain sectors — furniture, home appliances, consumer electronics and vehicles — that needed the most support. Furniture and home appliance sales had been wilting since China's real estate downturn began in 2022, dragging down sales for home furnishings. Chinese vehicle exports (particularly of electric vehicles) are a priority sector for Beijing's industrial development plans and have been facing geopolitical headwinds as Europe and the United States — two major consumer markets — have implemented protectionist measures to insulate their domestic automobile industries from Chinese competition. Consumer electronics weren't subsidized until early January 2025, after Trump had won the U.S. presidency and before his inauguration, as Beijing had good reason to believe (based on Trump's first term) that he would follow through on his repeated campaign pledges for new tariffs on China, and consumer electronics would be one of the Chinese export sectors hit hardest by such tariffs.

The Fallout From China's Real Estate Downturn

In August 2020, the Chinese government began implementing its "Three Red Lines" policy of debt controls in the real estate sector, in an effort to deflate the housing debt bubble. Since then, China's real estate sales have plummeted, with monthly home sales figures largely lingering in the range of -20% to -40% year-on-year growth from mid-2021 throughout 2024. Though early 2025 figures suggest retail sales may be finally bottoming out, they have yet to resume steady positive growth. This down period for real estate has weighed on local government budgets, which extract revenue from land sales to real estate companies. It has also weighed on household savings in China, 70% of which is stored in real estate, and thus on consumption by diminishing appetites for discretionary spending.

What Worked, What Didn't, and What's Next

Overall, the effects of China's consumer subsidies on these sectors are mixed when comparing the post-COVID, pre-subsidies period of January 2023-April 2024 (minus the aforementioned months with high base effects) to the post-subsidies period of May 2024-March 2025. The average year-on-year growth rate of monthly retail sales of furniture rose from 0.9% pre-subsidies to 16.8% post-subsidies. Growth rates of home appliance sales likewise surged from 2.8% to 7.4%. When evaluating the three months of subsidies on communication equipment (January-March 2025), the growth rate was 27.0% compared to 13.2% for the same three months in 2024. For unclear reasons, however, the growth rate of vehicle sales actually declined after Beijing introduced subsidies, from an already low 0.5% to -1.4%. Similarly, overall retail sales growth slowed from 4.9% to 3.6% after the implementation of subsidies, even when categories of retail goods with volatile pricing (like food and petroleum products) are excluded from calculations.

In the face of these difficulties, Beijing will likely gradually expand funding for consumer subsidies. Although Chinese consumer subsidies have lifted retail sales in subsidized categories, they've been ineffective or even counterproductive at raising overall retail sales, though this post-subsidy retail sales dip is likely influenced by various exogenous factors. Regardless of the reasoning for this dip, the inability of subsidies to raise overall consumption should not be too surprising given the modest scale of funding (at least $31 billion) that the Chinese government allocated to consumer subsidies from May 2024 to March 2025 relative to the scale of Chinese total retail sales ($6.3 trillion) and sales of subsidized retail goods categories ($917 billion) in that same period. Given these results and Beijing's top economic goal for 2025 being to revive consumption, it seems likely that the Chinese government will gradually scale up the funding for its consumer subsidies program in the next year.

Nonetheless, Beijing will likely avoid a more rapid expansion of funding and large-scale consumer stimulus so long as U.S. tariffs don't ramp up again. Lackluster consumption is placing increasing pressure on Beijing to replace the subsidy program altogether with a large-scale stimulus program. For instance, foreign and domestic economists have been calling for a cash handout system in China since mid-2023. Economists have also proposed that China make structural changes to boost household income, like lowering taxes, increasing social spending, or other means of structurally transferring wealth to the lower and middle class. So far, however, Beijing has resisted calls for what top CCP officials pejoratively call "flood irrigation stimulus," primarily because it could endanger China's broader economic reform plan and exacerbate the risk of a debt-fueled financial crisis. Likewise, Beijing has refrained from structurally raising household incomes, which could permanently increase the strain on local government budgets (e.g., if social spending, a municipal responsibility, were expanded) and exacerbate Beijing's concerns of a financial crisis. The May 12 bilateral tariff reduction deal with the United States suggests China is in no rush to rapidly accelerate economic support measures or to shift from short-term, cyclical support to structural reforms that would permanently boost household spending capacity. However, a dramatic re-escalation in the U.S.-China trade war — especially via the imposition of high U.S. tariffs over many months — could push China to accelerate its timeline for expanding the scale of consumer subsidies or opt for outright stimulus, given the deleterious effect of tariffs on manufacturing activity and thus on wages, employment and consumption.

The Impact on Western Businesses in China

Broadly, slower consumption growth will weigh on Western investment in the Chinese market, exacerbate foreign uncertainty about the health of China's economy, and drive Beijing to expand its retaliatory toolset against U.S. (and to a lesser extent, other Western) trade restrictions to better insulate the slowing Chinese economy. The apparent ineffectiveness of consumer subsidies at raising retail sales, paired with Beijing's resistance to stimulus, suggests that China's post-COVID consumer activity will remain depressed (relative to pre-COVID levels) for the foreseeable future. In conjunction with other factors (including uncertainty over U.S. tariffs and U.S.-China strategic competition), this lingering consumption slowdown will also prevent a revival of Western investment flows in China. Even prior to the latest tariffs, foreign investment into China had slowed markedly in recent years, with inbound foreign direct investment dropping 8% year-on-year to 1.13 trillion yuan ($157 billion) in 2023 (the first drop in over a decade); this figure fell by another 27% in 2024 and 11% in Q1 2025. Annual surveys by the U.S.-China Business Council and European Chamber of Commerce in China in 2024 support this connection between lower consumption and lower investment interest, with member businesses citing insufficient demand, overcapacity and macroeconomic headwinds as the primary restraints on increased profitability in China, beating out geopolitical factors.

Without the prospect of a consumption revival, Beijing will also remain highly concerned about social unrest and focused on mitigating internal threats to public stability, following the nationwide White Paper protests of November 2022 and growing incidences of Chinese worker protests and strikes in the last two years. This concern is partially driven by China's mounting youth employment problem, with the unemployment level among urban youth (age 16-24) steadily rising from 11% in 2018 to 21% in June 2023, before Beijing started excluding students from the formula. Even after this tweak, the new figure rose from 15% in December 2023 to 19% in August 2024, during the summer unemployment peak. Thus, with weaker consumption exacerbating unemployment concerns (and vice versa), Beijing will likely adopt more crackdowns on protests, as well as more censorship of economic data and dour economic commentaries from academia and the private sector, further increasing the opacity of China's information environment and the difficulty of evaluating new investments for foreign businesses in China. These domestic dynamics will also drive China to expand its toolset of economic retaliations (including myriad non-tariff restrictions) to counter U.S. economic threats — and to a lesser extent threats from other Western partners — that could further destabilize China's domestic economic and social conditions. The upshot is that Beijing's perhaps prudent caution about economic stimulus, combined with its systemic aversion to unrest and propensity for censorship, risks further eroding the Chinese business environment at a time when it is most eager to mitigate the deleterious impacts of geopolitical competition and trade wars.