A woman wearing a face mask walks past a closed shop in Rome, Italy, on May 18, 2020. The sign on the store window reads "Without government aid, we cannot reopen on May 18. Thousands of employees at risk."

COVID-19’s uneven economic impact on the European Union portends an equally uneven recovery, as growth in the south will be weaker than in the rest of the Continent due to structural factors. Different policy priorities between harder-hit southern states and their northern and eastern peers will thwart the bloc’s ability to increase financial integration among its 27 members, as well as implement monetary policies for its 19-member currency zone. The risk of social unrest, government collapses and the emergence of anti-establishment movements will also be higher in Southern Europe, where the pandemic has exacerbated countries’ pre-existing economic weaknesses such as high unemployment, deep fiscal deficits and high sovereign debt levels.

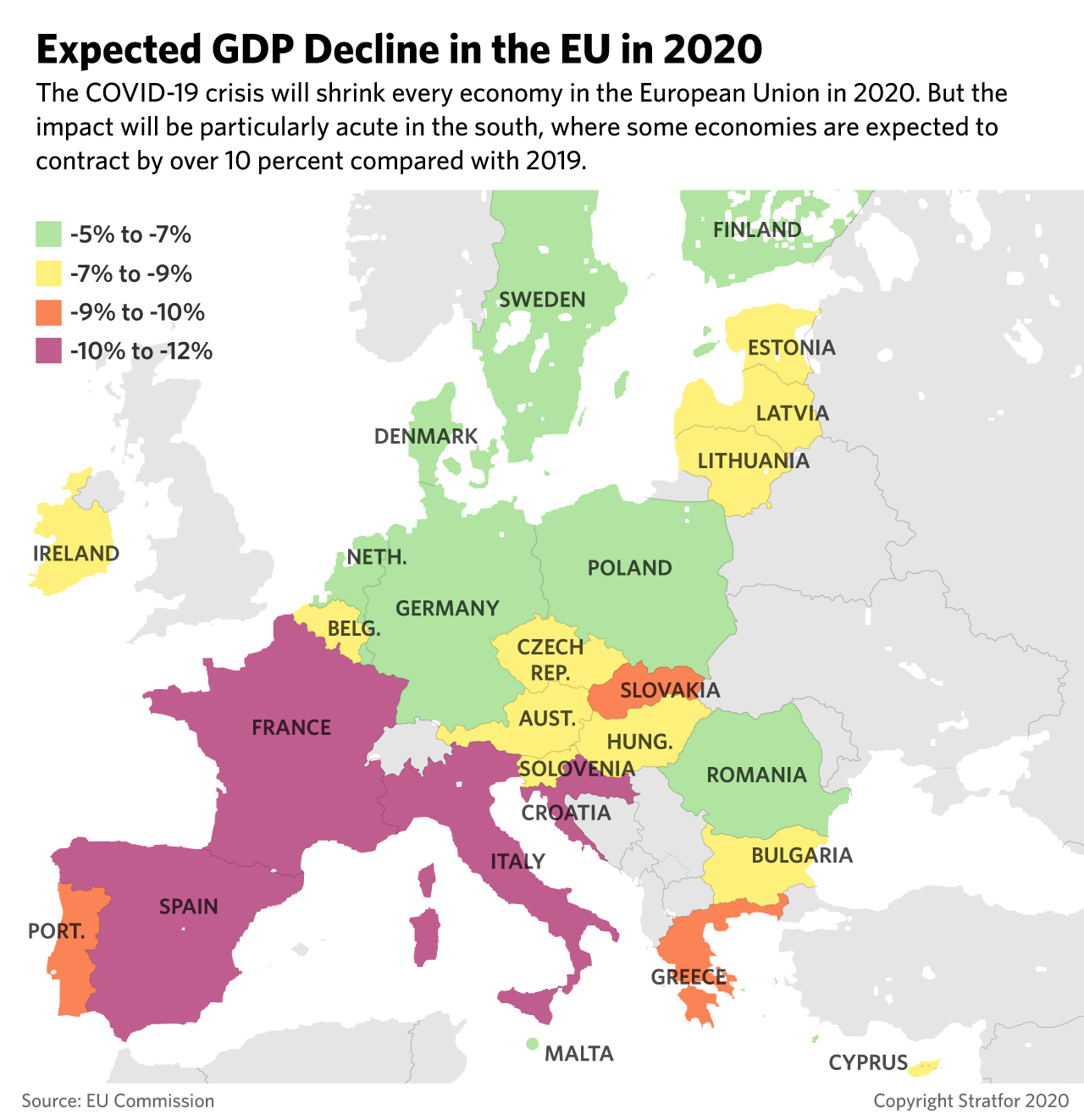

- According to the European Commission, the GDPs of Italy, Spain, France and Croatia will contract by more than 10 percent in 2020, followed by growth by between 6 and 8 percent in 2021. On the contrary, countries like Poland, Sweden, Romania, Denmark and Germany will only contract by 5-6 percent in 2020, followed by recoveries between 4-5 percent in 2021.

- In February of 2020, the last month before the start of the COVID-19 in Europe, the unemployment rate was already above the EU average (6.5 percent) in countries including Greece, Spain, Italy and France, and below the average in countries including Germany, the Netherlands, the Czech Republic, Poland and Romania.

- In the first quarter of 2020, the debt-to-GDP ratio was already above the EU average (79.5 percent) in southern countries including Greece, Italy, Spain, France, Cyprus and Portugal, and below the average in northern, central and eastern countries such as Germany, the Netherlands, Poland, Romania and Czechia. This increases the risk of a sovereign debt crisis in the south.

The economic crisis is deeper in Southern Europe because countries are more dependent on activities such as tourism, which have been particularly affected by COVID-19 lockdown measures. Northern and Eastern European countries, on the other hand, are more dependent on manufacturing and industrial exports, where the impact has been more modest.

- Tourism represents around 20 percent of GDP in Croatia, 18 percent in Greece, 13 percent in Italy, and 12 percent in Spain. On the contrary, it represents less than 6 percent of GDP in northern countries such as Germany and the Netherlands, and central and eastern countries such as Poland and Romania.

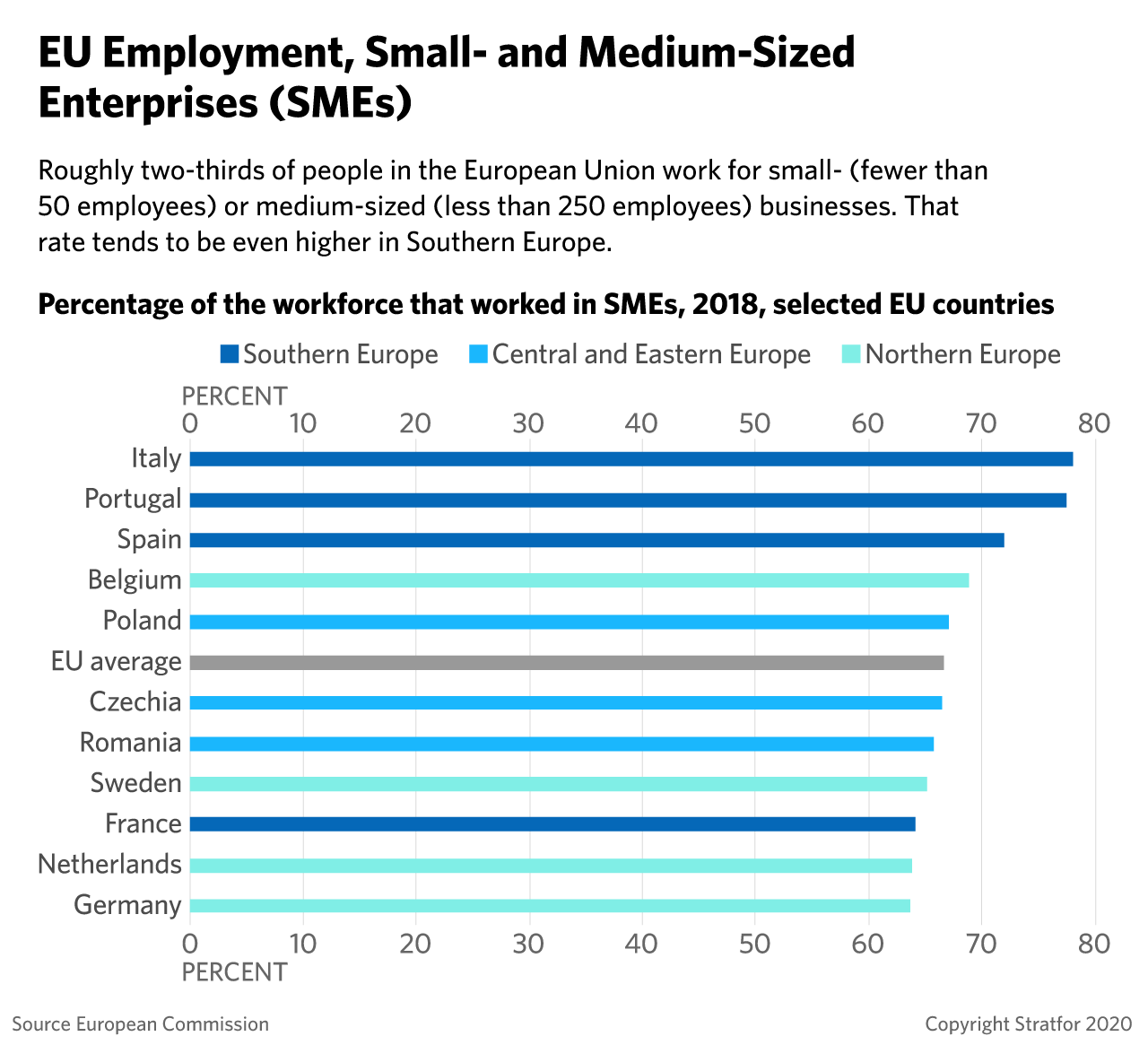

Southern European economies are also more dependent on small- and medium-sized enterprises (SMEs), which are less resilient to crises, for added value and employment. SMEs’ smaller structures and limited access to credit leave them more exposed to pandemic-related economic crises compared with their larger counterparts. SMEs in Southern Europe also tend to have a larger concentration of sectors that were hit hard by the lockdown measures (such as tourism, travel and hospitality) than their peers in other parts of the EU.

- SMEs generate around 68 percent of added value in Portugal, 67 percent in Italy, and 61 percent in Spain, as opposed to 54 percent in Germany or 52 percent in Hungary.

- SMEs generate around 78 percent of employment in Italy, 77 percent in Portugal, and 72 percent in Spain, as opposed to 67 percent in Poland and 64 percent in the Netherlands and Germany.

This economic divergence between Northern and Southern Europe will complicate the European Central Bank (ECB)’s ability to create and implement “one-size-fits-all” monetary policies for the 19 countries that use the euro, resulting in additional market uncertainty. Since the beginning of the pandemic, the ECB has expanded its bond-buying program to inject liquidity in the eurozone and to keep member states’ borrowing costs low. But inflation levels are very low (and in some countries deflations are already happening), which could further weaken domestic consumption and delay the eurozone’s economic recovery. The euro has also strengthened vis-a-vis the U.S. dollar in recent weeks, which undermines European exports. Against this backdrop, ECB policymakers are internally divided over whether the bank needs to expand its stimulus measures or wait for the individual fiscal measures taken by national governments to bear fruit.

- On Oct. 6, ECB President Christine Lagarde said the bank is considering other options to boost economic growth in the eurozone, but did not rule out a further cut in the already negative interest rate.

- Central banks in northern Europe, and the German Bundesbank in particular, are against interest rate cuts because of their negative impact on private banks’ profitability and their customers’ savings.

- The Bundesbank is also skeptical of further extensions of the ECB’s bond-buying program, and has warned that monetary policy cannot be a substitute for economic reforms in eurozone countries.

- ECB Vice President Luis De Guindos and Executive Board member Yves Mersch recently said there is no need for additional measures. But another ECB board member, Fabio Panetta, also said the bank should introduce preemptive stimulus.

EU grants and loans will help reduce the economic gap between southern countries and their eastern and northern peers, but probably not to the extent that the entire bloc comes out of the crisis at the same time. Southern Europe will be the main recipient of EU relief funds in 2021, but the bloc’s own forecasts predict that it will not be enough to prevent a two-speed economic recovery in the bloc. The ongoing disputes over the approval of the EU budget for 2021-2027 and the COVID-19 relief fund could delay the disbursement of the money and further consolidate this uneven economic rebound. Moreover, high unemployment in the south means that these governments will spend a significant part of EU funds on job retention schemes instead of other measures to stimulate the economy or promote innovation. Future decisions to increase financial risk-sharing in the European Union (such as the completion of the banking union in the eurozone) could also be delayed because of the deeper economic gap within the bloc, as the north will be reluctant to further share financial risk with the south.

- Italy and Spain will be the main receivers of loans and grants from the European Union’s 750 billion euro ($886 billion) COVID-19 recovery fund, with 209 billion euros ($245 billion) allocated for the former and 140 billion ($164 billion) allocated for the latter.

- The German government has admitted that because of disputes over mechanisms to link the disbursement of EU funds to keeping a strong rule of law, the recovery fund may not be implemented in January as originally scheduled.

Southern Europe’s more fragile economic situation means it will also face higher risks of social unrest and political volatility than other parts of the Continent. The added pressure of the current economic crisis could be the final straw that collapses the already weak coalition governments in countries such as Italy and Spain. In the meantime, rising unemployment and the expiration of furlough schemes (which will be phased out throughout 2021) will also increase the possibility of social unrest in Mediterranean countries. Anti-establishment and extremist political parties — such as Italy’s Lega, Spain’s Vox and France’s National Front — have so far failed to exploit the pandemic to their political benefit, but worsening economic conditions could boost their popularity by creating a fertile ground for their rhetoric. The risk of another rise of anti-establishment parties will also exist in the rest of the Continent, but they will be lower in those areas where the unemployment situation is not as severe.

- Germany, the Netherlands, Czechia and Bulgaria are the only EU member states with general elections scheduled for 2021, which should somewhat reduce political uncertainty in Europe.

- However, early elections could happen anywhere in the bloc if governments collapse because of internal disputes or social unrest caused by their weak economic situations.

- Countries like Spain and Germany have already experienced small scale anti-lockdown protests. More protests could follow in the likely case that further restrictions on social mobility are introduced, given that many countries in Europe are now seeing another rise in COVID-19 cases.