The risk of significant unrest in China persists following the 2022 White Paper protests driven by continuing poor economic prospects. New protests could drive the government to abandon economic reforms and threaten the president's tenure, exacerbate political centralization of power, or further restrict China's information environment. Since the White Paper protests of November-December 2022 and the Chinese government's subsequent abrupt end to its "zero-COVID" policy of frequent lockdowns and travel restrictions in December 2022, no other Chinese protest movement has been so geographically widespread or as well covered by the Western media. The risk of major protests in China remains significant, as illustrated by recent protests that have grown far larger than White Paper by participant count despite the lack of coverage on them in the West. Moreover, the underlying drivers of unrest have continued to build, prompting occasional large and interprovincial demonstrations, like the November 2024 Kaifeng soup dumpling bike rides and the January 2025 Pucheng vocational school protest.

- The November-December 2022 unrest garnered the name the White Paper protests after participants started holding up blank pieces of white paper to protest their inability to speak against the government despite the massive burdens placed on the people by Beijing's restrictive measures to combat the COVID-19 pandemic. Protests took place in more than a dozen cities and on at least 50 Chinese university campuses, with most demonstrations drawing hundreds or thousands of participants. The protests eventually prompted authorities to ban gatherings in key locations and conduct arrests, but it also spurred Beijing to abruptly abandon its COVID-19 lockdown policies in December of that year.

- From Nov. 27-29, 2024, university students from the central Chinese city of Zhengzhou participated in a viral social media bike ride, using rent-a-bikes to travel 60 kilometers (about 37 miles) to the neighboring city of Kaifeng to eat some of the city's famous soup dumplings. Though local state media at first covered the activity to advertise local tourism, it soon grew to more than 100,000 participants. Many interviewed college students said the ride was meant to protest their extremely poor employment prospects, and some were captured on video waving flags pushing for greater freedoms. Students from other universities across China soon joined in, with bike rides originating in Beijing, Wuhan, Chengdu, Hefei, and Nanjing, and total participation estimated at about 800,000. Authorities eventually intervened, blocking bike traffic at key intersections and pushing bike rental companies to remotely lock bikes that crossed city boundaries, effectively ending the protests.

- In early January 2025, parents and students from a vocational school in Pucheng county of Weinan city in Shanxi province gathered to protest the sudden death of a school student, presumably due to bullying, and the school's attempts to cover up the causes of the incident. The protests attracted local residents, growing to an estimated 50,000-100,000 participants (compared to Pucheng's total population of around 800,000) and lasting a week. Riot police were eventually summoned and violent clashes with protesters ensued, resulting in numerous arrests and the authorities blocking all city traffic from the area around the school.

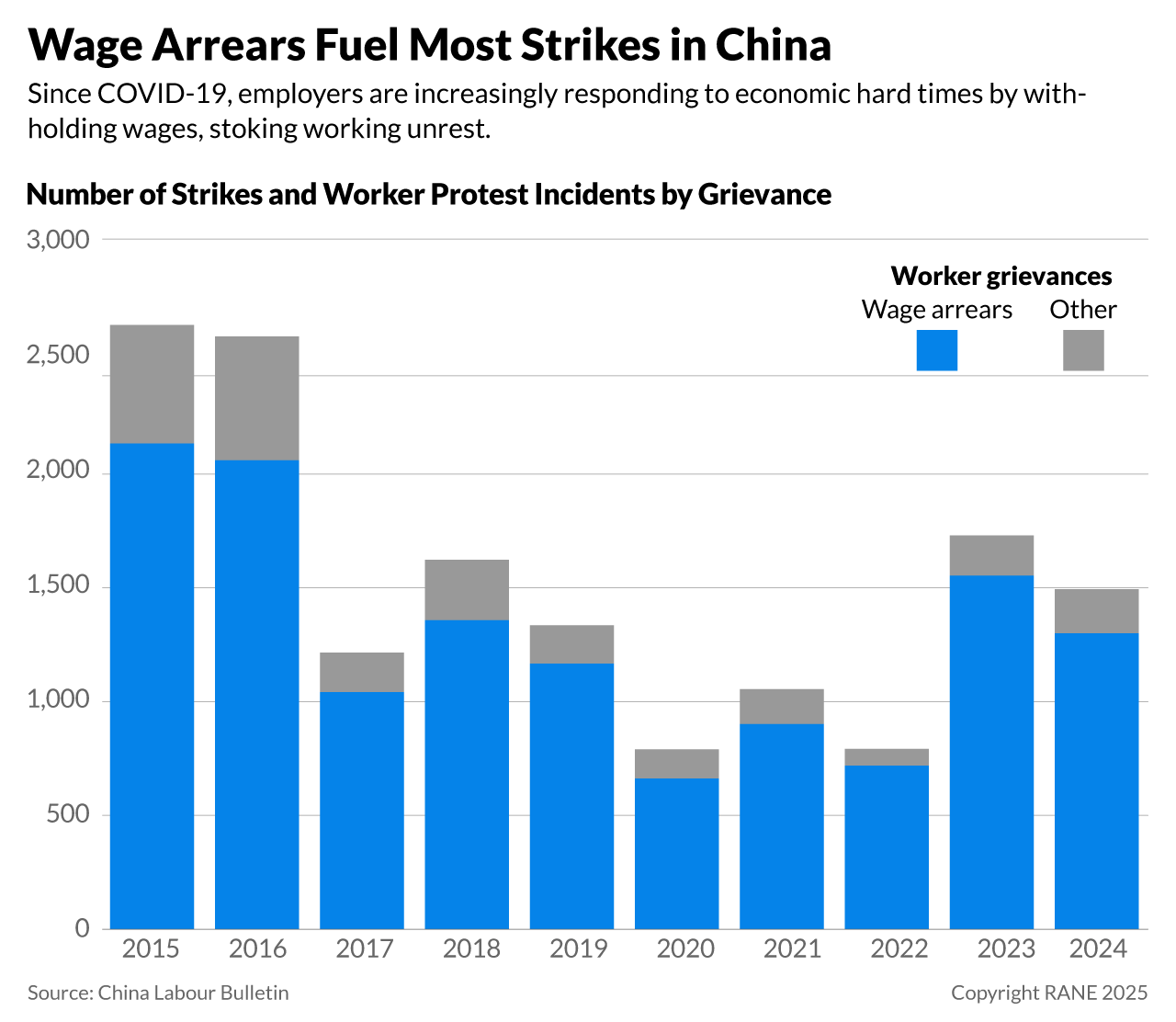

Recent data suggests the real estate downturn and an uptick in employers not paying wages are the main drivers behind protests, while the authorities and employers are less willing to engage with protesters' demands (partly due to financial constraints) and may instead be increasingly reliant on censorship to nip protests in the bud. These major protests are far from the only ones happening in China. Much more common are the smaller protests often only reported within China by anonymous netizens who post pictures or videos on social media, which government censors swiftly take down. These protests are usually of a small enough scale, censored quickly enough or related to such parochial interests that foreign media outlets do not report on them. Since January 2023, data from Hong Kong-based nongovernmental organization China Labour Bulletin shows that construction-related protests, driven by the real estate downturn, now account for most demonstrations, and there has been a significant rise in protests over wage arrears. A growing share of protests are also small-scale, and the number of protests in 2023-24 is elevated, unsurpassed in the data set except by the 2015-16 Chinese real estate and stock market crashes, suggesting lingering social discontent since the White Paper protests. Meanwhile, employers' willingness to negotiate relative to their summoning of the police or use of violence against protesters seems to have fluctuated alongside China's economic prospects, with more negotiations in 2023 amid post-COVID economic recovery hopes and far fewer in 2024, when those hopes had been dashed. Government intervention (e.g., mediation) appears to similarly fluctuate, likely due to the status of local government finances. Furthermore, more of these events have unknown resolutions, suggesting Beijing is being more proactive about curbing coverage of protests online.

- China Labour Bulletin has been tracking strikes and other workers' grievances in China since 2011, mostly using social media posts, though it does not track protests for nonworker grievances (e.g., the Pucheng protests and Kaifeng bike rides).

- In the two years since China emerged from zero-COVID in January 2023, 87% of CLB-logged protest events were due to wage arrears, compared with 73% from 2011-2022 (the remainder of CLB's data set). This is partly due to a phenomenon in China whereby employers in economic hard times commonly delay wage payments for up to several months, using the prospect of full repayment to deter resignations.

- The share of small protests (from 1-100 participants) has grown since the start of CLB's data, with 78% of protests being small from 2011-22, a figure that grew to 83% in 2023 and 96% in 2024. This may be due to a rebound effect from government crackdowns on protests during COVID-19, a period during which protests were larger than average.

- The number of protests was also elevated in 2023-24 at 3,297, a high unmatched since the 2015-16 Chinese stock market and real estate crashes, when CLB logged 5,446 protests in two years.

- The response to protests has also shifted. From 2011-22, 64% had an unknown resolution, while 19% saw police intervention, 9% government intervention, 6% negotiation with employers and 0.4% violence against workers. In 2023, after the White Paper protests, those figures shifted to 72% unknown, 11% government intervention, 9% negotiation, 5% police and 2% violence. In 2024, they were 92% unknown, 5% police, 1% violence, 1% intervention and 0.6% negotiation.

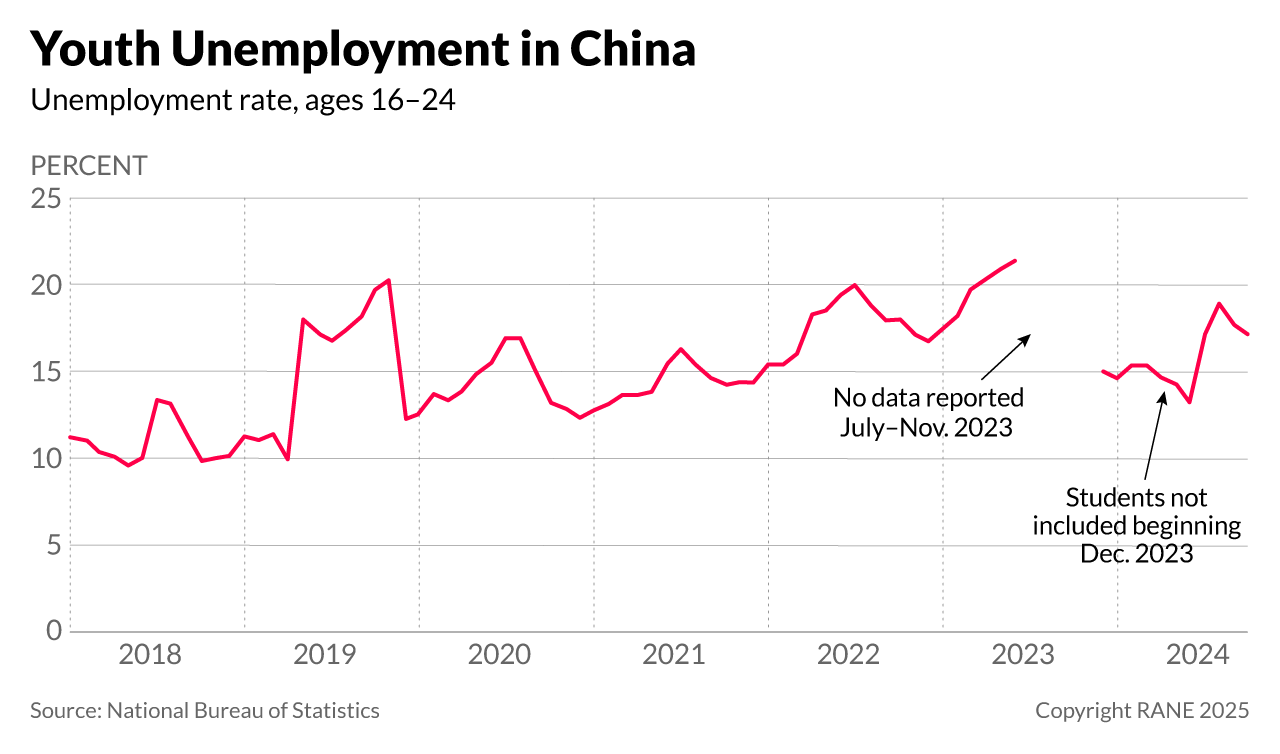

As is traditionally the case in China, protests are driven largely by continuing poor economic prospects, in addition to a public trust deficit in Beijing's governance capabilities post-COVID. Recent unrest is closely tied to China's economic prospects, a pattern that has persisted throughout the country's history. In China's most notorious incidence of mass protests, which led up to the 1989 Tiananmen Square Massacre, a major driver of public discontent (alongside the influx of Western ideas about freedom of speech and liberal democracy on college campuses) was rampant inflation, the result of rapid economic growth in the 1980s following two decades of economic stagnation under Mao Zedong. Today, the drivers of unrest are primarily youth unemployment (spurring unrest on college campuses) as well as slowing wage growth and a stagnating real estate sector (where 70% of household wealth is estimated to be stored). There is also lingering distrust in the government following three years of COVID-19 lockdowns, compounded by a burned-out work culture wherein young Chinese workers are increasingly inclined to "lie flat" and opt out from the proverbial rat race. This is directly related to high youth unemployment and stagnating wages, whereby many young Chinese workers feel disillusioned and see little reward for traditional career ambition, which directly contradicts Beijing's policies aimed at raising worker and industrial productivity in the face of geopolitical competition with the West.

- China's urban youth unemployment rate (among those aged 16-24) steadily rose from 11% in 2018 to 21% in June 2023, after which the government stopped publishing data on the phenomenon for months and then changed its calculation to exclude students looking for work. Even with this more restrictive definition of unemployed, the trend of steadily rising youth unemployment persists, rising from 15% in December 2023 to nearly 20% in January 2025, while overall unemployment (aged 25-59) remains stable at about 4%-5%.

- Since the end of zero-COVID, wages have lagged, whether measured by hiring salary or overall wage growth. In the three years prior to COVID-19, quarterly growth in hiring wages across 38 major cities averaged 5% year-on-year, according to Bloomberg data. For the three years of the pandemic (2020-22), that figure averaged 6.6%, buoyed partly by an uptick in Chinese export activity. By contrast, in the seven quarters from Q1 2023 to Q3 2024, hiring wage growth averaged just 0.07%, with Q3 2024 registering at -0.6%. Similarly, wage growth averaged 7.6% in the three years pre-COVID, 5.3% during the pandemic, and 5.2% in the seven quarters from Q1 2023 to Q3 2024.

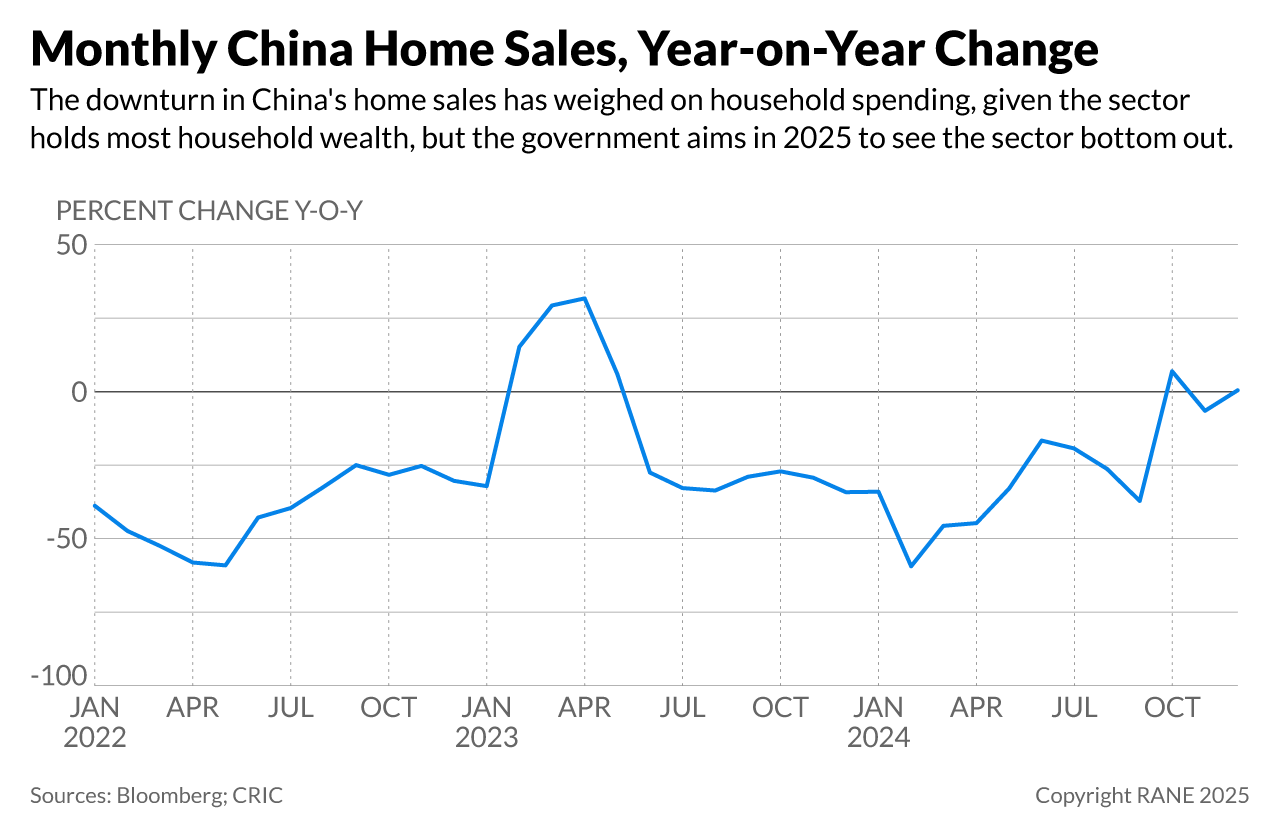

- Real estate activity has significantly shrunk since Beijing instituted the Three Red Lines policy of debt limits in August 2020 to reduce the risk of a Chinese financial crisis. This spurred myriad developer defaults starting in Q4 2021. Real estate sales dropped 31% in 2022, sank another 35% in 2023, and sat at 0% growth in 2024. The 2024 figure preliminarily suggests a bottoming out of real estate, but major developers continue to struggle. Vanke was formerly one of China's largest and most financially stable developers, but it required a 3 billion yuan (about $383 million) cash injection in February to pay its monthly debts and may need another 30 billion yuan for the rest of 2025.

- Retail sales activity has slowed too, indicating the drop in consumer sentiment and lower overall confidence in economic conditions. In the three pre-COVID years (2017-19), monthly retail sales growth averaged 9.1% year on year. In the next three years of the pandemic (2020-22), the average was 3.0%. And in the two years immediately post-COVID (2023-24), this averaged 3.5%.

Persistent economic challenges, coupled with Beijing's tightening control over society and the economy, will likely continue to fuel social discontent in China, with the precedent of the policy concessions amid the White Paper protests increasing the potential for future unrest. Economic conditions driving protests are unlikely to significantly improve in the next few years, as U.S. trade restrictions will weigh on Chinese exporters (whose top market is the United States) and related employment, which is heavily skewed toward younger workers, given the physical rigor of factory work. Even if China's real estate sector stabilizes, it remains highly unlikely that it will again become a major vehicle for household investment. This prospect is due to the difficulty of recreating the illusion of an ever-profitable investment avenue now that it has been shattered. But it is also partly by Beijing's design, as the purpose of Three Red Lines program was to reframe real estate from an investment to a family necessity; as Xi's common refrain goes "housing is for living in, not for speculation." These two developments will also continue to depress wages and consumption, which heighten the sense of worker and household grievances and contribute to protests. As for growing youth unemployment, aside from the issues with exporters and real estate, this phenomenon is also partly structural, driven by a mismatch between the masses of youth pursuing college degrees (especially in engineering and computing technologies) and the Chinese labor market's growing need for skilled and unskilled blue-collar and care workers. Unrest is also driven partly by the precedent of the White Paper protests, which both revealed the extent of popular discontent with government and highlighted that mass public action can yield quick policy results after Beijing's rapid abandonment of zero-COVID, encouraging future protests. Moreover, the Party's commitment to centralization of governing power, a firmer state hand in markets and greater political guidance over everyday life (e.g., guidelines on parenting standards and greater involvement of party committees in private enterprise) remains strong under Xi, so new economic and societal burdens on households are likely to emerge.

- One of the top arguments against the prospect of renewed mass protests in China is the lack of a significant enough trigger to galvanize and unify public opinion against the government, like the Urumqi apartment fire that triggered the most intense wave of the 2022 White Paper protests, but only after three years of COVID-19 lockdowns. But the Kaifeng bike rides and the Pucheng vocational school protest show that when lacking a major trigger, having significant enough latent public discontent can still serve to build demonstrations into the tens or hundreds of thousands.

Should major protests reemerge in China, they are still unlikely to threaten the survival of the Communist regime thanks to its extensive security apparatus and censorship system, but they would again likely drive policy change, including eased economic reforms and large-scale stimulus measures. The response by authorities to the White Paper protests, the Kaifeng bike rides and the Pucheng vocational school protest show that the Party wields a highly capable internal security apparatus to curb protests as well as an extensive online censorship system to control the public narrative and prevent grassroots regime change efforts. Still, a new, major round of protests — potentially triggered by the default of another large real estate developer or massive layoffs at any number of private export manufacturers — could drive Beijing to ease up on economic reforms, aimed at deflating debt bubbles and upscaling to a high income economy based on consumption and advanced industries. In the face of major unrest, Beijing could be forced to double down on efforts to bolster employment, wages and overall economic activity. This could involve large-scale consumer handouts via digital currency or significantly strengthening labor and wage laws to the benefit of workers and using anti-corruption and anti-monopoly investigations to punish businesses that fail to comply. Beijing could also launch another round of massive, state-funded construction (akin to China's response to the 2009 Great Financial Crisis), e.g., by raising the scale of special purpose bonds issued to local governments to build telecom, water management and other infrastructure. In addition, Beijing could conduct massive bailouts of indebted real estate developers in a desperate bid to revive investment activity and consumption, even if it once again encourages speculation.

A policy shift driven by future protests could endanger Xi's tenure or exacerbate China's tightening information environment, depending upon Beijing's management of protests and the scale of its policy U-turn. Beijing's likely economic responses to future protests would rapidly inflate state debt and delay much-needed economic reforms for years. If mismanaged — such as if Beijing intervenes too slowly to stop layoffs and financial contagion spreading across provinces and causing widespread defaults — the combination of massive protests and the abandonment of economic reforms could lead to Xi's stepping down as general secretary, whether by choice or by internal pressure from other top leaders in the Politburo. This could create an opening for a laxer leader to succeed Xi who eases up on efforts to bolster Party control over society. Still, China's myriad internal and external pressures would prevent the rise of a true liberal reformer. Instead, a milder version of Xi committed to more gradual economic reforms and a more cooperative approach to foreign affairs, for example, is more likely. Alternatively, if the scale of disruptive protests is smaller and Beijing's subsequent adjustments to economic policies subtler, Xi's position would likely be secure and he would continue to rely on relatively minor economic concessions and anti-corruption authorities to protect his unitary rule. He would also exacerbate China's information opacity problem by upping online censorship and further restricting the publishing of economic and demographic statistics (such as workers by industry, real estate sales or wage growth) to reduce the appearance of political and economic hardship in China. This would make it harder for foreign businesses to make informed, long-term investments in China — impeding China's investment-fueled movement up the manufacturing value chain — and could erode the efficacy of Beijing's economic policymaking as statistics become even more focused on propagandistic signaling than on reflecting reality.