An electronic board shows the index chart at the Sao Paulo Stock Exchange after shares in Brazilian state oil giant Petrobras plunged amid news of a leadership shake-up on Feb. 22, 2021.

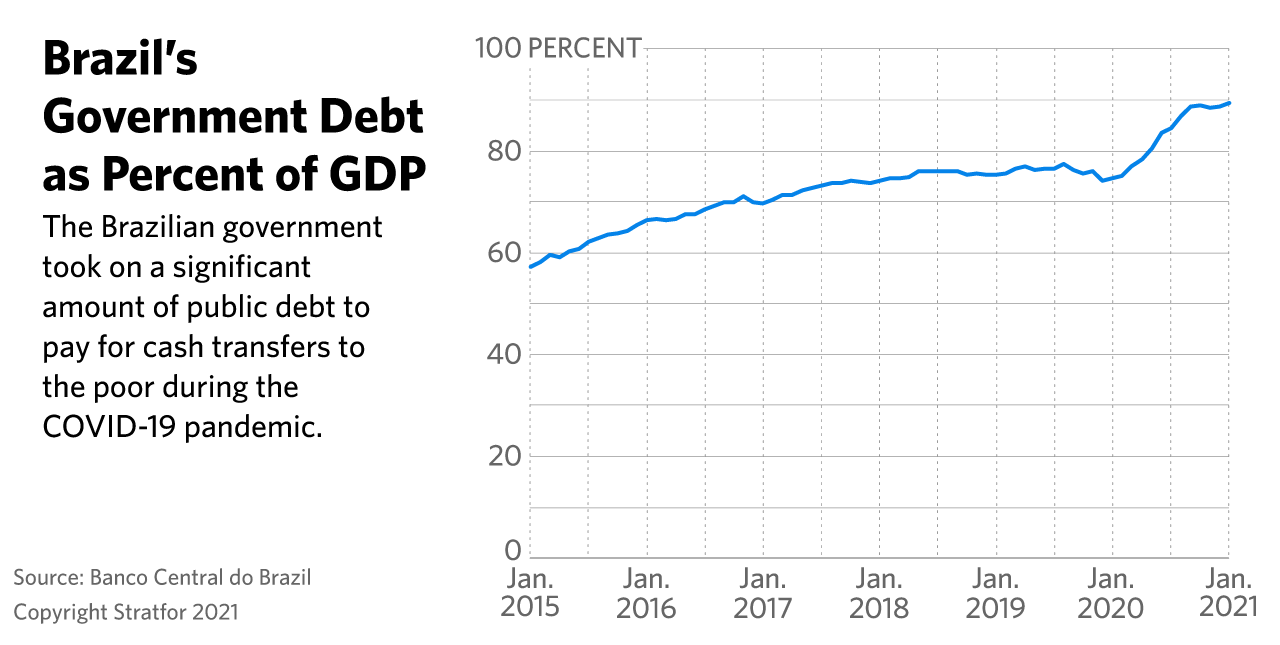

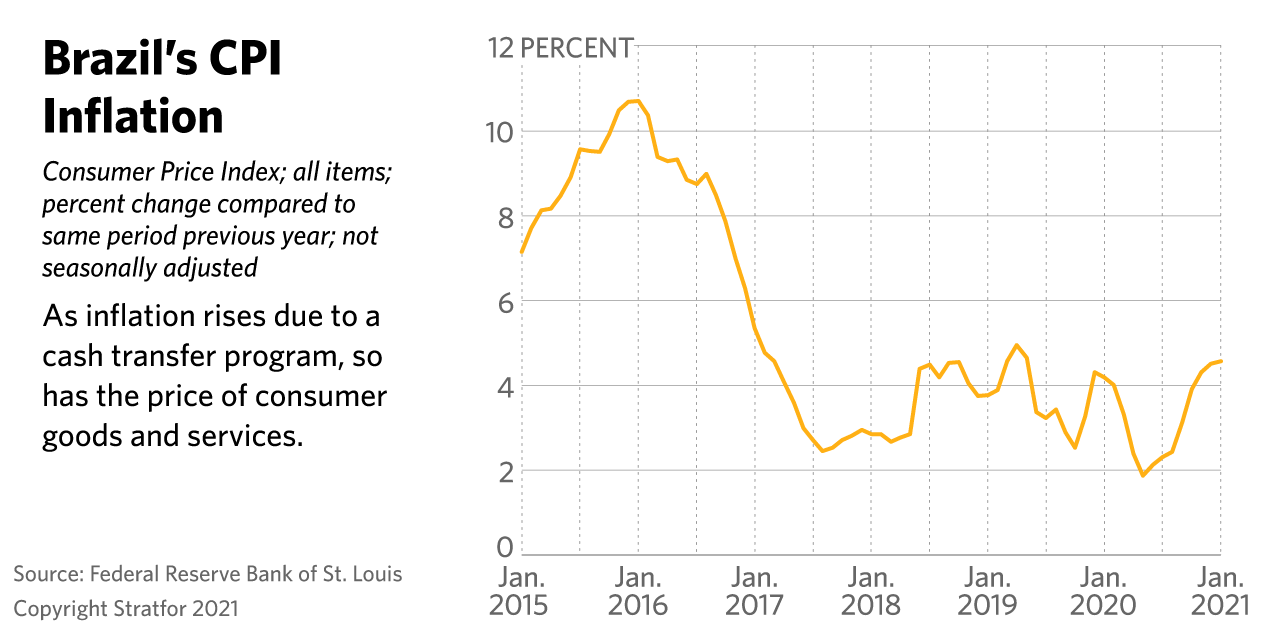

The Brazilian government is unlikely to implement fiscal reforms needed to emerge from its pandemic-induced recession ahead of the 2022 presidential election. This will, in turn, damage investor confidence and foreign investment inflows, which could delay Brazil’s economic recovery, worsen its fiscal problems and reduce trade with other nearby economies. Brazil’s politicians have used costly welfare programs to keep the economy and their approval ratings afloat during the pandemic, and are now adverse to putting a cap on public sector spending. Brazil’s fiscal sustainability is at risk due to rising inflation, high public debt and a recession triggered by the COVID-19 pandemic.

- Before COVID-19, Brazil’s GDP was growing at 1.4% in 2019. But in 2020, the country’s GDP contracted by 4.7%, putting Brazil into a recession.

- Annual consumer inflation in Brazil hit a four-year high of 5.2% in February, up from 4.6% in January and a steep rise from 1.9% in May 2020. According to estimates from Brazil’s central bank, inflation will likely rise to 7% by mid-2021. To combat inflation, Brazil’s central bank raised interest rates on March 17 by 75 basis points to 2.75% and has indicated that it will seek to further raise interest rates in May 2021.

- In April 2020, the government implemented a costly welfare program, paid for by the accumulation of public debt. This welfare program allowed President Jair Bolsonaro to maintain high approval ratings (40%) until the program was terminated in December.

Brazil will probably not implement structural economic reforms due to domestic political pressures brought on by the 2022 presidential election. Though over a year away, Brazilian politicians are already preparing for the country’s 2022 presidential election. Former President Luiz Inacio Lula da Silva recently had corruption charges dropped, allowing him to run as a presidential challenger. Bolsonaro’s declining approval ratings will probably push him to increase fiscal spending on popular welfare programs such as cash transfers to the poor and subsidizing the price of petroleum. Additionally, should da Silva win in 2022, he would almost certainly increase spending to implement the populist policies that he has championed.

- On Feb. 19, Bolsonaro announced his intent to replace the CEO of state-run oil company Petrobras with the country’s former defense minister, Joaquim Silva e Luna, following a weeks-long oil price dispute with the current CEO, Roberto Castello Branco. The swap will likely enable Bolsonaro to fix the domestic price of oil in the hopes of appeasing the trucker unions that have recently staged protests against rising diesel prices.

- The government is currently pushing to send emergency stipends totaling almost $7.96 billion, which will see payouts until June 2021. This latest round of fiscal spending is not subject to the government’s spending cap, meaning that Congress may supersede budget limits.

Failure to introduce fiscal reforms could result in Brazil missing the opportunity to attract new waves of foreign direct investment (FDI) when the pandemic starts to subside, depriving the economy of one of its main growth drivers. 3.8% of Brazil’s GDP in 2019 came from FDI inflows, as compared with the 1.8% global average. As global economic activity recovers in the second half of 2021, investors that postponed their decisions because of the global recession are likely to drive a wave of new investment, which Brazil may miss out on due to its domestic political and economic situation. The country’s ballooning public sector debt, high fiscal deficit and political uncertainty could undermine investor confidence.

- FDI flows into Brazil were roughly halved in the first half of 2020 to $18 billion, seeing a moderate recovery in the second half of the year due to asset sales and the rollout of an infrastructure program.

- The Brazilian government has not taken any substantial measures to reduce public debt. In 2020, Congress was able to circumvent a constitutional spending cap, which limits public spending growth to the previous year’s rate of inflation, by using a special allowance for “emergency circumstances.” As 2021 shapes up to be another challenging year for Brazil, politicians are likely to attempt to increase public spending again.

- Brazil’s fiscal policies have resulted in credit rating agencies labeling the country’s debt as junk bonds. S&P Global Ratings and Fitch Ratings have downgraded the country’s sovereign credit rating to a BB-, citing high government debt levels as the main factor in both of their decisions.

- Recent political interference in Brazil’s energy sector also risks deterring investment in projects that make up the bulk of the country’s FDI levels.

- Hikes in interest rates will also make it increasingly costly to take out loans in Brazil, straining the country’s businesses.

A prolonged recession in South America’s largest economy could thwart recoveries in other nearby economies like Argentina and Chile, which both rely on exporting goods to Brazil. An extended recession in Brazil would likely have a lasting impact on neighboring Argentina and Chile, which export 16% and 4.7% of their goods, respectively, to Brazil. It would also affect Peru, Colombia, Bolivia and Paraguay, all of which export significant quantities to Brazil as well. This would complicate South America’s efforts to end the recessions caused by lockdown measures in 2020 and early 2021.