A trader wearing a protective mask stands on the floor of the Boursa Kuwait stock exchange in Kuwait City, Kuwait, on March 1, 2020. Plummeting oil and gas prices amid the global COVID-19 crisis have hit the seven energy-rich nations in the Gulf Cooperation Council (GCC), including Kuwait, particularly hard.

The Arab Gulf states within the Gulf Cooperation Council (GCC) are looking down the barrel of a serious, multilayered economic shock as COVID-19 disrupts their main revenue sources by slashing energy prices as well as overall global demand. The sharp reduction in government income across the region portends increased budget deficits and significant borrowing in the months ahead, creating debt that will complicate spending and investment for years to come. But while they may be delayed, Gulf states' diversification strategies and social reform plans won't be canceled, as the crisis has also made clearer than ever the need for GCC governments to wean their economies off of oil and gas, and their populations off of state aid.

Diversification Plans, Interrupted

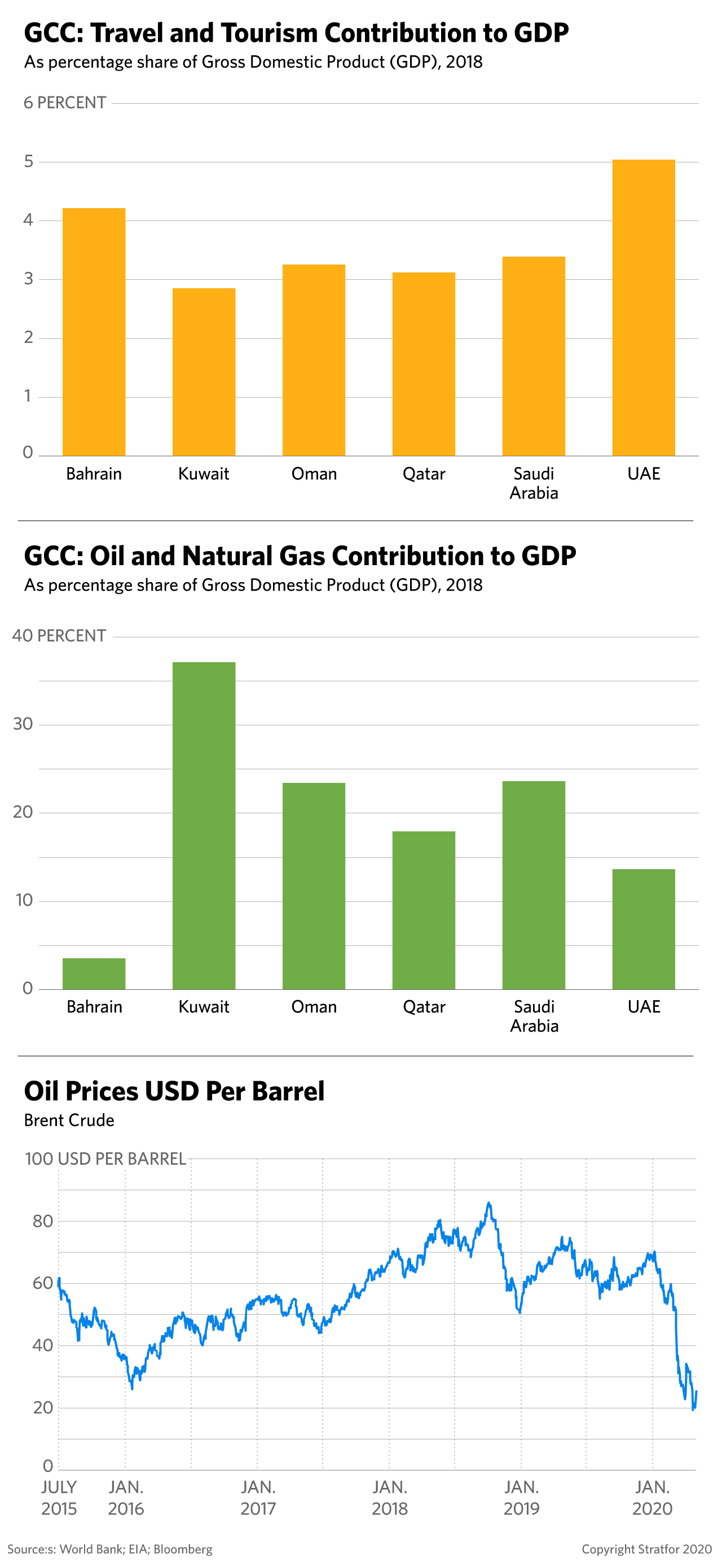

The economies of Gulf states share structural similarities but differ substantially in their levels of wealth, and in turn, their vulnerability to global economic shocks such as those being created by the COVID-19 pandemic. Oil output is contracting significantly this year, but the most energy- and cash-rich countries of Kuwait, Saudi Arabia, Qatar and the United Arab Emirates will have the largest buffers against swift financial ruin. Oman and Bahrain, on the other hand, lack the same deep pockets to help weather the storm, and are thus expected to slide into deeper dependence on their neighbors to make up anticipated shortfalls, especially as international debt markets remain wary of further supporting their already debt-ridden economies.

But in addition to detracting from these their primary source of revenue, the COVID-19 crisis is also depressing non-oil sectors, which these economies were banking on for their diversification strategies. Successful diversification away from energy depends not only on demand for non-oil services or products, but also on a continued source of oil and gas wealth to invest in diversification — especially at this early phase in the process. According to the International Monetary Fund (IMF)'s latest forecast, the economies of the seven GCC states are now expected to shrink an average of 2.7 percent this year compared with October's forecast of 2.5 percent growth, driven primarily by non-oil activity contracting by 4.3 percent due to low oil prices.

For many GCC countries, their vision of a less energy-reliant financial future included boosting their tourism and travel sectors. But the expected loss of travel revenue through this year due to the COVID-19 crisis exemplifies why these states will have to adjust or delay their diversification plans. Saudi Arabia, in particular, is losing out on the annual windfall from this year's massive Hajj pilgrimage this year and possibly next year depending on the virus's trajectory. The United Arab Emirates, meanwhile, has had to delay its much-touted Dubai Expo 2020, which was expected to bring $23 billion (or roughly a quarter of Dubai's GDP). Despite having a smaller tourism sector by volume compared with its wealthier neighbors, Oman will also suffer from the loss of visitors, given that tourism was particularly important to its diversification strategy in the years ahead as well.

A Fleeting Fix

To keep the loss of both oil- and non-oil revenue from quickly overwhelming their economies, the GCC states have all introduced similar initial stimulus packages. Tax and fee deferrals for small- and medium-sized businesses are happening across the board, as are guaranteed payroll support for GCC citizens and liquidity injections into the financial sector. But while these measures will help private sector companies in the near term, they will come at the cost of further reducing non-oil revenue and adding to fiscal deficits. The GCC's largest economy Saudi Arabia, for example, is using roughly one-third of a record $27 billion drawdown in its foreign reserves to bolster its banking sector.

As the crisis cuts into their cashflow, the wealthiest GCC states (except Kuwait, which often conducts its own unique and independent financial policy), are also turning to international and regional debt markets to help fund their stimulus packages, with Saudi Arabia is expected to see its largest-ever debt program this year.

Sky-High Social Spending

Gulf states, however, have notably not yet implemented direct cash transfers or subsidy assistance for citizens on a large scale amid the COVID-19 outbreak, except in cash-strapped Bahrain. In fact, there have been budgetary cuts to state spending across multiple ministries in several countries, with more spending cuts anticipated ahead. This is in part because these economies are already heavily state-driven, with citizens receiving significant economic support. Indeed, prior to the COVID-19 global economic crisis, GCC governments were in the midst of massive economic reform plans designed to wean nationals off of this substantial state spending, which has long been recognized as fiscally unsustainable.

To preserve social stability in the midst of a health and economic crisis, these states will avoid any sort of austerity measure for as long as possible. But the enduring financial crisis in the wake of COVID-19 will make the need to implement new taxes and fees, as well as roll back subsidies and generous state support, all the more imperative in the coming years. This will be especially true for cash-strapped Bahrain and Oman due to their small fiscal buffers, as well as Saudi Arabia due to its large population and deep dependence on energy revenue.

An Impetus to Act

There are, however, some silver linings amid the COVID-19 strain. The current, pandemic-depressed global environment will grant some investment opportunities for wealthier GCC states who have still cash on hand. Saudi Arabia, for example, is already investing in some distressed assets, and has yet to completely abandon its larger investment plans.

But the main focus in the near term for the GCC states will still be their political and economic survival. Being pushed to increase spending to fund stimulus will only accelerate the economic reform burden in the region, and will open up questions about the need to completely overhaul the way these economies are structured in the long term, including sensitive labor issues such as unemployment and pension reform, as well as immigration and visa policies.

For now, the IMF projects economic growth for Middle East oil exporters will rebound to 4.7 percent in 2021, though this depends on an optimistic view of the virus' trajectory, recovery in the global economy and oil price stabilization. No matter what happens, the decline in oil demand and tourism rates will weigh heavily on the Gulf states for years to come thanks to their inherent vulnerability to oil and gas volatility. And as a result, they may be among the last large economies to fully recover from the crisis.