A 3D rendering of the European Union's flag and a gas valve on the Nord Stream natural gas pipeline.

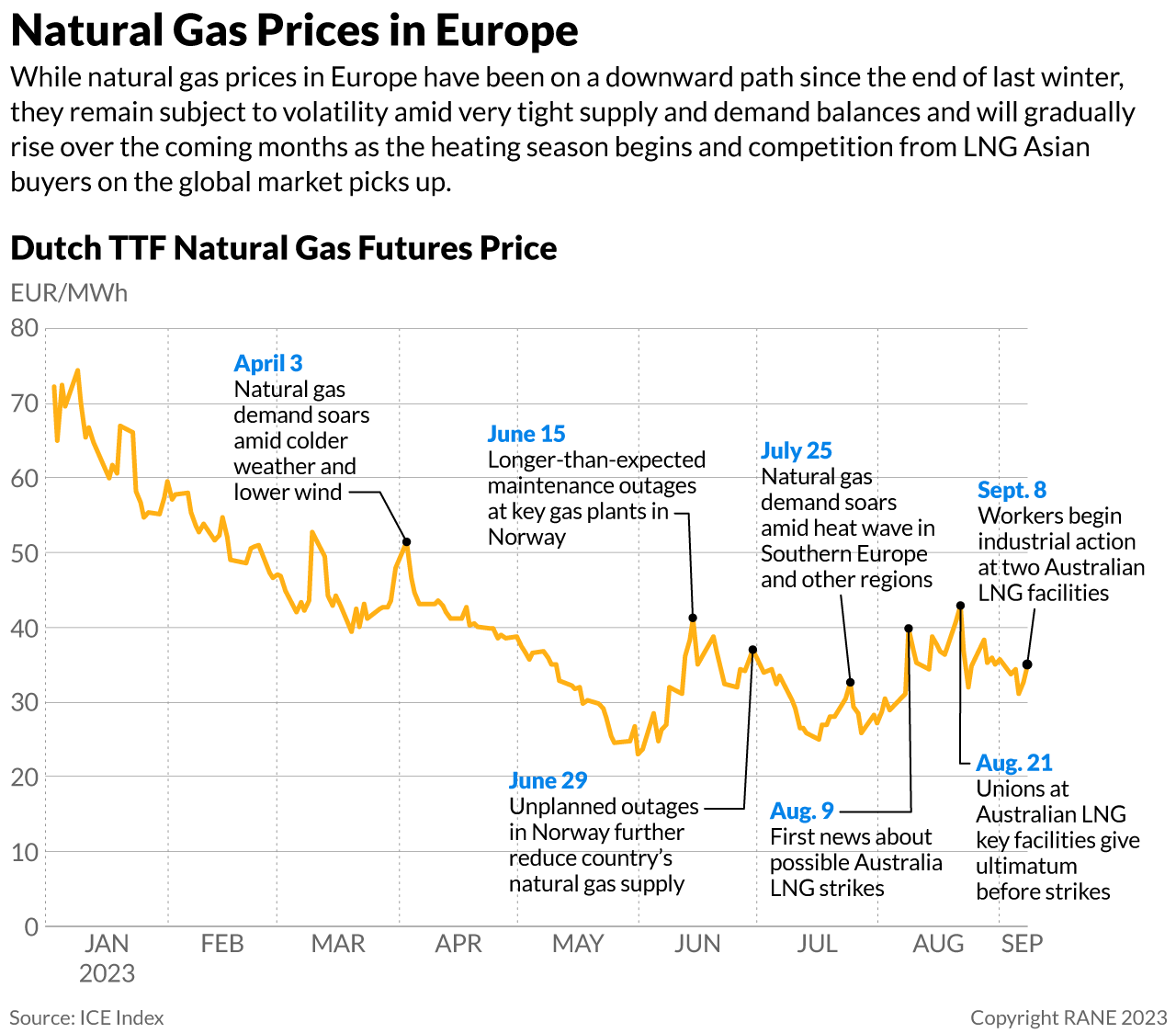

Europe will avoid an outsize surge in energy prices this winter thanks to record-high storage and lower consumption, but a delicate supply and demand balance means price shocks remain possible. On Sept. 14, striking workers at U.S. oil and gas giant Chevron's Wheatstone and Gorgon liquified natural gas (LNG) plants in Western Australia state began escalating action and threatened to increase stoppages over the "coming days and weeks." Industrial action at the two sites, which together account for 5-7% of global LNG supply, could escalate to a total halt or hours-long work stoppages for up to two weeks. European energy prices grew volatile at the news, as any prolonged strike action at the facilities could temporarily remove roughly 1 million tons of LNG from the global market, forcing Asian buyers to intensify competition with Europe on the global spot market. Separately, seasonal maintenance on Norway's gas infrastructure continues to experience delays across several key assets, including the giant Troll field, which means already lower-than-usual exports will remain subdued for longer than expected. However, operations at the Freeport LNG plant in Texas (which alone accounts for 20% of U.S. LNG exports and about 5% of global supply) restarted on Sept. 14 following an unplanned outage over the previous week, preventing a price rally. In fact, European natural gas prices fell 3.5% in intraday trading following the news, offsetting traders' concerns over supply disruptions in Australia and Norway.

- Workers began partial strikes at Chevron's Wheatstone and Gorgon plants on Sept. 8, and the most recent threats follow a breakdown in talks between unions and the company over pay and working conditions. Australia's regulator is expected to start mediating negotiations between Chevron and labor unions on Sept. 22, which could end the stalemate earlier than expected. Unions at Australian energy company Woodside's North West Shelf LNG facility also made similar demands, but the facility averted a strike by reaching a deal on Aug. 24.

- Norway has become Europe's key natural gas provider, along with the United States, after Russia significantly curbed supplies to the Continent following its invasion of Ukraine.

- European gas benchmark Dutch TTF fell to 35.5 euros per megawatt-hour (MWh) ($11.2 MMBtu) on Sept. 14, offsetting earlier gains in the day. As of Sept. 18, prices remain stable at 36.5 euros per MWh.

Europe's recent efforts to reduce demand and increase supply have stabilized energy prices. Following Russia's invasion of Ukraine in 2022, Moscow decreased the amount of natural gas it piped to Europe by billions of cubic meters, but a lack of infrastructure and various logistical hurdles made it difficult to reroute that gas to other buyers. As a result, the total global supply of natural gas decreased at the same time that Europe massively increased imports of global LNG to replace missing volumes of Russian pipeline gas, making the market extremely tight and causing prices to skyrocket. Europe's need for natural gas was particularly acute amid low storage inventories before the start of the heating season last October. This year, however, Europe has managed to keep importing LNG and almost entirely fill its natural gas inventories in preparation for the coming winter well ahead of schedule. These high storage levels will slow European gas purchases in the coming months, limiting competition with Asian buyers that are still working to build their own inventories and reducing price pressures. Additionally, Europe's natural gas prices have continued to decline since the spring thanks to a milder-than-usual 2022-23 winter and greatly reduced industrial consumption that helped the Continent achieve a more optimal storage cycle throughout 2023.

- Before its invasion of Ukraine, Russia exported around 155 billion cubic meters (bcm) of pipeline gas and about 16 bcm of LNG to Europe, accounting for 40% of the European Union's total gas imports. Pipeline gas exports to Europe, now limited to flows through two routes via Ukraine and Turkey, fell to 62 bcm for the whole of 2022 and have declined to about 18 bcm so far in 2023. Meanwhile, Russian LNG exports to Europe have increased, nearing 12 bcm in the first half of 2023, down only 1% from the same period last year but up 7% from the first half of 2021.

- Meanwhile, the European Union's total LNG imports increased by 70% to 170 bcm in 2022, making it the world's leading importer of the fuel. A switch to alternative sources of energy, diversification of supply, and a reduction in overall gas consumption further helped Europe drastically reduce its reliance on Russian gas. In 2023, Europe managed to meet the key energy security target of filling 90% of total storage capacity 10 weeks in advance, reaching its November target in mid-August. Natural gas storage facilities in the European Union are now almost 94% full, according to the latest data from Gas Infrastructure Europe.

Despite Europe's efforts, recent price volatility demonstrates the fragility of the Continent's natural gas markets, which may lead to price spikes as the heating season begins. Europe's ample storage and recent efforts to reduce demand and diversify supply mean energy prices are set to increase only gradually as demand for heating picks up in Europe and Asia. And even as these prices rise, they are expected to remain below the levels seen during the 2022-23 winter. However, the global LNG market is set to remain tight until significant new supply comes on stream from the United States, Qatar and other countries beginning in 2026. Additionally, downside risks will increase alongside seasonal demand, and any sign of major demand or supply shocks could cause panic reactions in the market and result in severe price spikes, as seen in recent price swings linked to outages in Australia and Norway. While a repeat of the 2022 energy crisis is unlikely, much higher gas prices throughout the winter remain possible, particularly if temperatures are colder than expected or if there are severe disruptions to supply. A prolonged period of very high energy prices would have particularly severe economic and sociopolitical implications for Europe given a stagnant economy, stubborn inflation, high interest rates and growing war fatigue.

- Potential disruptions to supply include major accidents knocking down key LNG facilities abroad for a prolonged period of time. Sabotage to Europe's energy infrastructure is also possible, and this risk will increase over the winter as Russia searches for other ways to pressure Europe into reducing support for Ukraine, having lost much of its capacity to manipulate Europe's energy market through supply cutoffs.

- Even at full capacity, Europe's storage facilities would only cover 25-30% of typical EU wintertime gas demand, so the Continent will still have to rely on continuous imports of LNG through the winter.

- However, global LNG supply is expected to rise by about 6% in the 2023-24 winter compared with last winter due to the Freeport LNG project's recovery and additional capacity from new facilities in Russia, Mexico, Indonesia and sub-Saharan Africa.