People walk on a street at the end of the workday in Beijing, China, on March 17, 2023.

Despite the post-COVID uptick in economic activity, China's medium-term growth potential will continue to decline, while macro-financial vulnerabilities will remain elevated, which will accelerate efforts to strengthen political oversight of the economy — especially as policymakers try to reduce China's exposure to external economic pressure. Over the past 40 years, Chinese policymakers have proven remarkably adept at maintaining high growth rates while effectively managing financial risks. The government has relied on a mixture of state-led economic development and gradual, market-oriented liberalization. More recently, the government has backtracked on market-oriented reform despite previous commitments to let markets play a ''decisive role'' in economic development. China's political economy model has traditionally proved very effective in terms of mobilizing savings and channeling them into strategic sectors. A combination of financial repression (keeping interests on bank deposits low) and government-guided bank lending provided a cheap and stable source of funding for development-oriented, strategic economic sectors. Today, however, this system is channeling savings into relatively low-productivity sectors, like real estate and physical infrastructure, creating financial vulnerabilities and limiting future economic growth.

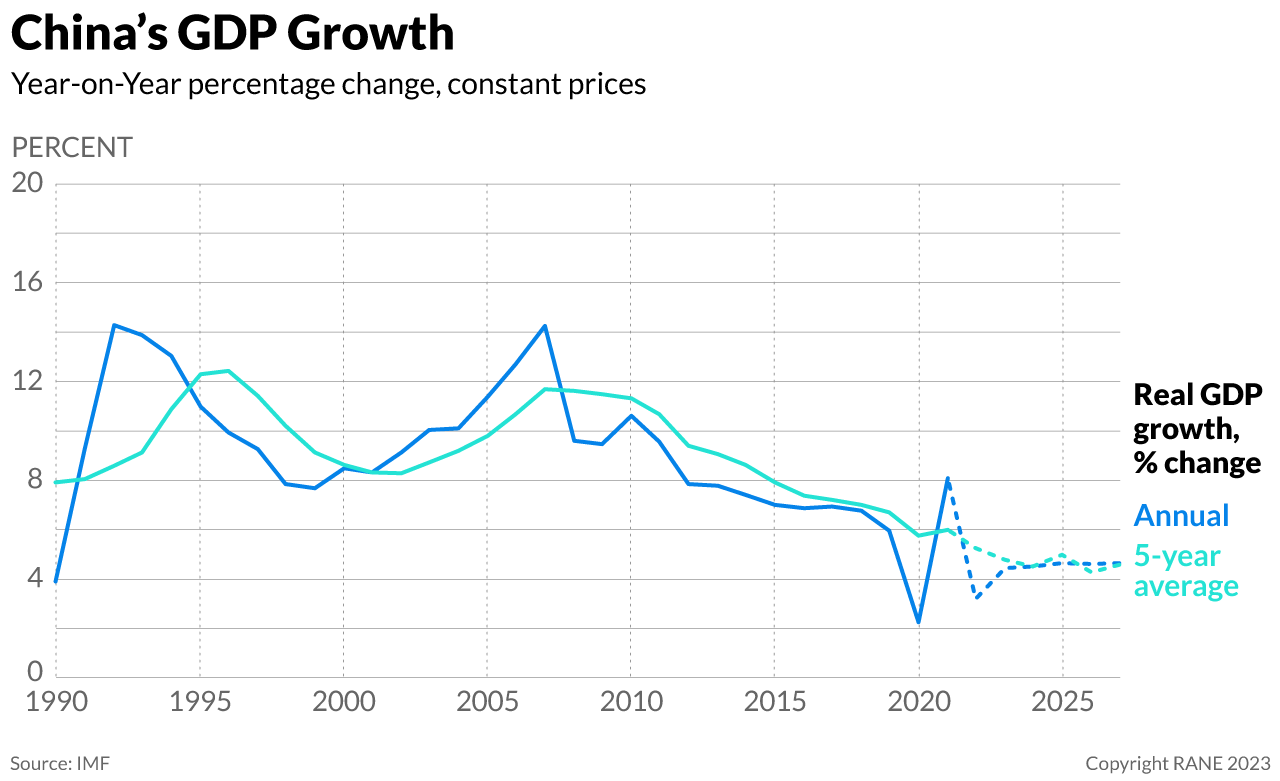

- China's real GDP growth has averaged 8-9% over the past four decades. Recently, however, ten-year average economic growth has slowed to 5%. The government's official growth target for 2023 is ''around 5%.''

- At the Chinese Communist Party's Third Plenum in 2011, China committed itself to letting markets play a ''decisive role'' in the country's economic development. Over the past few years, however, Beijing has increased the role of the government (and thereby the Communist Party) in state-owned enterprises and has announced its intention to do the same in the case of private Chinese companies.

China's traditional approach to economic development has been strained for some time, and the continued failure to reform it will increasingly weigh on the economy's medium-term growth outlook. The International Monetary Fund (IMF) and most private-sector economists expect China's real GDP growth rate will continue to decline, which will put pressure on China's political economy model and financial stability. China's banking system intermediates a large share of total domestic savings, channeling significant amounts of it into the real estate and infrastructure sectors, which then leads to banks holding large financial claims on real estate companies and households. At the same time, local-government-backed funds — so-called local government financing vehicles (LGFV) — also raise funds to finance local infrastructure and housing projects, while local governments in China derive revenue from real-estate-related land sales. This system is highly interconnected, and financial problems in one part of it can quickly cascade through the entire system. Moreover, the system works well as long as there is sufficient demand for real estate and infrastructure, prices continue to rise, supported by solid economic growth, and borrowers are able to repay their debt. Moreover, the system works well as long as there is solid economic growth, sufficient demand for real estate and infrastructure, a continued rise in real estate prices, and borrowers are able to repay their debt. But banks face potentially significant losses if real estate companies are placed under financial distress and mortgage defaults rise. China has experienced a slight uptick in credit losses tied to the real estate sector, following the introduction of greater restrictions on real estate developers. These losses, however, have so far been relatively minor. If real estate prices fall or infrastructure investment proves unprofitable, banks will experience financial losses and LGFVs may be forced into bankruptcy or restructuring. To the extent that these vehicles are backed by local governments, the authorities may then be forced to bail them out at a time when they start to lose revenues from declining land sales. Viewed from a macro angle, ''excess savings'' are being channeled into sectors of the economy that will generate low returns and low productivity growth, which will weigh on China's medium-term economic growth and increase the risks of financial losses.

- Bank loans amounted to 180% of China's GDP in 2022, up from less than 100% in 2008 and 150% of GDP in 2018. An alternative measure of domestic non-financial debt stands at around 300% of GDP, which is extremely high by international standards — particularly for a middle-income economy.

- Land sale-related local government revenue amounts to 2-3% of China's GDP, while LGFV-related debt amounts to about 40%.

Chinese policymakers are fully aware of the significant medium-term economic challenges and macro-financial risks related to overinvestment in real estate and infrastructure, but they will continue to struggle to rebalance the economy. To the extent that policymakers are successful in terms of rebalancing the economy away from overinvestment in real estate, economic growth will slow, unless savings can be put to better use. According to the IMF, China's domestic savings rate amounts to 45% of GDP. It is impossible to reduce the excess domestic savings rate from 45% of GDP to, for example, a more reasonable 35% within just a couple of years without causing major disruptions, the very thing Beijing is trying to avoid. This means there is no such thing as a quick fix to China's economic challenges, leaving Beijing with no choice but to gradually adjust the country's economic model. If Chinese authorities continue to go slowly in terms of reducing the importance of the real estate and infrastructure sectors and limiting concomitant financial risks, financial instability risks will remain manageable due to China's high savings rate, significant control over the financial system and capital controls. Effectively, the entire system will remain backstopped by the government. A precipitous downward shift in economic growth, however, would expose these vulnerabilities immediately; by the same token, a precipitous reduction in real estate and infrastructure investment would lead to a sharp economic slowdown. This is precisely why Beijing has opted for a gradual approach. Such slow and steady policy adjustment will still lead to declining economic growth (and, in turn, increasing — if manageable — financial losses), but it will also make that slowdown more manageable overall.

- Estimates vary, but most put the combined direct and indirect contribution of China's infrastructure and real estate sectors at 20-30% of GDP.

- Non-performing loans (NPLs) stand at less than 2%, but the NPL ratio is a backward-looking indicator.

In light of deteriorating medium-term growth prospects and continued domestic financial vulnerabilities, Chinese policymakers will intensify efforts to limit China's susceptibility to foreign economic and political pressure. In addition to the aforementioned domestic challenges, China is also facing mounting foreign economic pressure — particularly from increasing U.S. investment and export restrictions — that could further hamper its economic growth by targeting innovative, high-productivity tech sectors, such as semiconductor chips, artificial intelligence and quantum computing. To mitigate this threat, the government will accelerate policies geared toward the ''securitization'' of foreign economic relations. In addition, Beijing will press for a more rapid shift toward ''dual circulation,'' a policy focused, among other things, on increasing domestic consumption and reducing supply chain vulnerabilities. But while these policies will help make China's political economy less susceptible to external shocks, they will also further weigh on medium-to-long-term economic growth. Greater state intervention and a lower degree of economic and financial openness will be less conducive to competition, innovation and hence economic growth. Chinese policymakers might be able to halt a slide in economic growth if they strengthen the role of the private sector and limit government interference in growth-oriented, high-productivity sectors. But Beijing is unlikely to offset these securitization measures with further market liberalization, despite such reform being needed to ward off a precipitous deceleration of economic growth that could keep China from reaching high-income status (a phenomenon known as the ''middle-income trap'').

- The IMF expects Chinese real GDP growth to fall below 4% over the next four years. Some private-sector economists expect the growth rate to decline to a mere 3% before the end of the decade.

- Under the leadership of President Xi Jinping, China announced a policy of ''comprehensive national security'' in 2014. In view of intensifying conflict with the United States, the trend toward increased political control will likely continue to limit market-based competition and weigh on productivity and economic growth.

- China is the world's second-largest economy in nominal dollar terms at market exchange rates. It is the world's largest economy in purchasing power parity terms, a more accurate measure of economic size.