A view of the International Monetary Fund (IMF) building from the street in Washington D.C. on Sept. 25, 2020.

Zambia is expected to default on its external debt when the southern African country misses $118 million in interest payments on eurobonds due from Oct. 14 to March 2021. Hopes for a comprehensive debt restructuring are overly optimistic without major help from China, its largest creditor, as well as a substantial macroeconomic adjustment program supported by the International Monetary Fund (IMF). Zambia is the first comprehensive case involving all creditor classes this year, and neither the Paris Club nor bondholders will restructure debt without appropriate burden-sharing by China.

On Sept. 30, holders of $3 billion in eurobonds rejected Zambia’s request for a freeze on payments. That was just one day after the country became the first to ask for treatment from private creditors comparable to what the Paris Club already has done by deferring debt payments due over the last eight months of 2020. Press reports indicate an official request was made for some form of debt relief, if not debt cancellation, from China in July, but bondholders were not given details on negotiations or Zambia’s plans.

- The Paris Club and international financial institutions wrote off Zambian claims in 2005 under the Heavily Indebted Poor Country (HIPC) initiative and the Multilateral Debt Relief Initiative.

- The IMF estimated in 2019 that Zambia owed the Paris Club only about $100 million, although the African Forum and Network on Debt and Development (AFRODAD) reports relief from Group of 20 (G-20) countries would be on the order of about $150 million in 2020.

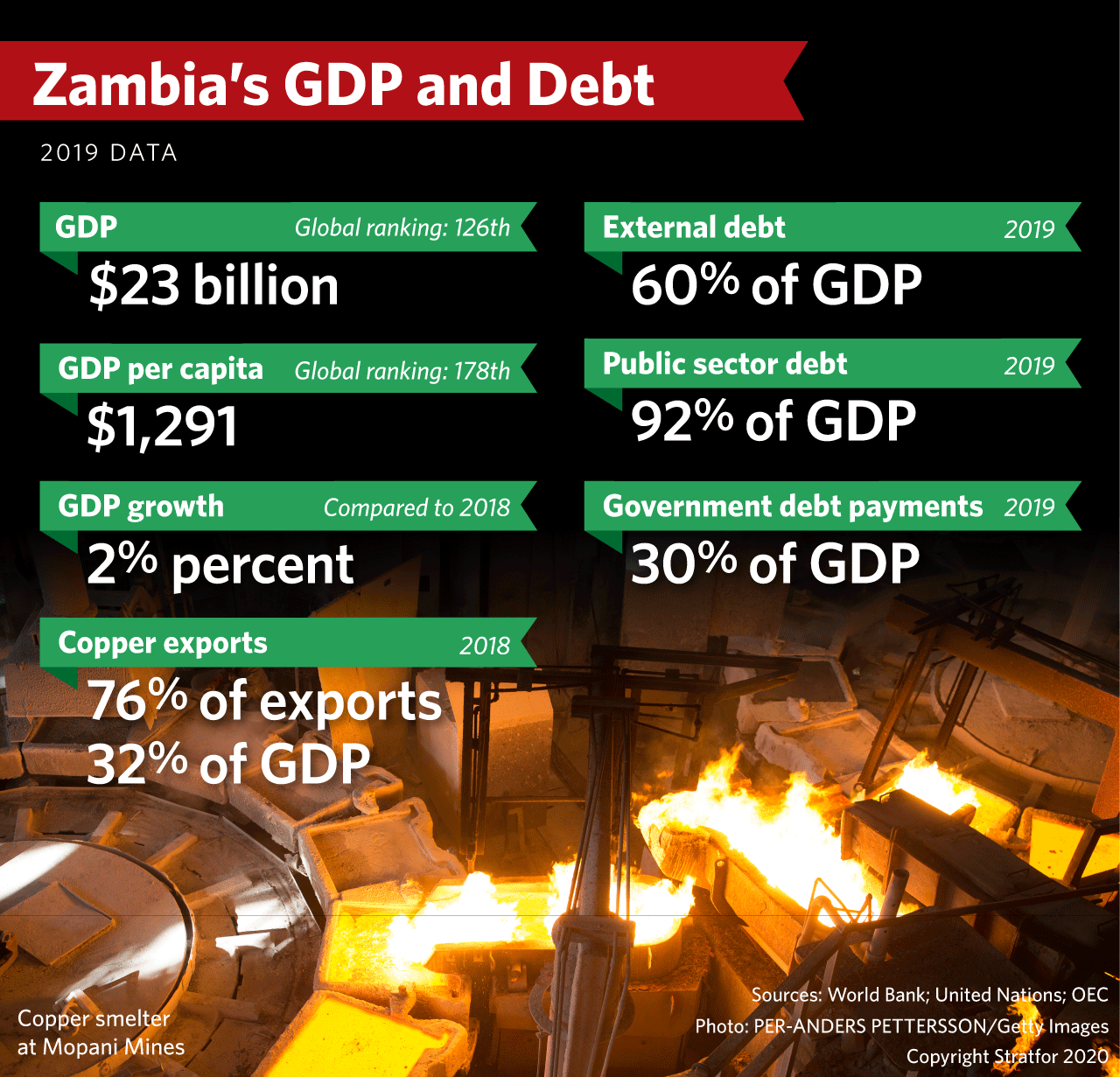

Chinese claims on Zambia are not known, but the IMF reported in mid-2019 that the country’s non-Paris Club bilateral debt was 26.5 percent of its total external debt of $13.2 billion. Other estimates are that China is owed about one-third of the outstanding debt. Chinese state-owned policy banks and commercial banks lend, most often, for construction projects, which finance Zambia’s development strategy of rapid public investment in domestic infrastructure. Government investment was projected at 8.4 percent GDP, nearly all of it foreign-financed, when initial 2020 projections were made, which also included a forecast of 1.7 percent GDP growth. It’s not clear that investment spending was scaled back in 2020, even as GDP falls by an estimated 3-4 percent, while the fiscal deficit hits 11.7 percent of GDP (up from 8.2 percent in 2019).

While the Paris Club is providing temporary debt relief through a delay in interest and principal payments, Zambia also requires debt reorganization by all external creditors, including China and private creditors. Zambia’s debt is unsustainable due to its falling export revenues, large fiscal deficits and depreciating exchange rate, which led the IMF to deny the country money from its emergency Rapid Financing Instrument and Rapid Credit Facility in May. Zambia remains in discussion with the IMF, but the latter made clear that “any IMF financial support, including emergency financing, is contingent on steps to restore debt sustainability.” That includes a major realignment of economic policies, including reining in public spending.

- Zambia’s external debt service requirements are high, with a scheduled debt service of $1.6 billion in 2020 and again in 2021, before rising to $2.34 billion (or 10 percent of the country’s pre-pandemic GDP) in 2022.

- Zambia’s external debt increased by more than 10 percentage points of GDP in 2019, from 48.1 percent to 59.9 percent. While exchange rate depreciation played a role, the debt spike was largely driven by new money disbursements of more than $2.7 billion. Zambia’s total public sector debt-to-GDP ratio increased even more, from 78.1 percent of GDP in 2018 to 91.6 percent by the end of 2019.

- In mid-2019, well prior to the current recession, the IMF recommended that Zambia make a fiscal adjustment equivalent to 7.3 percent of GDP in 2019-2020, including a more than 5 percent of GDP cut adjustment in capital spending.

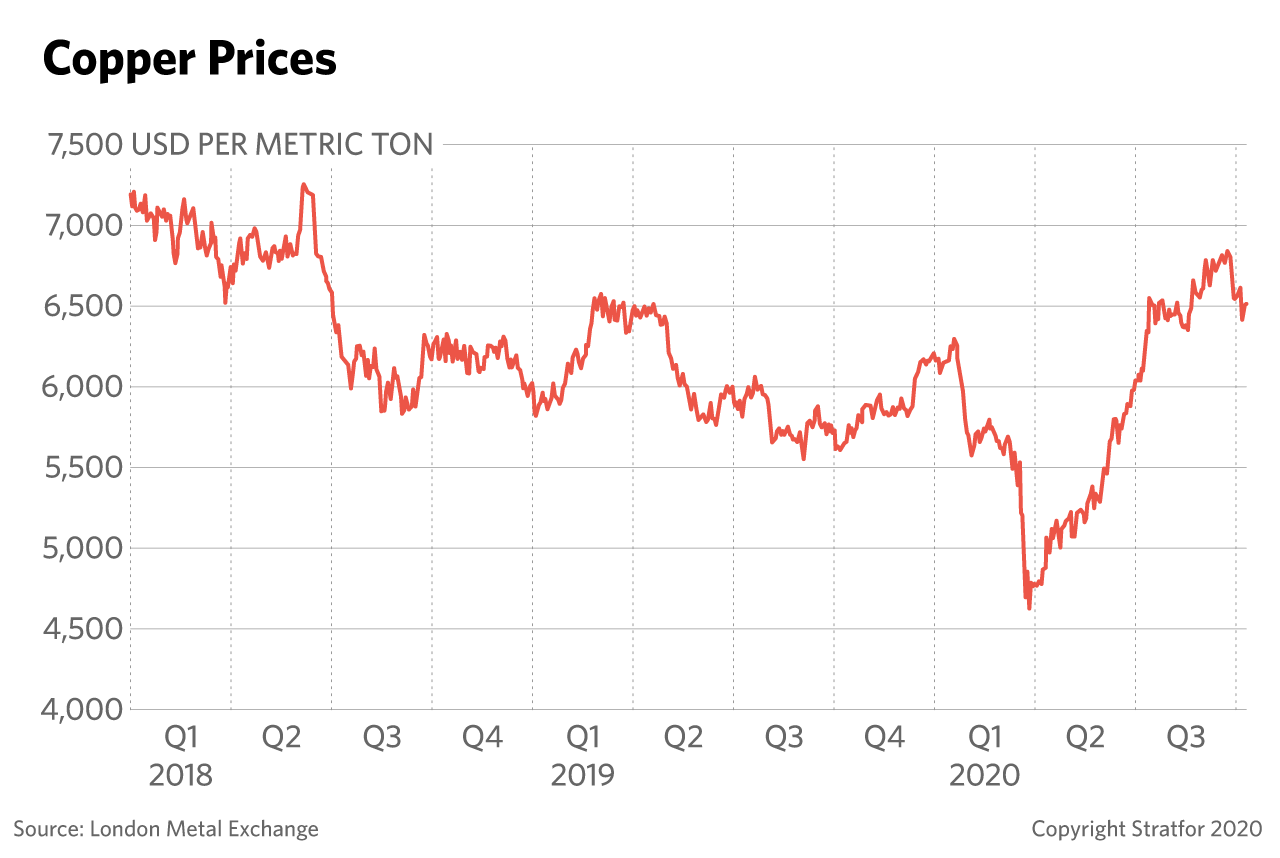

Zambia’s business environment is also deteriorating. Press reports indicate the government is trying to influence asset prices of international companies with controversial operations in the country, as COVID-19 causes disruptions in the trade and prices of commodities. With government revenue also reportedly down by one-third in the second quarter of 2020, Lusaka is looking to increase its revenue share generated by Zambia’s mining sector, which accounts for 70 percent of the country’s exports. But Zambia’s cumbersome tax policies have only further impeded the country’s copper production by increasing costs in its already high-cost mining industry.

- Despite recent increases, global copper prices are still down nearly 10 percent overall since mid-2018.

- Glencore PLC recently offered to sell its stake in a major mine after a number of policy dustups with the government. Canadian-based First Quantum Mining has also delayed expanding its operations in Zambia due to disputes over royalties.

As it tries to extract more revenue from its copper industry, the Zambian government may be looking to make concessions with China in exchange for favorable treatment of its debt. Those could include allowing a Chinese takeover of some copper mines or other state-owned assets, or pledging of revenues that would otherwise be available to pay all creditors and would effectively give China preferred creditor status. China may be seeking similar concessions in Angola where it’s also the largest creditor, and press reports say it’s seeking ownership shares in some oil fields.

Other issues that will affect creditor attitudes and restrict Zambia’s ability to get an IMF program include:

- A prolonged drought affecting non-mining activities, with agricultural and electricity generation down sharply. Agriculture accounts for less than 10 percent of Zambia’s GDP, but 50 percent of employment. Structural efforts to diversify away from mining are essential.

- Presidential and legislative elections scheduled for August 2021, with government patronage efforts crippled by lower fiscal revenue. Zambia’s political will to implement economic adjustment is questionable in the best of times, but especially so prior to elections.

- Zambia’s historically poor track record of implementing economic policies. The IMF reported in mid-2019 that its previous “recommendations to rein in fiscal deficit and reduce debt vulnerabilities were not implemented” by the Zambia government.