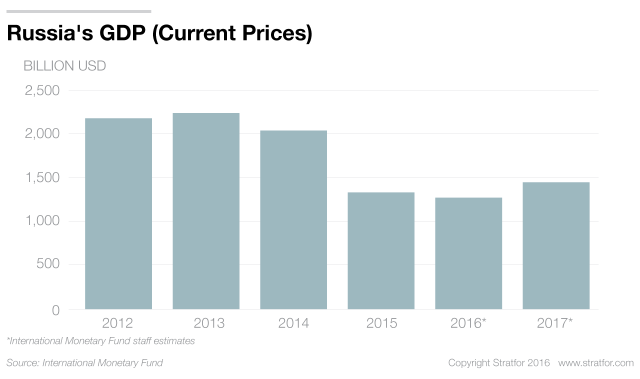

For two and a half years, the Russian economy has struggled in recession, mostly as a result of low oil prices. (Oil revenue traditionally accounts for a quarter of the country's gross domestic product and half of its federal budget.) Western sanctions against Russia and declining foreign investment compounded the effects of low energy revenue, creating a perfect storm for the country's finances. Though the economy has shown signs of improvement this year — the ruble recovered 14 percent against the dollar, and inflation is down by nearly half from its 15-year high in 2015 — Russia's GDP remains diminished.

Drafting on a Budget

The first iteration of this year's budget assumed that oil, at $50 per barrel, would make up half of government revenue as usual. Less than a month into the year, though, the Kremlin had already slashed each ministry's budget by 10 percent and adjusted its expectations for the price of oil to $40 per barrel. As the year wraps up, the Kremlin finally seems to have a handle on its revenue and spending for the year, which have been whittled to less than half of those in pre-recession budgets. Energy revenue has accounted for only 37 percent of government income this year, an indication not of diversification on the Kremlin's part but of the austerity measures the government has had to implement. Despite tightening its belt, the Kremlin still had a budget deficit of $48 billion in October after issuing an extra $2 billion to retirees before the September legislative elections and handing another $12 billion to Russia's ailing defense industry.

To keep the budget deficit under the president's 3 percent target, Russia's government has had to get creative. The Kremlin plans to raise more than $17 billion by privatizing swaths of two of its largest oil firms, Rosneft and Bashneft, before the end of the year. Rosneft, Russia's biggest oil company, has fought its privatization for years, but now Putin and the company's head, Igor Sechin, seem to have reached a compromise. Having purchased a controlling stake in Bashneft, Rosneft will buy its own shares from the Kremlin during its privatization in November. This solution will enable the Kremlin to begin filling in its budget gap, while also settling the dispute between Sechin and Putin — for now. (In early October, the president warned Sechin that the Kremlin still intends to sell Rosneft to a foreign partner eventually.) The rest of the money will come from the Reserve Fund, one of two primary government funds. The fund, which Moscow has already tapped this year to keep state firms and banks afloat, currently holds some $32 billion — just over one-third of its pre-recession level. Although these measures will be enough to resolve this year's budget problems, the seemingly endless revisions to the budget and the dwindling reserve have many Russians worried about the future.

Moscow Accepts Its Financial Reality

But Russia's leaders appear to be coming to grips with the country's financial straits. Over the past two years, the Kremlin has refrained from drafting multiyear budgets, focusing on a single year — or even a single quarter — at a time. But starting with next year's budget, the Kremlin is returning to a longer-term approach, drawing up plans for 2018-19 as well. Like much of the international community, Moscow believes that the Russian economy has hit its bottom and could start to climb out of recession next year. The Russian government projects a modest recovery, estimating slight but steady GDP growth of 0.6 percent in 2017 — 0.4 percent lower than the International Monetary Fund's projection — 1.7 percent in 2018 and 2.1 percent in 2019. Even so, the Kremlin is keeping its revenue and spending projections close to this year's, while tempering its expectations for the price of oil, which it estimates at $40 per barrel, about $10 less than the current price. Putin suggested the more conservative rate during a recent Cabinet meeting, warning that the country should be prepared in case Saudi Arabia and the other OPEC producers adjust production. Prime Minister Dmitri Medvedev, meanwhile, ordered Russia's financial and economic circles to devise ways to spur economic growth, should it start to lag again next year.

The 2017-2019 budget will allow for a nearly $40 billion budget deficit — the largest in over a decade. At the same time, it promises to slash defense spending by about $16 billion (though Russian newspaper Novaya Gazeta reports that one-third of slated spending in 2017 is classified as "closed expenditures," 70 percent of which will go to defense). Moscow also plans to borrow some $7 billion on the international markets for 2017, sparking controversy in the Kremlin. Many prominent figures in the government, such as Medvedev and central bank chief Elvira Nabiullina, have expressed concern about Russia's growing reliance on foreign debt. Over the summer, Moscow sold its first batch of eurobonds since the West imposed its sanctions on Russia, and the Kremlin is planning to sell another $4 billion worth. (State lender VTB Group, and not a foreign bank, will continue to underwrite the sales, however.) Furthermore, the West has not lifted its sanctions on the country and has in fact threatened to increase them over Russia's actions in Syria.

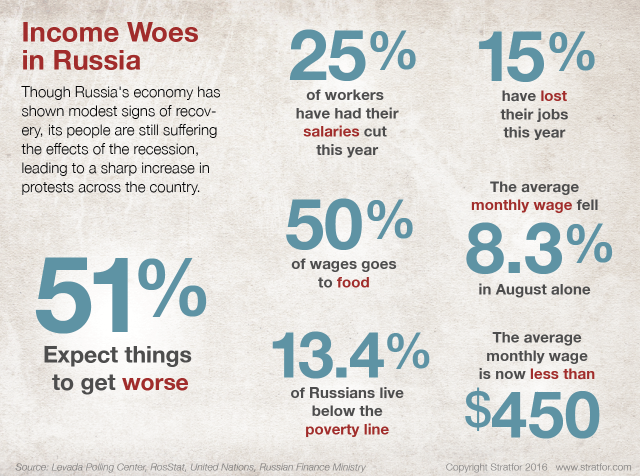

The Plight of the People

A tight budget and international borrowing will not be enough to support Russia's spending, though. In addition to these measures, the Kremlin will have to draw on what remains of the Reserve Fund in 2017 and then tap into the $74 billion National Wealth Fund, which is meant to support Russia's pension system. Because retirees make up a third of Russia's population, and most families include at least one retired person, the Kremlin's use of the fund could draw blowback from the Russian people. After all, many Russians are already aggrieved after years of economic hardship. Though the government has come up with a politically and financially viable budget to muddle through the next year, the Russian people continue to suffer the worst effects of the recession. The Kremlin's spending has helped keep Russian firms and government agencies afloat, but that money has not trickled down to the average citizen. Protests are on the rise across the country, and most Russians expect their financial situation to worsen in the next year, despite glimmers of improvement in the economy. Even with lower inflation, Russians are still spending nearly half their incomes on food on average, and they are worried about pay cuts and layoffs.

Amid these social and economic pressures, Putin is preparing to enter the next election cycle in a bid for a fourth term as president. When Putin last announced his intention to seek another term, mass protests rocked the country and its leaders. To avoid that outcome, the Kremlin is trying a strategy similar to the one it used to keep the peace and shore up support during the recent legislative elections. But pledges to boost health care spending and stop tax increases may not be enough to win over the Russian electorate. To maintain his hold on power, Putin may have to put his money where his mouth is and deliver the prosperity the Russian people have come to expect.