Containers sit stacked on a cargo ship berthed at China’s Zhoushan Port on Feb. 4, 2020. China’s COVID-19 outbreak and the subsequent closing of factories caused outbound shipping from the country to drop significantly at the beginning of the year.

By sapping global economic growth and emboldening nationalist calls against globalization, the COVID-19 crisis risks upending the past 30 years of rising intercontinental trade volumes. Countries have implemented various new shipping restrictions to contain the virus, though pandemic-induced declines in demand have so far prevented severe disruptions to international trade. But with the global recession likely to extend well into 2021, the long-term loss of business — exacerbated by a surge in U.S.-China trade tensions and security concerns over global supply chains — could cripple the shipping industry for years to come. In the meantime, the oversupply of container shipping capacity will force companies around the world to consolidate as their governments increasingly opt for more protectionist policies.

Short-Term Disruptions

- Shipping restrictions: In response to the COVID-19 pandemic, countries have imposed various restrictions on global shipping that have reduced efficiency and produced delays. This has included imposing 14-day quarantine periods on ships prior to docking, preventing crews from disembarking in port, and banning crew substitutions and transit to local airports. The actual spread of COVID-19 aboard commercial ships, however, has been modest, as many crews stay at sea for up to 10 months at a time. But bans on crew changes have forced some to extend their deployments.

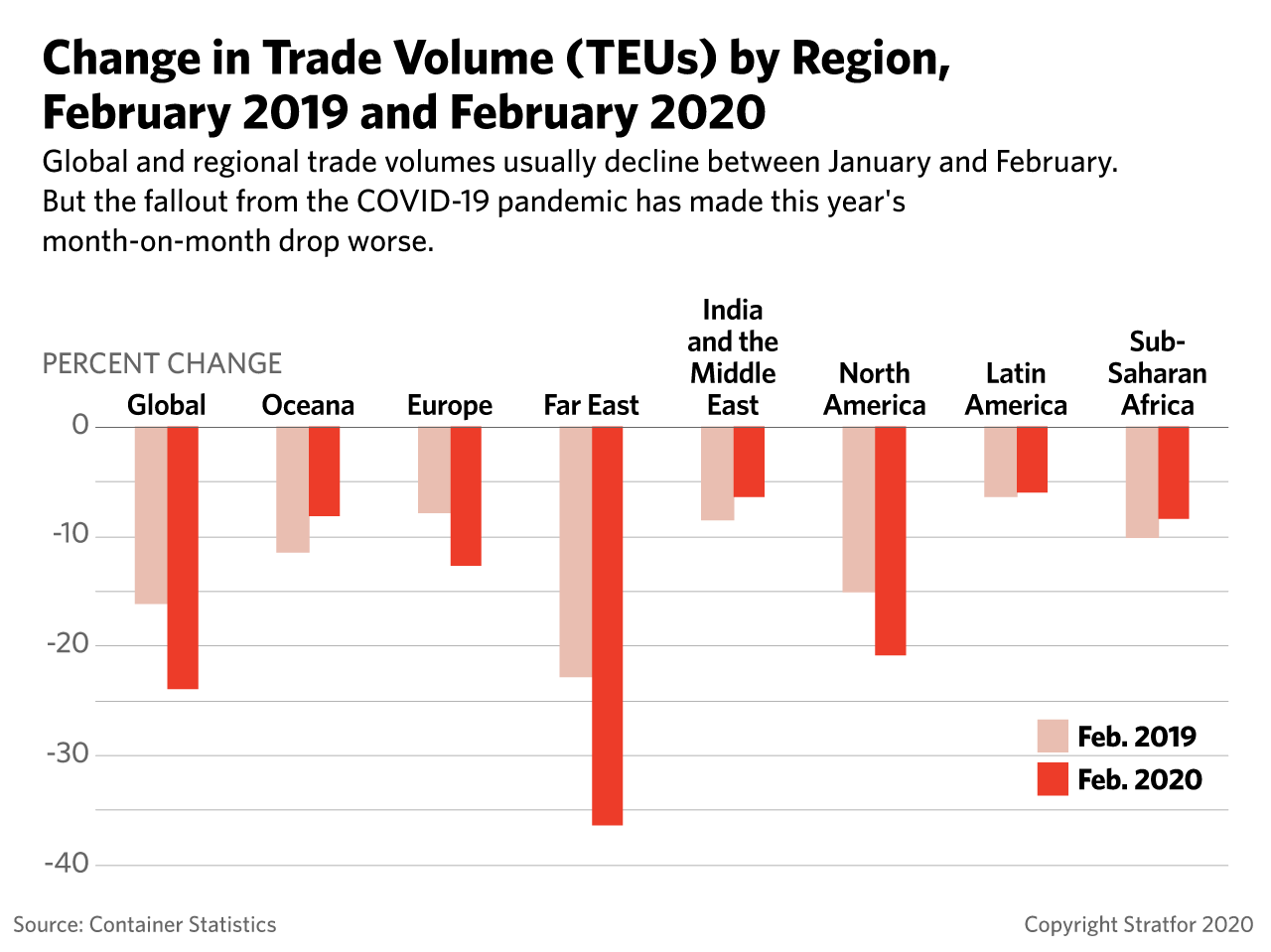

- Declining demand: Lack of demand amid the deepening global recession, however, has prevented or limited short-term disruptions in the container shipping sector that could have otherwise been an issue due to these labor, transportation and regulatory restrictions. The demand for the transportation of goods has plummeted, particularly in container shipping. In the first quarter of 2020, the impact was initially concentrated in China. But it has since spread more evenly around the world. Shipping capacity is now expected to fall by up to 20 percent on the Far East to North America route, and up to 25 percent in the second quarter of 2020 on the Far East to Europe route. As a result, shippers are now finding that container transport is available, but often with a couple of weeks delay in point-to-point time requirements. To prop up rates, ship owners have been "blanking" some departures by sailing back with completely empty ships.

- Container shortages: The drop in outbound shipping from China caused an initial container shortage at U.S. and European ports in the first quarter of 2020. But amid the reopening of factories in China through February and March, container availability at Chinese ports has since steadily fallen from the unusually high levels seen at the beginning of the year, and are now rising elsewhere.

Long-Term Implications

- A prolonged recession: Demand for container shipping demand will likely recover in the second half of the year. But after 2020, the outlook for global shipping remains grim. Without a vaccine available, the potential for repeated COVID-19 outbreaks will likely sustain the global recession for at least another year, restraining consumer spending in the process. Economic activity will not recover to pre-pandemic levels until at least 2022, and double-digit unemployment rates in developed economies could last well into 2021. Demand for services and durable goods, in particular — which consumers can do without in the short-term — will see the largest declines. As a result, container shipping volumes will remain depressed through 2021 relative to 2019 levels.

- Increased trade tensions: The pandemic will also likely increase in trade protectionism and further degrade U.S.-China relations. The administration of U.S. President Donald Trump had negotiated a "phase one" trade agreement with China in December. But the controversy over the Chinese government’s possible concealment of the true scope of the COVID-19 threat has since brought Washington’s rivalry with Beijing back to the fore. Amid the increase in U.S.-China tensions, the Trump administration has already imposed new restrictions and approval requirements for U.S. technology companies exporting goods to Chinese companies that do business with the Chinese military. But even if a new president takes office after the November 2020 election, these tensions are unlikely to be quickly resolved. Indeed, despite criticizing the White House’s overall response to the COVID-19 crisis, the presumptive Democratic nominee Joe Biden has also echoed some of Trump’s criticism of Chinese authorities.

- Reshoring imports: By intensifying efforts to "reshore" trade operations in China, the further deterioration of U.S.-China relations will continue to see a rise in U.S. imports from other countries with inexpensive labor, including Mexico, where most imports come across the border by truck. In 2019, U.S. manufactured goods imports from China were already down 17 percent year on year, partially offset by increases from Mexico and Vietnam.

- Shipping cancellations: While construction cancellations by shipping operators are difficult once the construction of a ship begins, some companies may be forced to pull back orders that were not yet under construction.

The Upshot

All of these factors are likely to leave an oversupply of container shipping in the coming years, even as container shipping volumes begin to recover. A turn toward worsening trade protectionism could prolong that period, which could keep container rates only slightly above breakeven levels through 2022. Several global shipping operators have already seen bond rating downgrades reflecting their weakened financial outlook.

Falling fuel prices will help offset some of the immediate impact of lower shipping rates, with global oil prices unlikely to rise much past $50 in 2021 as the COVID-19 crisis continues to drive down demand and increase inventory overhang among producers. New pollution standards set by the International Maritime Organization (IMO) last year forced owners of older ships to either cough up the costs of an expensive retrofit, or switch from using marine bunker fuel to more eco-friendly, low-sulfur marine diesel. The decline in diesel prices has made the latter option less cumbersome by lowering operating costs. But overcapacity will still probably accelerate the retirement of these older vessels over the course of the next one-to-three years as new vessels are built.