The U.S. Federal Reserve building is seen on July 1, 2020, in Washington D.C.

By saying it will tolerate higher inflation for longer and not move preemptively against potential reignited inflation, the U.S. Federal Reserve is conducting a monetary policy experiment with long-term risks to interest rates, exchange rates, wages, investment, financial stability and, ultimately, economic growth. There is no alternative to the current easy monetary policy, given the continued disruptions in the U.S. economy. And, while rekindled inflation is not an immediate threat, political pressures to maintain exceptional monetary support and a broadening central bank mandate, along with large fiscal stimulus, could create a situation that leaves the Fed with too few options, too late.

According to a comprehensive study the World Bank released in 2019, “high inflation is often associated with lower growth and financial crises.” Inflation infamously distorts the economy by causing the misallocation of resources, eroding savings and asset values, and leading to unproductive activities that undermine long-term growth. Significantly, inflation is correlated internationally and fighting it requires central banks to raise interest rates and tighten financial conditions. That, in turn, has immediate effects on highly indebted households and businesses, both in the United States and abroad, as well as governments with high debt levels in foreign currency, including emerging markets.

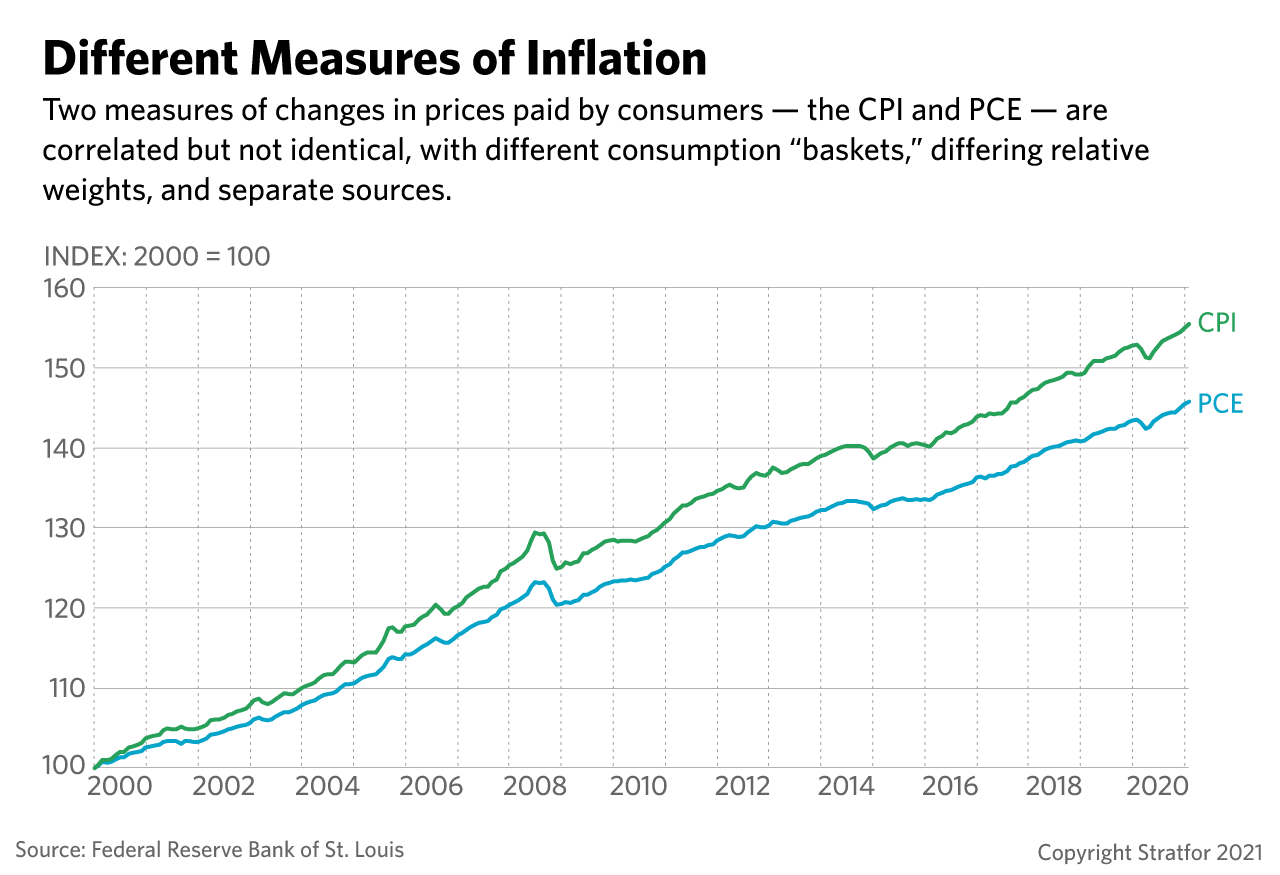

Headline inflation will increase in the United States over the next 2-3 months, if for no other reason than the price level decline in March-May 2020 at the height of COVID-19 lockdowns giving rise to “base effects” as prices recover. The U.S. Consumer Price Index (CPI) increased in February (the latest reading) by 0.4% (seasonally adjusted, m-o-m), accelerating slightly from a 0.3% increase in January and was up by 1.7% (y-o-y). The Fed’s preferred inflation measure, the Personal Consumption Expenditure Index (PCE) — which is a broader measure and more consistent with GDP — was also up by 0.23% in February, slowing from 0.33% in January and rising 1.6% from a year earlier after a less than 1.3% increase in 2020.

The Fed believes the expected increase in inflation will be transitory and not durable. Its median projections are for an increase in the PCE of 2.4% in 2021, returning to it’s 2% average inflation target in 2022. Those projections do not, however, address other current inflation trends, which include global food prices being at a seven-year high, according to the U.N. Food and Agriculture Organization. The past year has also seen a tripling in global shipping costs, as well as price increases for nearly all industrial commodities (including an 88% increase in copper prices alone) and supply chain bottlenecks (as evidenced by the global shortage of semiconductors, which has affected everything from automobile production to consumer electronics).

Indeed, the Fed is betting it can ignore coming changes in actual inflation, opting to determine its policy path based on economic outcomes instead of acting preemptively based on projections. The Fed’s recent adoption of average inflation targeting also means it will tolerate inflation greater than 2% for an indefinite time, as long as inflation expectations don’t increase.

- The immediate focus is on stimulating employment among low income and minority workers. This is based on the assumption that the economy can run “hot” as long as there is excess slack, with employment levels still 8.5 million below pre-pandemic levels and capacity utilization in February at less than 74%.

- The Fed sees recent labor market headlines with payroll gains of 1.3 million in February-March and an unemployment rate of 6% as not fully reflecting underlying trends and hidden unemployment. At 57.8%, the U.S. employment-population ratio is 3.3 percentage points lower than in February 2020.

The Fed believes a 30-year history of average 1.6% inflation gives it credibility, as realized inflation during much of that period did not exceed expected inflation. Inflation, however, is a forward-looking iterative process based on multiple factors, which central banks may not fully or properly understand. Over the past several years, U.S. inflation has undershot targets, with the Fed unable to boost it to 2%. But the Fed and central banks elsewhere in the world cannot explain what they call “missing inflation.” They may not give enough credit to non-monetary factors suppressing inflation, including the increased global labor supply from China since 2001, low real wages and structural changes in the world economy that reduced production costs. Those factors are now reversing as demographics and increased incomes dampen China’s comparative advantage. Global supply chains, meanwhile, are either “reshoring,” shortening or diversifying, which will cause higher input costs for labor and materials and create a need for permanently higher inventories compared with the “just-in-time” model of the past 20-30 years.

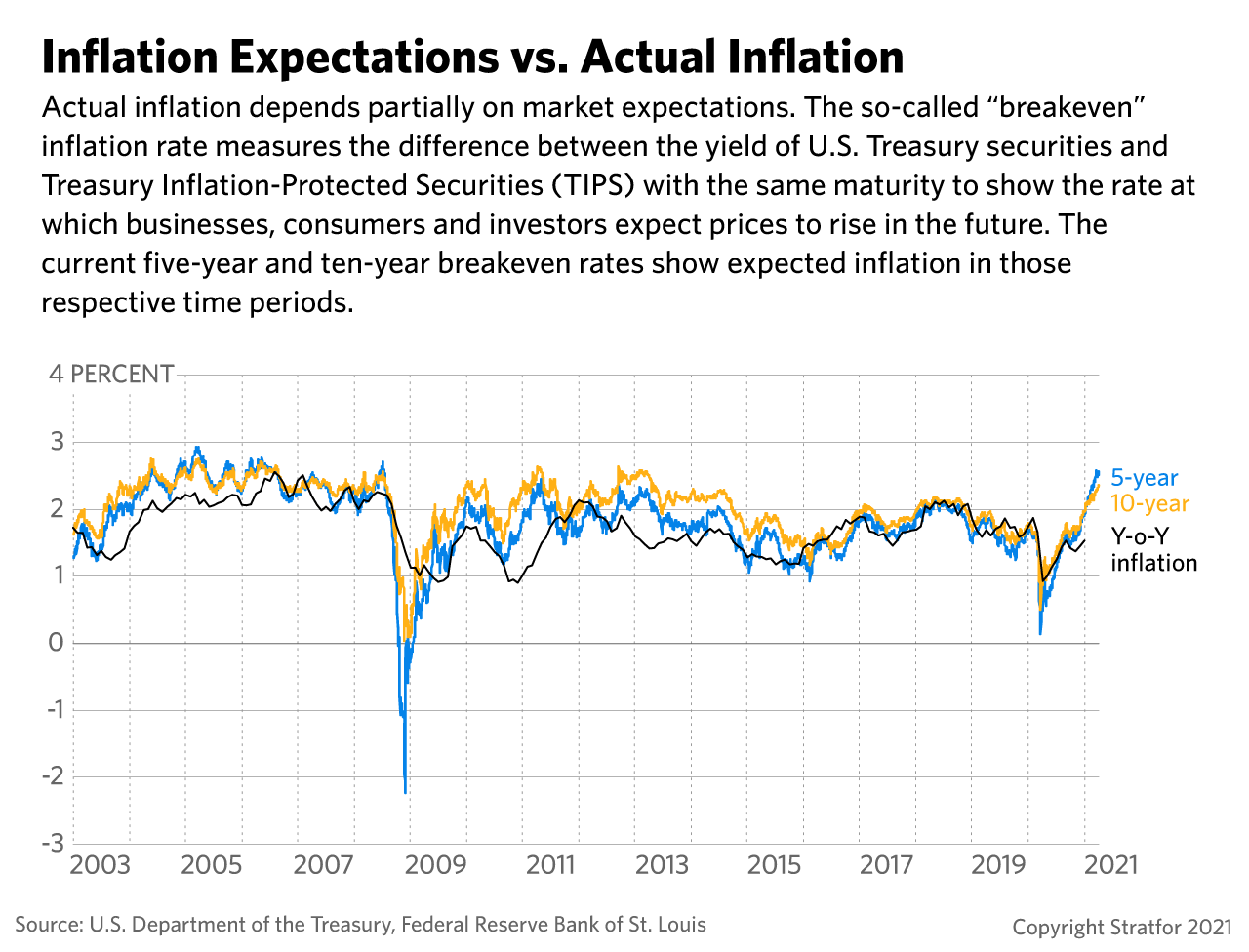

In addition, market measures of expected inflation are increasing, even as the Fed says they are anchored:

- Long-term bond yields, while still low by historical standards, are rising. The rate on five-year U.S. Treasury notes is near 1%. The 10-year yield is also hovering around 1.7% after having been less than 1% at the beginning of 2021, while the 30-year bond yield recently increased from 1.66% to 2.3%.

- So-called “break-even” rates on Treasury securities, which subtract returns on inflation-protected bonds from nominal yields, shows market expectations of five-year inflation equal to more than 2.5%.

- Consumer sentiment surveys conducted by the New York Federal Reserve Bank and the University of Michigan show expectations of five-year inflation above 3%, well past the Fed’s horizon.

Fed Chairman Jerome Powell has acknowledged the uncertainty, saying that the United States has never experienced such a sudden economic downturn and recovery on the scale of the past year, nor has the country ever, outside of wartime, had fiscal (and monetary) stimulus on the scale now anticipated. Powell didn’t, however, say that underlying economic relationships in the U.S. economy, such as consumption functions and labor demand, may have shifted during the COVID-19 pandemic, leading to structural breaks in time series that make past data poor indicators of the present and future path. Accordingly, the Fed’s willingness to let the economy “run hot” in the face of massive fiscal stimulus and rebounding aggregate demand could, within a short time, increase expected inflation.

Other factors could constrain the Fed's ability to take action and further complicate its response, should it need to react quickly to inflationary pressures. The Fed is now the lender of last resort not just to the banking system, but to large parts of the private sector through emergency lending programs. It also makes credit allocation decisions normally made by financial intermediaries. This undermines market determinations of value and preserves what might be otherwise insolvent firms that will resist liquidation.

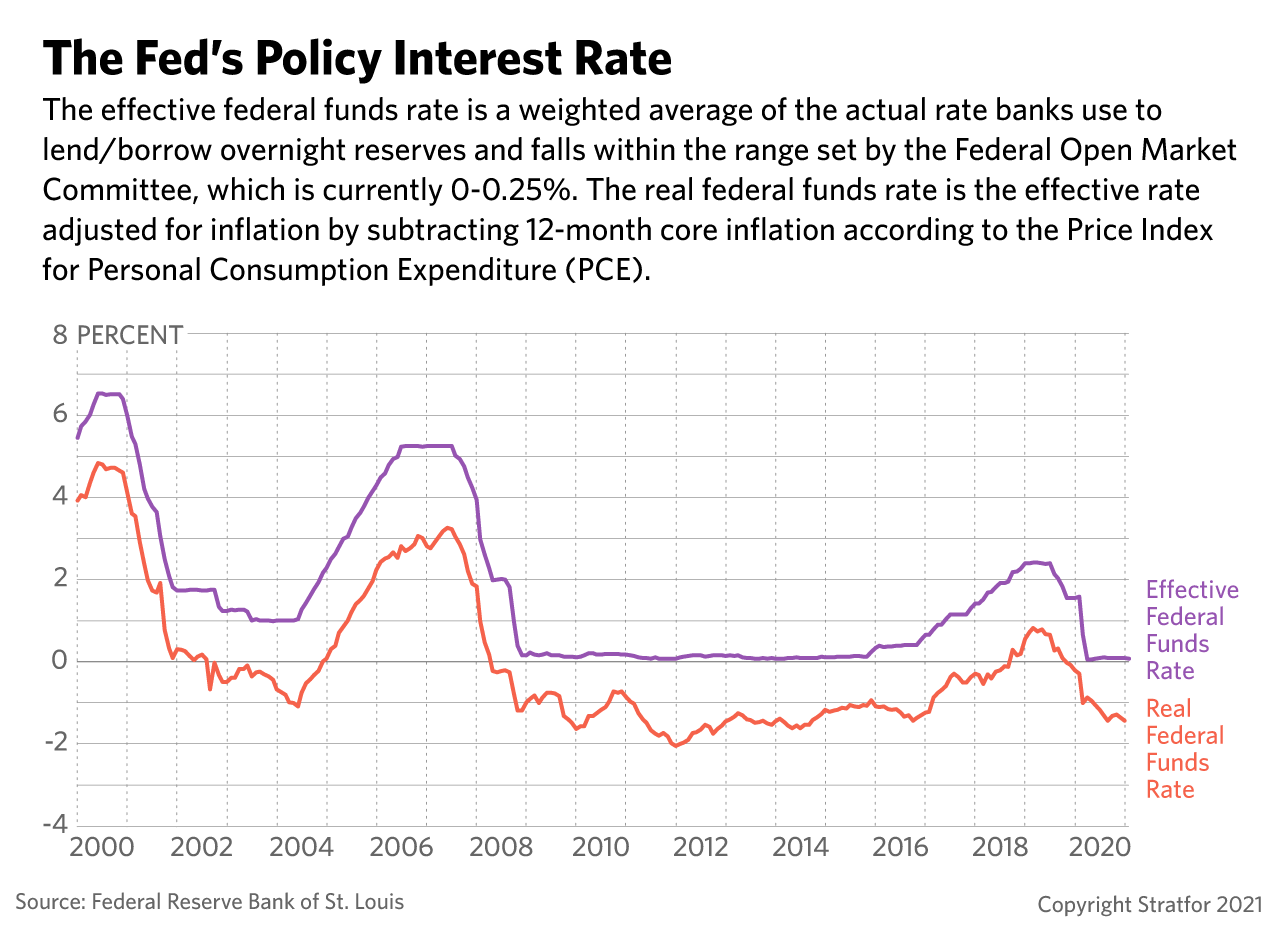

- Equity and housing markets are underpinned by low interest rates, with the Fed buying $40 billion worth of mortgage-backed securities a month while providing market liquidity with $80 billion a month for Treasury purchases. Tapering asset purchases or unwinding the current $7.7 trillion balance sheet — which is still growing at more than $1.4 trillion yearly — will affect financial markets adversely by reducing valuations, as new assets sold by the Fed and new liabilities issued by the Treasury cause the market supply of bonds to increase.

- U.S. fiscal policy is propped up by low interest rates on an unprecedented and growing level of debt. The Congressional Budget Office projects a near doubling of the U.S. public debt-to-GDP ratio to 195% by 2050. Government deficits will continue to drive debt accumulation. High rates of money growth and the larger debt supply, meanwhile, will increase the cost of capital, deter long-term investment in plant and equipment needed to increase productivity, and tamp down long-term growth prospects.

- The Fed is also using its monetary tools to address, among other things, labor market disparities, income inequality and climate change. None of those problems were caused by monetary policy and addressing them could give the Fed a political agenda that prevents effective action to stem inflation.

The implication of dependency on outcomes risks putting the Fed behind the curve in taking action. Adding to the uncertainty is the fact that monetary policy also does not change inflation dynamics quickly, but rather with long variable lags of 18-24 months. Ex-post data, which by definition is backward-looking, could force the Fed to over-respond and suddenly put on brakes by raising interest rates precipitously, which could put the economy back in recession with unemployment still high. Alternatively, the U.S. central bank might act slowly, inviting an inflationary spiral and eventual stagflation — that is, low growth with a rapidly rising price level.

- The Congressional Budget Office’s most recent projections, released in mid-February, estimate the U.S. economy’s “output gap” was 3% of GDP in 2020, and did not foresee a positive inflationary output gap until 2025. However, that forecast included neither the $1.9 trillion American Rescue Plan Act nor infrastructure spending of $2.25 trillion, which combined equal to another 20% of 2020 GDP.

- There is also $1.7 trillion in forced “excess” savings from foregone U.S. spending, equal to more than 8% of 2020 GDP.

- The combination of a sooner-than-expected positive/inflationary output gap, plus rapidly increasing and largely monetized federal debt, could explode inflation, especially if supply constraints persist.