Lebanese pounds.

Lebanon is highly likely to default on a $1.2 billion, 10-year eurobond that matures March 9. Even if it makes that payment, the country's finances are near collapse. When that happens it will accelerate a crisis in the country's insolvent banking sector, probably deepening its ongoing currency crisis and setting off a downward economic spiral threatening social and political stability.

Perverse as it sounds, the government might decide it is better to default now rather than using up scarce foreign exchange and putting off what financial markets already consider inevitable. The only real question is whether the government can muster the political will to act now — and penalize the political and financial elite which benefits from Lebanon's rentier-type economy, in which citizens are dependent on government largesse often according to sect and political affiliation — or whether it will give priority to external creditors at the expense of the Lebanese middle class, which is limited in accessing its bank deposits. The former would require a credible path to stabilize government finances and restructure debt, possibly with some type of international support, as well as a probable devaluation of the Lebanese currency. Waiting will inevitably increase the size of the economic adjustment required, since ultimately there is no alternative to required economic changes

The newly formed government under Prime Minister Hassan Diab will bear the brunt of the inevitably negative popular blowback. Over the long term, as Diab becomes synonymous with painful economic restructuring, his main patron, Hezbollah, might suffer politically, in turn boosting the standing of Hezbollah's political rivals in the March 14 Movement. These rivals include the Sunni al-Hariri clan, which has strategically opted not to participate in the government during this chaotic time. This political reality is one reason why Hezbollah has opposed, and will continue to oppose, economic restructuring and any external financial relief.

Unsustainable Financials

Lebanon's public finances and banking system operate much like a giant Ponzi scheme, this one reliant on new foreign currency deposits and new debt to repay old debt. Tax revenues finance less than half of government spending, but political will to implement new taxes is historically nonexistent. As long as foreign currency deposits and new debt continue to grow, however, the scheme can continue, with the government running large budget deficits, funded by borrowing mainly in dollars from the central bank and domestic banks that depend on a steady inflow of hard currency remittances and bank deposits from abroad.

The central bank maintains high deposit rates to attract funds which it then uses to finance government budget deficits and to protect a 22-year peg of the Lebanese pound to the dollar. The result is a bloated banking system with assets equal to more than 400 percent of GDP, nearly 70 percent of which are foreign currency claims on the government. Large bank lending to the government crowds out private investment in productive activities that boost growth. As a case in point, lending to the private sector — much of it for real estate investment — accounts for less than 28 percent of bank assets. The banking system, including the central bank, provided the equivalent of 12 percent of GDP in new financing to the government in 2018, which actually exceeded the government's overall fiscal deficit of 11 percent of GDP.

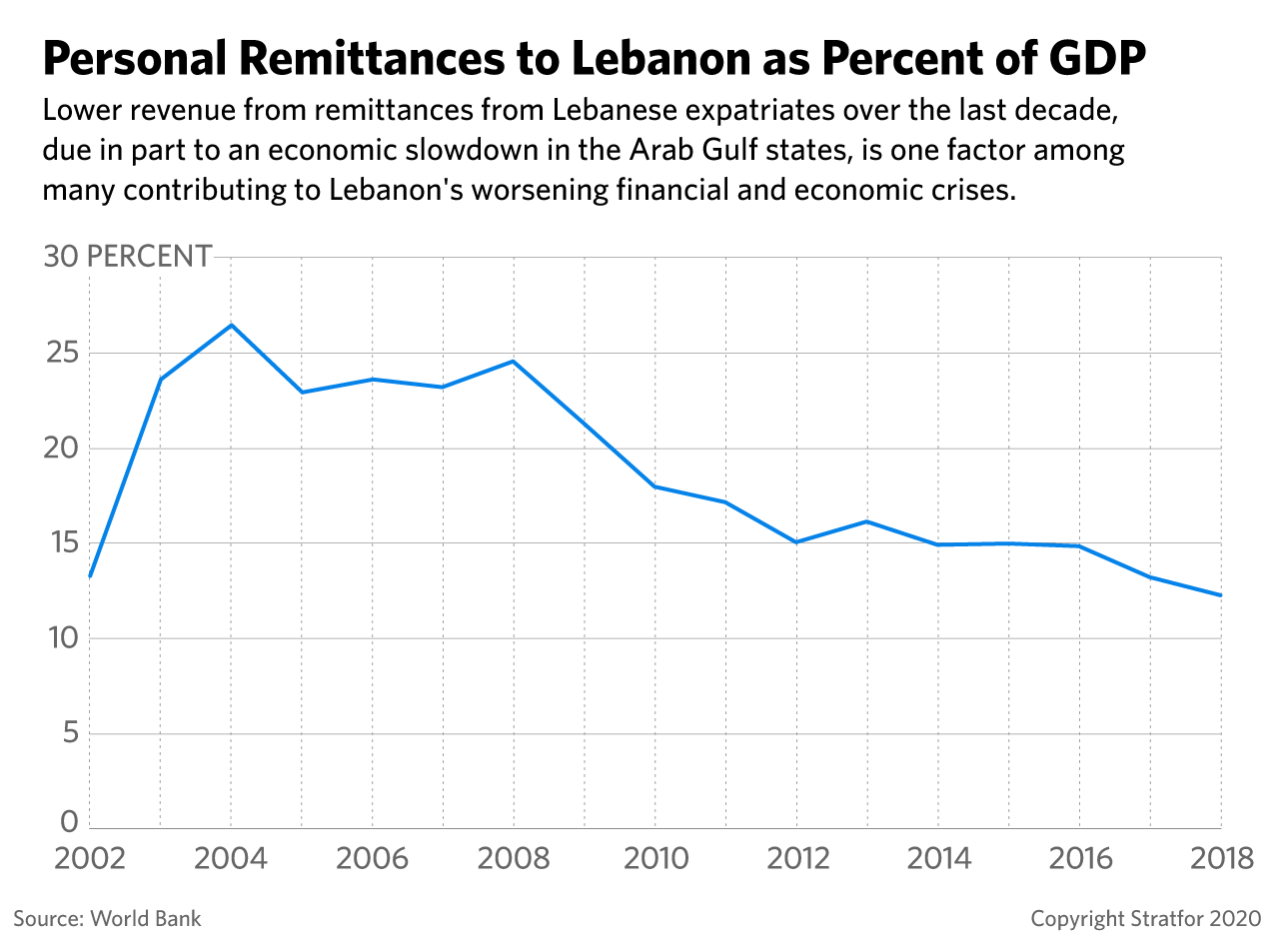

Deposits by wealthy residents and the Lebanese diaspora account for most of the banking system's liabilities, but remittances have been halved as a percentage of GDP since 2008 due to economic slowdowns in the rest of the region where Lebanese expatriates work, including the oil-rich Arab Gulf states, where lower oil prices have been the norm since 2014. Bank deposit levels probably declined in 2019-Q4 as the depth of the financial crisis started to become evident and capital flight accelerated.

Lebanon's current account deficit, one of the highest in the world at more than 25 percent of GDP in 2018 despite chronic low growth, further illustrates the economic imbalances. A fixed exchange rate, which the IMF estimates is at least 50 percent overvalued, discourages exports and encourages goods imports, which were five times the size of goods exports in 2018. That probably includes capital flight through over-invoicing of imports, given that more than a third of the 2018 current account deficit of $14 billion was "financed" by "errors and omissions" in the balance of payments accounts.

No Good Options

In the long term, there is no path to resolution that won't involve pain for large parts of the Lebanese population, government and banks. Solutions could involve an IMF-supported stabilization program with drastic cuts in public spending other than for the social safety net and infrastructure, along with a reorganization and recapitalization of the banks, while giving a haircut to a substantial amount of the debt. That would require a reorganization of banking liabilities in a way that would protect small depositors. A currency devaluation is also necessary, which, although inflationary, would be less so than continued unsustainable monetary financing of government deficits.

Painful as it will be, and though it will guarantee popular unrest, the government is likely to begin rolling out such austerity measures very soon. The prime minister's office said March 4 that intensive measures, yet unspecified, would be implemented beginning March 10. Lebanese citizens are already worried about the steadily dropping value of their life savings. A devaluation would only deepen this concern, ultimately driving unrest, but is a necessary step to begin to reinvigorate the economy. Anxiety over possible disruptions to imports of critical goods will further drive protests, threatening the Diab government's durability and hampering business continuity.

In the near term, the debt restructuring challenge is the most critical issue. The government tried early this year to perpetuate the overall Ponzi scheme, proposing an exchange of longer-dated maturities for the March 9 payment. Rating agencies, however, said that would be a default event, and the idea was dropped. It's unclear if the central bank has resources to make this payment, let alone similar ones due in April and June. It reports gross foreign exchange reserves of nearly $40 billion, but does not publish a balance sheet and could well have net negative reserves. Exports are not even large enough to meet critical import needs, which the finance minister estimated recently as at least $4 billion to $5 billion per year.

So the question facing the government is whether to conserve foreign exchange reserves or default on the payment, which, when assets are marked to market or sold at a loss, would make the country's banks insolvent. Banks have depleted equity to absorb losses on assets, which are trading at discounts of up to 70 percent.

Nevertheless, Lebanon's government would probably rather face the wrath of bondholders than of protesters, so it will probably choose to cover necessary imports while failing to make debt repayments. That is a crisis of a different type, one that will affect primarily the wealthy in Lebanon and the international bondholders who bet that Lebanese debt had a reliable return. But it will still allow Diab's government to argue that the country is in crisis and that it needs more support than what international allies are providing, and it will help control social tensions in Lebanon by ensuring that some essential imports continue for everyday Lebanese. But it will, however, hurt wealthy Lebanese insiders, who form the backbone of the state. It will also put the country into a new economic crisis that eventually will require tough measures to solve and will impact ordinary Lebanese.