A row of empty seats on a passenger aircraft. Travel restrictions and plummeting demand due to the coronavirus outbreak are ravaging the global airline industry, especially in key Asian and European markets.

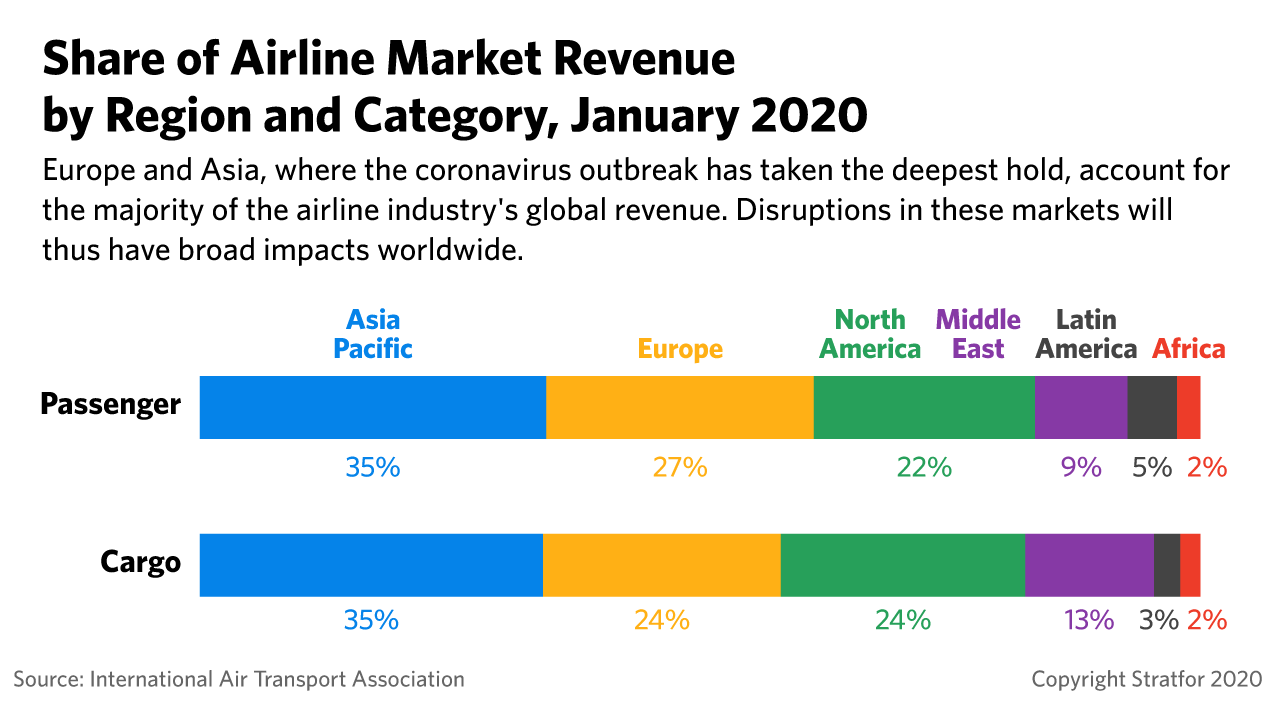

The coronavirus pandemic is ravaging the airline industry, with the most highly impacted countries of China, South Korea, Italy and Iran accounting for over a quarter of global passenger revenue alone. As panicked consumers continue to cancel or suspend their travel plans for fear of getting sick, and as more governments pursue containment measures and travel bans, an increasing number of airlines will be forced to either consolidate or go out of business.

In China, this will likely lead to a market that's even more dominated by the state-backed carriers. Bigger airlines in Europe, meanwhile, will merge as revenue losses deal the final blow to their smaller competitors. But while so much is still unknown about how the outbreak will unfold in the weeks ahead, what remains certain is that the airline industry is headed for even more unexpected turbulence.

Impact on the Chinese Market

China’s status as the epicenter and worst-affected country in the coronavirus outbreak means that its airline industry is set to sustain the greatest losses, although it is also the country with the first chance of recovery. Although China’s outbreak appears to have already peaked, its economy was all but offline for much of the period from late January to early March — most critically during the travel-heavy Lunar New Year holiday. Full figures have yet to emerge, but domestic Chinese travel dropped 6.8 percent year-on-year in January 2020. Airlines in China lost $3 billion in February amid the coronavirus outbreak, with an 84.5 percent drop in passenger traffic and a 21 percent drop in cargo flows.

For Chinese airlines, this translated into a February loss of over $1.44 billion and a revenue drop of $5.33 billion. In 2019 overall, China accounted for around $98 billion in domestic and international passenger revenue. But now, the International Air Transport Association (IATA) projects a 23 percent drop in Chinese passenger flows this year, with revenue dropping $22.2 billion. More uncertain, however, are the knock-on effects to Chinese airlines from the outbreaks in key international travel destinations such as South Korea, Japan, Singapore, Malaysia and Thailand. And the as-yet unclear overall impact of the coronavirus on both Chinese gross domestic product (GDP) growth, as well as global economic growth, could bring further damage to China's aviation sector as general consumption declines.

Amid the outbreak, the Chinese government has moved quickly to support the sector. On March 4, the Civil Aviation Commission of China (CAAC) unveiled financial incentives in the form of direct subsidies for airlines that resumed suspended service to international destinations through June 2020. Chinese airlines might have some relief as the country recovers from the outbreak, and works to get manufacturing back online and rebound from the bottleneck in overseas shipping by sending more goods by air. This would especially benefit the country's state-backed players (namely, Air China, China Southern and China Eastern), which are some of the world's largest cargo carriers. Passenger demand is also already starting to rebound in China’s domestic market from its February low point, but the stigma of the virus will take some time to dissipate. The first week of March saw 40 percent of flights resumed domestically but some of this uptick is being fueled by so-called "cabbage prices," or cheap seats meant to fill planes and not generate revenue.

But the sector still faces major headwinds, which will hit particularly hard on private and smaller players. China’s market is dominated by the so-called “Big Four” carriers, who command 84 percent of the country's aircraft fleet: Air China, China Southern, China Eastern and HNA Group. Of these, HNA Group is the only private entity, while the others are partly state-owned. While there's been recent government efforts to open up the airline sector somewhat and foster competition, the massive damage to the sector caused by the coronavirus outbreak may accelerate a trend back toward consolidation under the umbrella of the state-controlled carriers. In addition to its other supports to the ailing industry, the Chinese government is reportedly considering having the three big government-linked carriers — which still account for 46 percent of China's airline capacity — absorb smaller players unable to weather the crisis.

Even HNA Group may fall victim to this consolidation push. HNA Group’s aviation component accounts for 17.2 percent of the Chinese aircraft fleet and is comprised of 13 airlines, the largest of which by far is Hainan Airlines. But despite its outsized role in the sector, HNA Group has one of the highest corporate debt levels in the country at $35.6 billion — a 90 percent debt-to-capital ratio — due to an overseas buying binge that in 2017 put it in the crosshairs of both Chinese and overseas regulators. HNA Group has since been working to offload hotel, property and insurance assets in an attempt to attain some sort of financial stability. In November, it announced plans to focus the business on its more profitable aviation units and to separate this from a "non-aviation asset management unit." But the carrier has since been hit hard by the coronavirus, compelling the Chinese government to intervene. In January, Hainan airlines reported a 35 percent year-on-year drop in passenger flows. The Hainan provincial government recently appointed two of its officials to serve as co-CEO and executive chairman of HNA Group, as part of a working group to manage the company's financial problems in conjunction with the CAAC and China Development Bank. Reports indicate that the government will direct an aggressive campaign to sell off HNA Group’s assets with a possibility that its aviation components may be taken on by Air China, China Southern and China Eastern.

All in all, the coronavirus outbreak will likely bring about a degree of consolidation of the sector under the mantle of these three state-backed carriers, allowing China to prop up its industry in a way more difficult for other countries and regions. Greater consolidation will mean an increased ability for the sector to outcompete regional rivals and to set higher prices for consumers. But Beijing will still tread carefully. Already the increased state oversight of HNA Group has raised the prospect that the airliner's American assets could come under scrutiny by the Committee on Foreign Investment in the United States (CFIUS). If HNA's airline assets are eventually brought under the purview of China's big three government-linked carriers, it will need to avoid strengthening one of these players to the detriment of the others.

Impact on European Markets

Meanwhile, in Europe, the coronavirus outbreak is severely threatening the profitability of most European airlines. On March 5, the IATA warned that airlines operating in Western Europe could see a reduction in passengers of up to 24 percent this year, and a fall in passenger revenue of more than $37 billion. Several factors explain the problems facing European airlines. For one, many carriers have suspended their flights to China, Italy and other countries with high numbers of confirmed coronavirus cases. Anxiety is also hurting holiday traffic and undermining travel to popular destinations in countries like Spain or Italy, as lots of people are canceling or postponing their vacations for fear of contracting the virus. Meanwhile, companies across the continent are telling staff to work from home and suspend all non-essential travel, which reduces demand for flights to business centers such as London, Paris, Frankfurt or Geneva.

The U.S. government's recent announcement that it was banning all flights from 26 European countries for a month beginning March 13 will make matters even worse for airlines operating routes to the United States. In addition, several international fairs and sports and cultural events in Europe have either been canceled (such as the Mobile World Congress in Barcelona) or postponed (such as the International Motor Show in Geneva), which further undermines demand for flights to the cities holding them. Against this gloomy outlook for Europe's crucial tourism industry, airlines have also been among the main losers in recent drops in stock exchanges in Europe and other parts of the world.

For the companies that were having financial problems before the outbreak, the coronavirus has made things even more difficult. This is the case of Britain’s Flybe, which went into administration on March 5, leaving thousands of passengers stranded and putting some 2,000 jobs at risk. But the escalating coronavirus crisis has begun testing the endurance of stronger European airlines as well. In recent weeks, companies including British Airways and Finnair warned of significant falls in their operating profit this year because of the outbreak, while airlines including Lufthansa, Easy Jet, Virgin Atlantic and Ryanair said they were considering measures such as freezing recruitment, promotion and pay rises, as well as offering unpaid leave to their staff. Many airlines are also calling on regulators around the world to suspend a rule according to which they lose landing and take-off slots in airports if they don’t use them for prolonged periods. This has forced several airlines to operate "ghost flights" with little to no passengers to preserve some of their routes, which further weakens their profitability. On March 10, the European Commission announced that it would temporarily suspend these rules.

However, some airlines are making it clear that the ongoing crisis should not open the door to national governments granting financial aid to weak companies. William M. Walsh, the CEO of the International Airlines Group (which owns British Airways), recently said that governments should not provide state aid to "airlines that were not sustainable before the coronavirus.” As national governments in Europe struggle to come up with stimulus measures for the economy, they may not have fiscal room to rescue airlines in trouble. Governments are more likely to help airlines via tax benefits or tax delays, and not so much through bailouts. This could result in more of the weaker players collapsing, as the Flybe case illustrates.

The spread of the coronavirus in Europe will eventually be contained, but it will be weeks, if not months, before that happens. In the meantime, companies will struggle to adapt to this new environment. And policies that are meant to reduce internal costs (such as offering employees unpaid leave or suspending the purchase of new aircraft), as well as strategies to boost sales (such as offering customers the chance to rebook their flights for free, or giving them discount prices for flights), may not be enough to save the weaker players in the industry. And as carriers continue to face millions in revenue losses, those that were already struggling to make ends meet before the outbreak may not survive.

By bankrupting some companies and forcing others to merge in order to mitigate their revenue losses, the coronavirus crisis will likely accelerate the ongoing process of consolidating Europe’s airline sector. As a result, many small players will disappear as the bigger players get bigger. When the coronavirus outbreak eventually wanes, Europeans may find that former airline competitors are now owned by the same parent companies. But while this could mean higher prices and fewer options for consumers, it would also mean a less fragmented and somewhat more cost-effective airline sector in Europe.

The Unknown Global Impact

The now global coronavirus outbreak is highly fluid and its spread unpredictable, meaning that both new and sustained outbreaks will likely bring further knock-on effects to the sector. In the Middle East, where Iran has been at the regional epicenter of the outbreak, low oil prices will limit the government’s ability to prop up airlines in the face of declining demand amid already growing global competition. In the United States, where many global air airlines are based, carriers are already expecting to annualize declines in Revenue Passenger Miles (RPMs) significantly greater than those even following the Sept. 11 terrorist attacks.

And, lastly, the still-unknown fallout in terms of global economic growth due to the virus could further stymie demand and damage the industry. The IATA now forecasts that the global passenger airline sector will lose between $63 billion and $113 billion. But whether losses meet or exceed the far end of this spectrum will depend on the scope and trajectory of the increasingly global outbreak — especially in the United States, where the situation is rapidly evolving. The key will be whether more countries experience surges in coronavirus cases, and whether transmission rates in the Northern Hemisphere slow as the weather warms in the months ahead.