The national flags of the European Union’s 27 member states are seen at the European Council headquarters in Brussels, Belgium.

COVID-19’s long-term impact on the EU economy and the lack of a consensus on a bloc-wide banking union mean European banks remain vulnerable, despite extensive institutional and national measures to avoid a banking crisis. Since the onset of the pandemic in early 2020, EU institutions and national governments have implemented several measures to assist the bloc’s banking sector and ensure the availability of credit to companies across the Continent, which has prevented a banking crisis despite the severity of the recession. The measures include cheap liquidity and funding guarantees for banks, softer regulations and the creation of emergency funds for business lending.

- From April 6, 2020, to March 31, 2021, the European Investment Fund (EIF) made 49 billion euro available to banks in order to provide them liquidity and guarantees so that they could support the capital needs of small- and medium-sized enterprises.

- The European Commission made the Coronavirus Banking Package available to European banks and credit institutions on June 27, 2020. This package aimed to provide flexibility in bank lending to businesses and households in the eurozone.

- In April 2020, eurozone and non-eurozone countries also agreed to create a Financial Emergency Fund to provide 540 billion euro in national support for unemployment mitigation schemes, as well as additional support for business lending.

- In order to ensure banks continue providing loans to businesses and households to mitigate the economic fallout from the pandemic, the European Parliament relaxed banking rules related to lending from European banks.

Stimulus programs have also boosted economic growth and reduced the risk of companies and households defaulting on their debt. In addition to helping banks, EU institutions and national governments introduced broader measures aimed at boosting domestic consumption, protecting jobs and increasing investment across the bloc. These measures indirectly helped the banking sector because they somewhat mitigated the economic and financial impact of the pandemic.

- In March 2020, France implemented an exceptional state guarantee of 300 billion euro in loans to businesses.

- Germany created a 600 euro billion economic stabilization fund, available until the end of 2021.

- Italy created the Guarantee Fund for Small and Medium Enterprise, which aimed at assisting companies without any non-performing loans in accessing funding from financial institutions.

- The European Union’s long-term budget increased its flexibility mechanisms to guarantee it has the capacity to continue addressing the fallout from COVID-19.

- In July 2020, the European Union created the Next Generation EU Recovery Instrument, a 750 billion euro fund to finance spending programs across the bloc. Brussels started disbursing money from this fund in July of 2021.

- In 2020, the European Central Bank (ECB) introduced a 1.85 euro trillion Pandemic Emergency Purchase Programme (PEPP) for the purchase of government and corporate bonds.

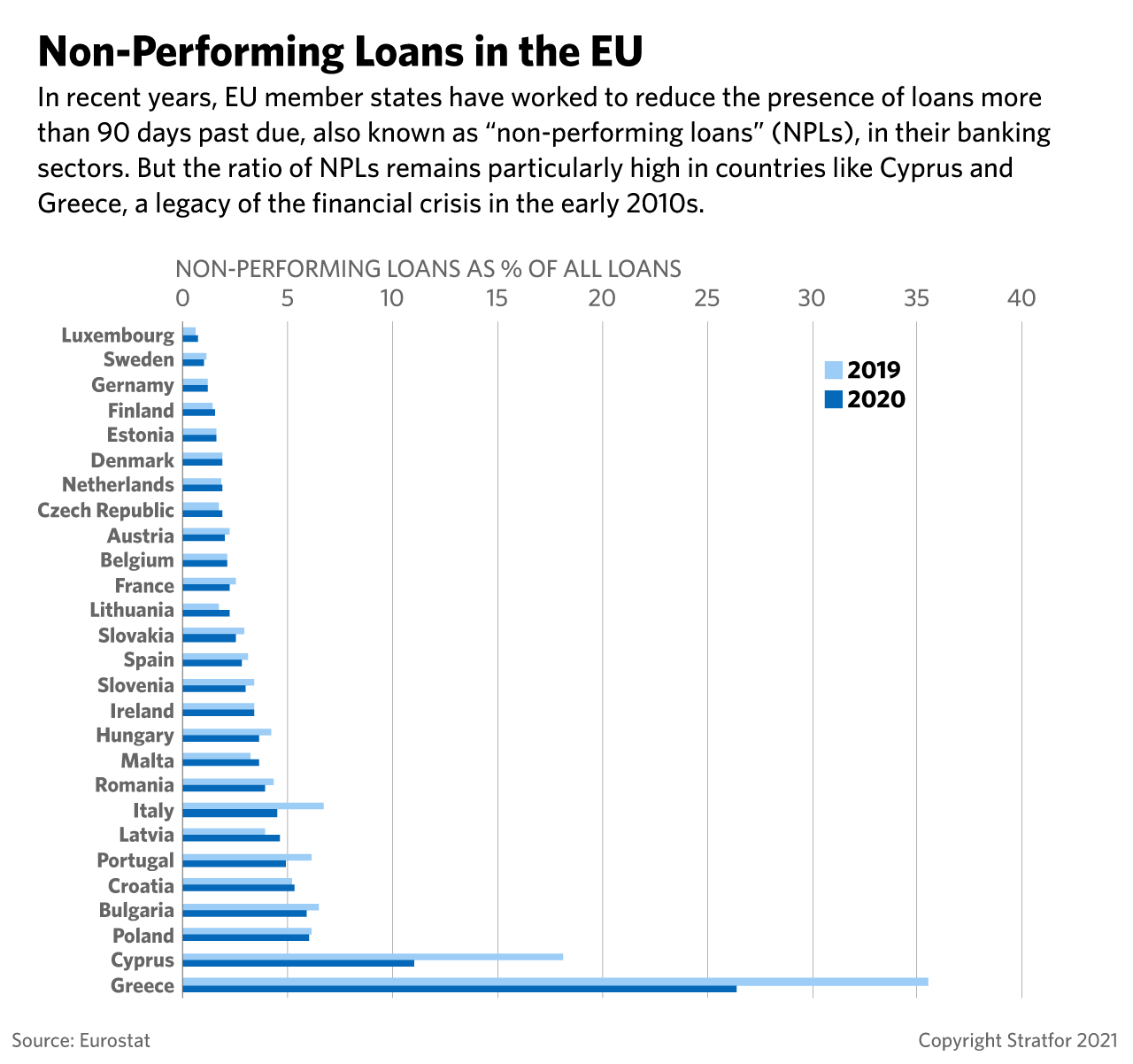

But while economic stimulus and assistance measures have so far shielded the European Union’s banking sector, rising household debt, high unemployment and a group of fragile banks could still result in a future banking crisis. The European Union has avoided a banking crisis following the COVID-19 pandemic, but there are still key weak spots throughout the bloc. In the most recent stress test conducted by the European Banking Authority (EBA), released on July 30, a number of financial institutions were flagged as being weak spots in the European banking sector because of their fragility in case of a prolonged recession in the Continent.

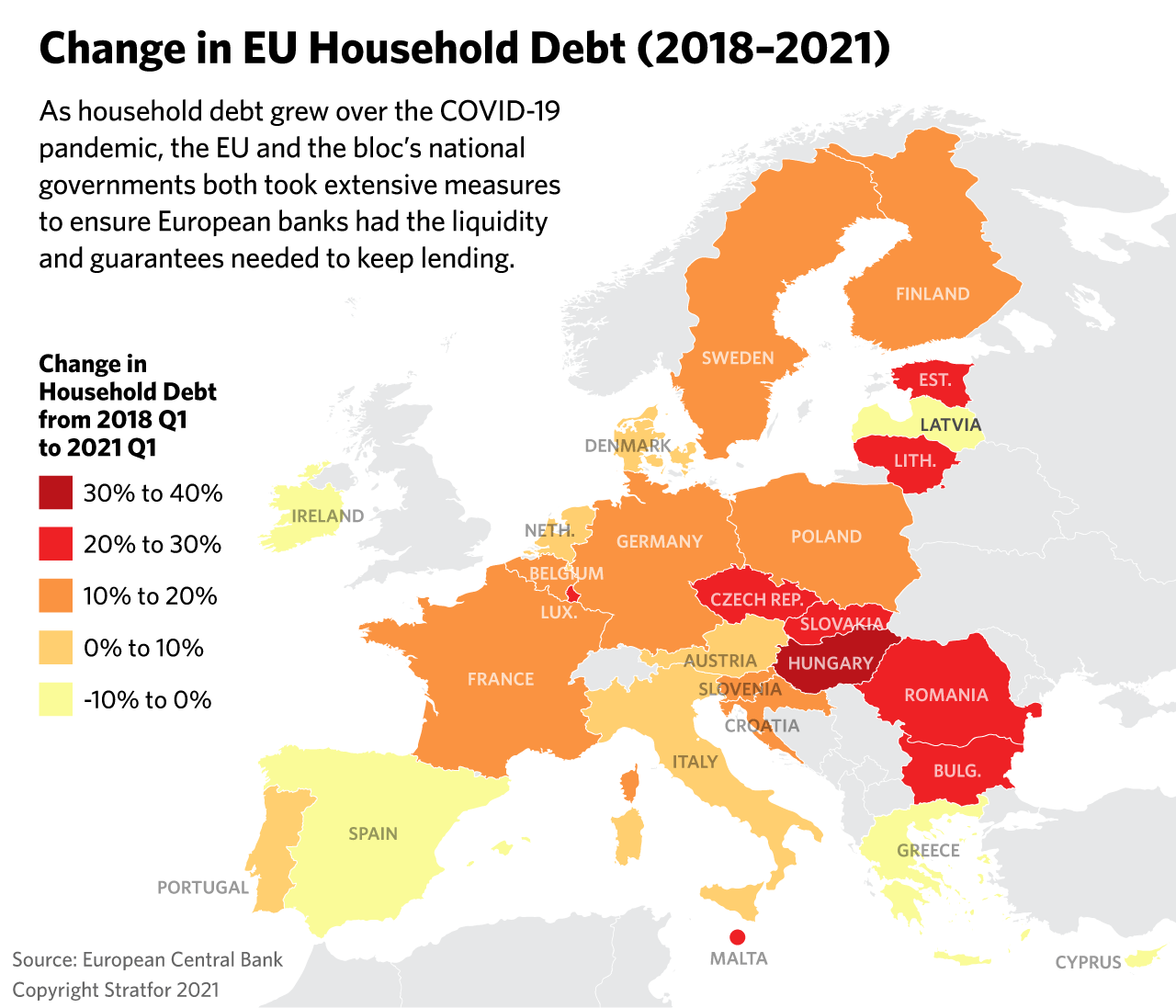

- Household debt rose an average of 9% across the European Union from the first quarter of 2018 to the first quarter of 2021. Unemployment, meanwhile, rose an average of nearly 5% across Europe. This, coupled with the decrease in household deposits and the reduction of household savings across the European Union, signals a potential rise in non-performing loans across the region.

- The EBA’s recent stress test revealed that most European banks are better prepared to deal with a severe economic crisis than they were before the pandemic, but there are still institutions to watch. Germany’s Deutsche Bank AG and France’s Societe Generale SA emerged as some of the weakest large European lenders, as Deutsche Bank’s common equity tier 1 ratio (a key measure of financial strength) fell 620 basis points to 7.4% and Societe Generale’s fell 562 basis points to 7.5% in the worst-case scenario of a prolonged recession. Italy’s Banca Monte dei Paschi di Siena’s capital would be depleted in the case of a long recession, in the adverse scenario presented in the stress test.

The lack of a unified European view on the creation of an EU banking union makes the bloc’s banks vulnerable to economic downturns, debt crises and bank failures. Following the debt crisis of 2008, EU governments proposed to further integrate their banking sectors to make them more resilient to future crises, but the plan has yet to be completed due to fundamental differences in strategic objectives between Northern and Southern Europe. While the Basel Committee on Banking Supervision instigated important first steps, without the completion of a full banking union in Europe, the region’s fragmented banking sectors will remain exposed to financial risk. Without a unitary, centralized mechanism to deal with bank failures and a common mechanism to guarantee deposits in all member states, some countries (like those in Southern Europe) and some specific banks (like those identified in the stress tests) will continue to be perceived as more fragile and therefore more exposed to crises than others, which threatens the overall stability of the EU financial sector.

- Only the first pillar of the banking union, the creation of a single supervision mechanism for EU banks, has been fully completed.

- While the second pillar, the creation of a single resolution mechanism, is theoretically in place, its actual implementation remains controversial. The current banking regulations have not fully found a way to effectively stop the link between European banks and their sovereigns. So long as banks continue to expose themselves to risky sovereign debt, the integrity of the euro area will continue to be undermined.

- The third and final pillar of a complete EU banking union would be the implementation of a European Deposit Insurance Scheme (EDIS), which would guarantee deposits below 100,000 euro of all the banks in the union. But Northern European countries are skeptical about this step, as they argue that financial risk must be reduced before it can be shared. Without EDIS, markets and savers will continue to see the banking sectors of some countries as more fragile and riskier than others, increasing the probability of bank runs during crises.