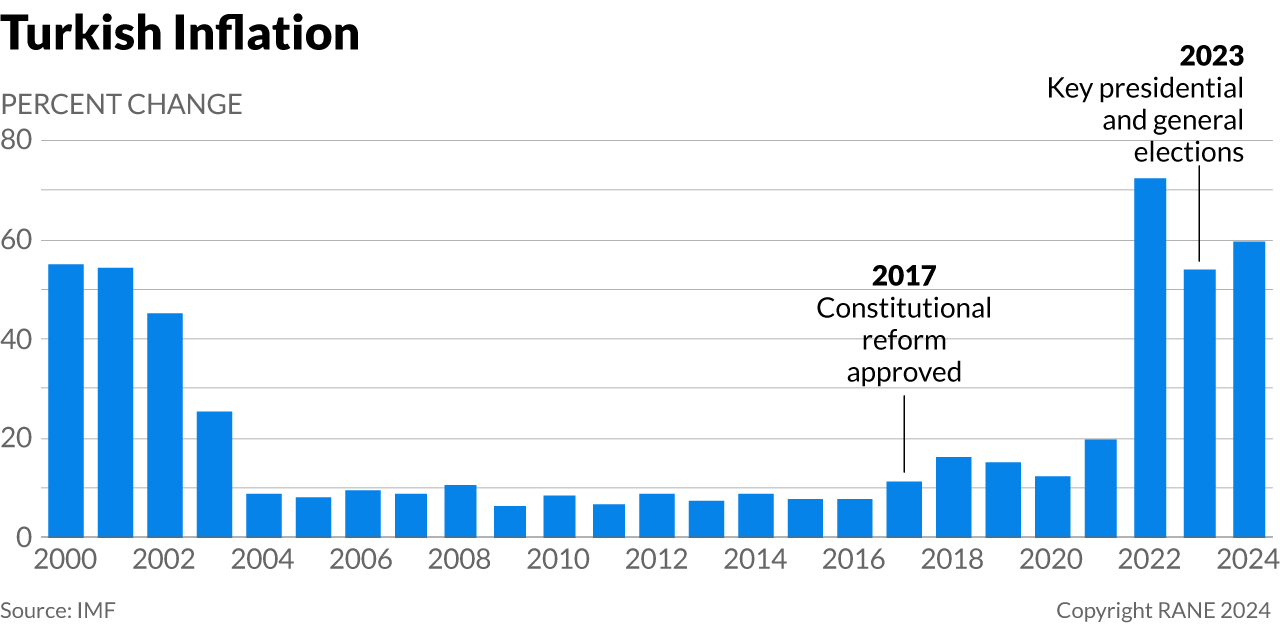

Turkey's technocratic economic strategy will likely continue to slow inflation in the medium term, but Ankara will be tempted to politicize the central bank as the 2028 general election nears, potentially returning Turkey to economic instability and risking a power shift. Turkey's inflation slowed for the first time in seven months in June 2024, declining to 71% year on year from 75% in May. The consumer price index also slowed from 3.4% in May to 1.4% in June, another sign of cooling inflation. At the news, Finance Minister Mehmet Simsek declared, "The age of disinflation has begun." This change is the result of the technocratic economic strategy Simsek has overseen since taking over as finance minister in July 2023, when he was given a mandate to break the cycle of inflation driving down the value of the country's currency, increasing the costs of imports and eroding the standard of living. Meanwhile, President Recep Tayyip Erdogan suggested that disinflation "had just begun" in comments made only a few days after the data was released, a sign that, at least for now, Erdogan would not pressure the central bank to change its tight monetary policy. However, questions remained about how long Erdogan and his government, famous for supporting low interest rates despite their effect on inflation, would remain hands-off.

- Turkey's inflation rate soared in 2021-22 after the Russian invasion of Ukraine affected food and energy prices and the COVID-19 pandemic disrupted supply chains amid Turkey's loose monetary policy. As a result, inflation went from around 21% year on year in November 2021 to almost 85% a year later.

- Starting in 2019, Erdogan began firing a series of central bank heads who contravened his views on economic policy. Meanwhile, Erdogan pushed the bank to cut interest rates and maintain a loose monetary policy as his party tried to maintain power through a series of key elections, including municipal votes in 2019 and national votes in 2023. After winning the national election in 2023, Erdogan appointed Simsek to implement an orthodox economic policy that would embrace a tighter monetary policy.

The Turkish government's current support for orthodox monetary policy is part of a strategy to improve economic conditions ahead of national elections in 2028. The ruling Justice and Development Party, or AKP, succeeded in taking power in 2002 in part because the Turkish governments in the 1990s could not defeat record-high inflation, which peaked at 105% year on year in 1994 and did not decline below 50% until after the AKP's victory in 2002. However, in recent years the AKP has steadily lost its share of seats in the National Assembly — from 295 members of parliament in 2018 to 264 in 2024, well short of a 300-seat majority — amid defections, voter fatigue, economic struggles and policy missteps. Erdogan is also term-limited under the current 2018 constitution, and there is no clear successor to his rule after 22 years as party head and national leader. As a result, the AKP and Erdogan are attempting a myriad of political strategies to entrench the party's power and secure Erdogan's legacy. These strategies range from embracing Simsek's orthodoxy to improve macroeconomic conditions ahead of 2028's election to negotiating with smaller opposition parties to secure the supermajority needed for constitutional reforms and/or a snap national election that might extend Erdogan's rule or smooth the path for his chosen successor. Amid these maneuvers, the AKP is incentivized to continue following a tighter monetary policy to bring inflation back down and stabilize the lira, even if these measures are unpopular, because there are no major elections between now and 2028 that could upend the AKP's control. Meanwhile, the AKP appears to have concluded that despite the victories of the opposition Republican People's Party, or CHP, in major cities like Istanbul and Ankara in municipal elections, the opposition is still too divided to expand on these successes to threaten the party nationally.

- Under Turkey's 2017 constitution, which transformed the government from a parliamentary republic to a presidential one, presidents are limited to two full five-year terms, though a president could theoretically extend their second term by calling early snap elections. However, calling elections requires support from three-fifths of the National Assembly, or 360 lawmakers, and the current government coalition only has 319 votes.

- Although Erdogan said in March that this is his "final" presidential term, AKP officials have tried opening talks with smaller parties about constitutional reforms. However, this process also requires a three-fifths majority in the National Assembly to proceed, and since most opposition parties reject a reform process designed to benefit the AKP and Erdogan, a reform to extend presidential term limits is unlikely to pass.

- Erdogan and the AKP previously favored a looser monetary policy in part to make the lira cheaper to drive up Turkish exports, produce jobs, increase economic growth, boost foreign tourism and attract foreign investment in a heated economy. This policy also appeased Islamists (including Erdogan) who see interest rates as un-Islamic. However, the country struggled to attract positive inflows, particularly in foreign direct investment, and since 2009 has been unable to attract beyond 2% of gross domestic product in net inflows.

As 2028 approaches and disinflation declines, the government will pressure the central bank to increase the pace of growth again, potentially eroding the bank's independence, the struggle against inflation, economic stability, and the AKP's chances of maintaining power. If Erdogan does not run in 2028, the AKP may struggle to transfer the outgoing president's popularity to his successor. Rather, the candidate may have to run on the AKP's overall party legacy, which will include its recent economic management. Should macroeconomic conditions provide an unfavorable political narrative for the party and its presidential candidate, the government could lean on the central bank to manufacture high growth even at the cost of increased inflation, the erosion of the lira's value and reduced foreign exchange reserves. This pressure would run up against the central bank's independence and might lead President Erdogan to fire its chief until he finds a suitable leader willing to cooperate with the government's political aims. As a result, the country's economic strategy might return to its previous patterns of favoring low interest rates and/or monetary expansionism to increase economic growth, even if that growth causes high inflation, produces inequitable results, or makes imports increasingly unaffordable for many Turks. If such conditions occur, they would endanger the AKP's control of the government in the 2028 general election, opening the door for the opposition to take the presidency and/or the National Assembly.

- Turkey's high cost of living may be one major issue in the 2028 election, and the government would seek to combat it by raising wages, despite risks of stoking inflation or slowing disinflation. The government might also utilize subsidies and tax cuts to win support despite the overall negative impact on the national budget.

- There is currently no clear front-runner to succeed Erdogan, though Selcuk Bayraktar, the CEO of the defense company Baykar, is often speculated to be in the running. With no political background, someone like Bayraktar would benefit from favorable economic conditions to win the presidency.