Turkey's economy has largely had a good run under the leadership of President Recep Tayyip Erdogan's Justice and Development Party (AKP), which came to power in 2002. Following the country's currency crisis in 2001, the AKP faithfully implemented and successfully completed two successive International Monetary Fund (IMF) programs between 2002 and 2008, which saw stable and, by Turkish standards, low inflation. Economic growth averaged more than 7% during this time, and has averaged more than 5% annually over the past two decades — putting Turkey in the category of high-growth emerging economies, comparable with Asia's top performers.

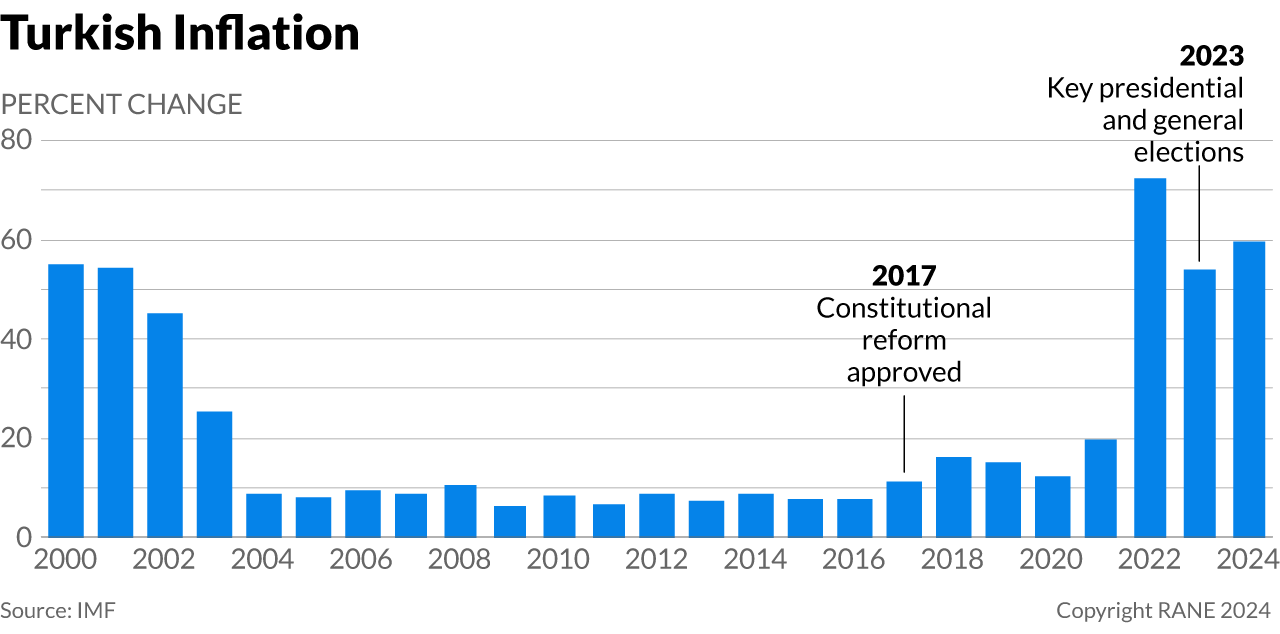

In the past few years, however, the country's continued strong growth was accompanied by high and increasing inflation and a deterioration of Turkey's international financial position. This coincided with the growing centralization of Turkey's political system following the 2017 constitutional reform, which consolidated power in the hands of the Turkish president and, in turn, increased Erdgon's influence over central bank policy. It also coincided with weakening support for the government, which was acutely evidenced by the AKP's painful defeat in municipal elections held in 2019, putting Erdogan and his party on edge ahead of the 2023 presidential and general elections.

With Erdogan concerned over his reelection prospects, and with the 2017 constitutional reform giving him greater sway over monetary policy, short-term political calculus began dominating Turkey's economic policymaking. To bolster its waning popularity ahead of the 2023 national ballot, Erdogan's AKP-led government started increasing pressure on the central bank to pursue a more inflationary policy to stimulate economic activity and employment. During this time, Erdogan also removed several central bank presidents, further showing how political centralization and the concomitant weakening of institutions can be exploited for political-electoral reasons at the expense of longer-term economic stability.

Turkey's Shift to Unorthodox Monetary Policy

The Central Bank of Turkey (CBRT) began shifting toward a more unorthodox monetary policy as early as 2010, mainly in an attempt to cope with strong financial inflows and exchange rate appreciation. This led the CBRT to continuously miss its inflation target, but it also made Turkey stand out compared with its top-tier emerging economy peers where inflation was significantly lower (e.g. Brazil, Mexico, and South Africa). But after the 2017 constitutional reform significantly consolidated power under President Erdogan, Turkey's monetary policy turned decisively unorthodox and inflationary. While inflation was high between 2009 and 2016, it typically hovered around 10%. In 2018-19, inflation reached the mid-teens, before exceeding a staggering 70% in 2022 in the wake of the COVID-19 pandemic.

Growing Imbalances and Weakening Institutions

Increasing political centralization and a shifting political-electoral calculus help explain the worsening quality of Turkey's economic policies in recent years. When the AKP first came to power in 2002, it gained an absolute majority in Turkey's parliament. Economic conditions were improving following the country's 2001 financial crisis. The AKP won absolute majorities in 2002, 2007 and 2011, as well as in 2015 following a surprise loss and a repeat parliamentary election.

Although Erdogan dominated Turkish politics and the AKP, until the mid-2010s, other senior AKP figures retained a degree of influence, at least over economic policy. Many of these party figures supported orthodox economic policies. The AKP expanded its influence by gaining control over institutions (e.g. the presidency) and by weakening institutional opponents (e.g. the military and judiciary). The 2017 constitutional reform also led to a very significant centralization of power in the hands of the president and a weakening of the independence of the central bank. Following the IMF-led economic and structural reforms in the early 2000s, the Central Bank of Turkey (CBRT) was legally independent. The CBRT's failure to maintain low inflation and meet its inflation target can be interpreted as the consequence of the government's increasing pressure on the bank, or it can be seen as the bank pursuing unorthodox policies to stem capital inflows. Following the 2017 constitutional reform, however, the CBRT lost complete control of inflation due to Erdogan's new ability to fire the bank's governor and appoint loyalists in their place (which he has since done repeatedly). At the same time, Erdogan sidelined remaining senior AKP officials, giving him unprecedented sway over his party. The constitutional shift and the sidelining of potential internal AKP opposition effectively gave Erdogan free rein. For Erdogan, the strengthened presidency made it all the more imperative that he be reelected in 2023 — something that he and his party's waning popularity threatened by raising the prospect of an opposition victory. In this sense, the constitutional reform created the ability and increased the incentives to pursue less orthodox, pro-growth economic policies aimed at winning over more voters ahead of the 2023 elections.

In the years that followed the constitutional reform, monetary policy became significantly more inflationary and the government began to resort to unorthodox policies in order to limit the negative effects of easy monetary policy on inflation, currency valuation and capital outflows. While the CBRT failed to meet its 5% inflation target throughout the 2010s, often by a small margin, Turkey's economic policy and inflation took a decisive turn for the worse in 2017-18, as the pressure on the CBRT to pursue expansion increased substantially. The central bank has had six different governors just since 2019 — several of whom were sacked or otherwise pushed out of office for failing to align with Erdogan's preference for low interest rates, including Murat Uysal in 2020 and Naci Agbal in 2021. The appointment of Sahap Kavcioglu (2021-23) to CBRT governor, who was aligned with Erdogon's desire to pursue an easy monetary policy, then set the stage for even more inflationary policies.

Turkey's economic policy also became much more interventionist with the appointment of Berat Albayrak (2018-20) as finance minister, who happened to be Erdogan's son-in-law and had no policy-making experience. Albayrak failed to regain market confidence and was ultimately replaced by a slightly less unorthodox finance minister, Lutfi Elvan (2020-21). But Elvan's tenure also proved to be short-lived, due likely to disagreements with Erdogan over the course of economic policy. Ultimately, sustainable policies aimed at maintaining macroeconomic stability were at odds with Erdogan's political-electoral calculus, which focused on pump-priming the economy in view of the important 2023 national elections against the backdrop of the president and his party's weakening popular support.

Playing the Phillips Curve

The so-called Phillips curve postulates an inverse correlation between unemployment and wage growth (or, by extension, inflation), though economists agree this inverse relationship only holds in the short term. In the years leading up to Turkey's 2023 elections, the government exploited the Phillips curve by pressuring the central bank to shift toward pro-inflationary policies (i.e. maintaining low interest rates despite rising inflation) in the hopes of lowering employment and bolstering economic growth ahead of the ballot. This is why political economists recognize the need to establish independent, inflation-righting central banks to limit the ability of elected politicians to exploit the Phillips curve for short-term electoral benefits at the expense of longer-term economic and financial stability.

A Return to Greater Orthodoxy — For Now

In the run-up to Turkey's May 2023 elections, inflation reached 85% year-on-year in November 2022. But the government's pre-election focus on lowering unemployment and increasing economic growth at the expense of higher inflation appeared to work in its favor at the ballot box, as Erdogan won the 2023 presidential race, while his AKP maintained its majority in the concurrent parliamentary elections.

Since being reelected for another five-year term as president, Erdogan has appointed a new economic team headed by finance minister Mehmet Simsek, and tasked with reducing inflation and stabilizing the economy. Although years of inflationary monetary policy had helped maintain high economic growth, the consequent worsening of Turkey's cost of living crisis had become deeply unpopular. And with no national elections on the horizon, Erdogan also had more political breathing room to pursue such a policy shift, even if it meant job losses and an economic slowdown in the short term, while longer-term even higher inflation would have weighed on the president's popularity

Shortly after the May 2023 elections, the reelected AKP government began rolling back some of its interventionist economic policies, letting the exchange rate adjust while tightening monetary policy. Thus far, the adjustment has been fairly gradual. The CBRT raised its policy rate in June 2023, just after the elections, with a modest hike to 15% in the context of 40% year-on-year inflation. It took until March 2024 for the policy rate to reach 50%, but in the meantime, inflation had reached 70%, leaving real interest rates in deeply negative territory. Moreover, a minimum wage hike in January 2024 was not exactly conducive to rapid disinflation. This suggests that political considerations remain as important as economic ones.

Stabilizing the Economy Amid Centralized Political Power

It is difficult to say whether the lack of more aggressive adjustment is due to political constraints faced by Erdogan's new economic team or by a conscious decision to avoid a potentially destabilizing ''shock therapy'' in light of potential financial vulnerabilities in the banking sector. The IMF, for one, has highlighted ''high and growing'' banking sector risks in Turkey due to rapid credit growth and weakening of supervision.

Equally important, however, is the fact that Turkey's economic policy is subject to the decisions of a powerful president who now faces even fewer checks and balances following the 2017 constitutional reform. This sets Turkey apart from other large emerging economies, such as Brazil, Mexico, India and Indonesia, which have far more robust institutions and, in turn, greater policy certainty.

In less centralized political systems, significant shifts in economic policy can be expected when, for example, a different political party comes to power; and it is also often easier to gauge what that shift will look like based on that party's policy platform and past actions. But in Turkey, where power is highly concentrated, economic policies are much harder to predict because they are more beholden to the whims of the president (and their political calculus), and less to institutional checks and balances. The outlook for the Turkish economy thus depends on what authorities do today, as well as what they can be expected to do in the future — something that is far trickier to speculate and can change quickly based on personal or political changes of heart.

Looking Ahead

So what does this all mean for Turkey? If the above analysis is correct, macroeconomic and especially monetary stability in the country will be difficult to maintain. Electoral-political incentives will continue to see Turkish presidents wield their power over the central bank to exploit the tradeoff between economic growth and broader inflation, likely resulting in stop-and-go policies akin to what the United Kingdom experienced in the 1960s and 1970s.

Against this backdrop, Turkey's new economic team will also struggle to regain and maintain investor confidence. This is because if stable inflation depends on individuals appointed by the president, low inflation and broader economic stability will continue to hinge on that president's political calculus, which can and will likely change in the run-up to important elections, thereby leaving investors cautious. As a result, Turkey will face higher interest and financing costs than it would otherwise under a regime where the central bank is institutionally independent and committed to low inflation and monetary stability.

But the recent shift toward greater orthodoxy will help improve economic fundamentals and reduce downside financial risks. The gradual rebuilding of institutional guardrails around Turkish economic policy would boost domestic and foreign investor confidence and help the country exploit its significant economic growth potential in the context of greater economic stability. Indeed, on June 4, the country's Constitutional Court invalidated a presidential decree issued in 2018 that authorized the president to sack CBRT governors and force the central bank into an inflationary monetary policy. If an institutional process is put in place that is conducive to economic technocrats being appointed to the central bank leadership, the outlook for longer-lasting economic stability will improve in Turkey, which has been pursuing a fairly stability-oriented fiscal policy over the past two decades.