Prospects for a quick global economic recovery from the COVID-19 pandemic are officially dead, with all major international financial institutions and private forecasters now projecting huge cumulative losses and an uneven, prolonged climb out of the world’s steepest recession in 80 years. Economic models have proven incapable of dealing with uncertainties and discontinuities of the current unprecedented global lockdown. But even though magnitudes vary, recent forecasts are headed in the same direction — down.

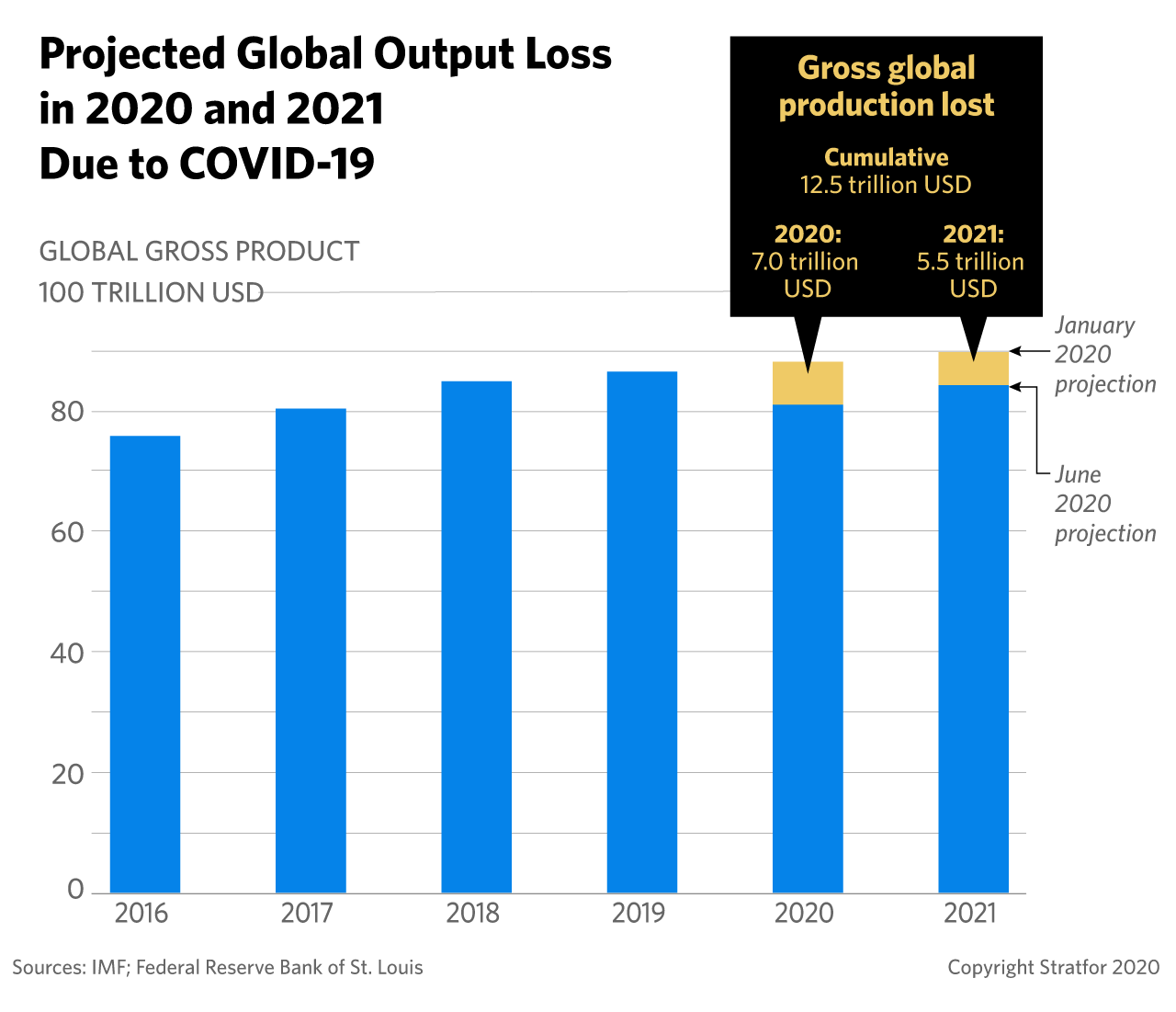

- The International Monetary Fund (IMF) now expects a cumulative $12.5 trillion economic loss from COVID-19 in 2020-2021, with a 4.9 percent fall in global production this year and a 5.4 percent recovery in 2021. The IMF also presumes that the strength of the recovery remains “highly uncertain,” and that a potential second wave of global infections in 2021 would result in an additional 2.5% decline in economic growth that year.

- The IMF, however, is actually one of the more optimistic prognosticators: The World Bank has predicted a 5.2 percent global economic contraction in 2020, with the Organization for Economic Cooperation and Development foreseeing an even larger 6 percent decline. Private sector forecasts, meanwhile, foresee global declines of as much as 12 percent this year in their worst-case scenarios.

There are considerable downside risks that include the synchronized nature of the slowdown in 95 percent of the world economy, especially without a major country or group of countries acting as a “locomotive engine” to pull along the rest. China is the only major economy that still has a chance of slightly positive growth this year of about 1 percent. Though even that small uptick presumes the recent outbreak of COVID-19 in Beijing does not become widespread.

Even if the pandemic is brought under control in the coming months, the global recovery will still be slow and uneven since countries are emerging from lockdown at varying speeds. Caution by consumers and businesses will mean hangovers for labor markets, particularly given the unprecedented speed of economic decline and resulting job losses. In the “dismal science” that is economics, real wages would normally be expected to rise during a pandemic as a result of deaths and changing capital-labor ratios. But this time, modern medicine might perversely stymie that outcome by preserving more lives, thus throwing off that ratio.

A rise in precautionary savings will continue to restrain global demand as shell-shocked households remain worried about their incomes. Declining business investment, which was already falling in the United States before the COVID-19 outbreak, will further constrain demand. Cautious spending on plant and equipment, in particular, will also disrupt global supply chains, implying slower future productivity and economic growth.

Borrowing costs will likely remain low for a long period, particularly as central banks engage in financial repression to control the costs of servicing higher public debt. On the other hand, debt repayments by households and businesses are mostly fixed regardless of their incomes and revenues. This means people and companies will need to control variable costs to avoid bankruptcies, which are already increasing due to the fallout from the pandemic.

The depth and duration of the global recession depend not only on the course of the virus and lockdowns, but on government stimulus measures remaining in place to support collapsing incomes and revenues. Such stimulus measures continue to lag in emerging markets, which have a high dependence on foreign financing. Financial markets seem “disconnected” from the real economy, and the IMF has warned that excessive risk-taking could result in “sudden stops” of capital flows to emerging markets if sentiment shifts again. Meanwhile, the World Trade Organization predicts a decline in world trade this year of 13-32 percent (equating to a 2.5-8.8 percent drop in global GDP), which will most acutely affect countries dependent on exports.